PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851613

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851613

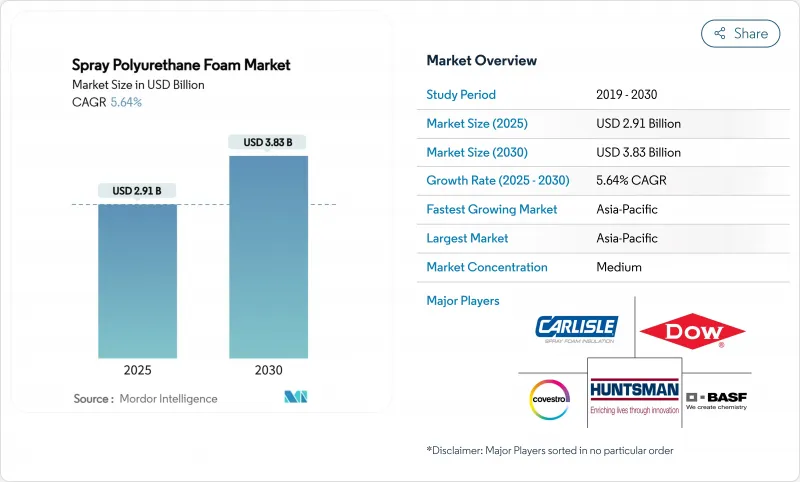

Spray Polyurethane Foam - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Spray Polyurethane Foam Market size is estimated at USD 2.91 billion in 2025, and is expected to reach USD 3.83 billion by 2030, at a CAGR of 5.64% during the forecast period (2025-2030).

This expansion occurs as building-energy codes tighten, low-GWP regulations take effect, and cold-chain investment accelerates, driving higher-value insulation demand. Manufacturers are swapping high-GWP HFCs for hydrofluoroolefin and other next-generation blowing agents to comply with the EPA's Technology Transitions Restrictions rule that began on 1 January 2025 epa.gov. Consolidation among installers, growing retrofit activity, and ESG-linked financing further reinforce momentum across residential, commercial, and industrial projects, while innovation in CO2-based polyols positions suppliers for long-term sustainability gains.

Global Spray Polyurethane Foam Market Trends and Insights

Strict Building-Energy Codes and Retrofit Mandates

The 2024 International Energy Conservation Code elevates closed-cell spray foam as a preferred air-barrier solution, compelling architects to specify higher R-values and moisture control measures. California's 2023 standards and Florida's 2026 code update both streamline retrofit approvals, lowering removal costs and accelerating demand, particularly for low-slope commercial roofs These rule changes widen the retrofit addressable base, encourage hybrid insulation assemblies, and push contractors toward more training and equipment investment that favors two-component systems.

Rising Concerns Over GHG Emissions

Corporate net-zero goals merge with building-owner cost targets, highlighting spray foam's ability to cut heating-and-cooling energy by up to 10% according to the EPA's Energy Star program. Installed Building Products reported a 55% CO2 reduction from spray foam use since 2020 while materially increasing output, showing the technology's decoupling of growth from emissions. Manufacturers such as Johns Manville logged double-digit drops in absolute emissions even as energy-saving product volumes rose, underscoring alignment between sustainability and profitability.

Competition from Fiberglass and Cellulose

Cost-focused residential builders still default to fiberglass batts, supported by long-standing installer networks and low equipment requirements. Home Innovation Research Labs data showed an 11% to 8% pullback in spray foam share amid multifamily growth and material cost saving, highlighting price sensitivity. Fiberglass makers are narrowing performance gaps with higher-density offerings, while cellulose leverages recycled content branding to appeal to eco-minded consumers. Spray foam suppliers must therefore sharpen value messaging around lifecycle energy savings to overcome higher upfront spend.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Cold-Chain and Refrigerated Logistics

- ESG-Linked Green-Bond Financing for SPF Upgrades

- Regulations and Restrictions on Di-Isocyanates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The segment anchored by two-component high-pressure systems held a 37.62% spray polyurethane foam market share in 2024, reflecting consistent on-site mixing, superior R-values, and code acceptance in commercial construction. BASF's new isocyanate and TPU lines in Zhanjiang strengthen local supply chains, reinforcing the segment's dominance in Asia-Pacific. Semi-rigid spray foam is expanding at a 7.19% CAGR as infrastructure projects need flexibility for vibration and temperature swings. One-component cans address small-project convenience, while low-pressure kits cover sensitive substrates where reduced exothermic heat is critical.

A push for integrated brands illustrates competitive strategy: Holcim's Enverge(R) label merges Gaco(TM) and SES(TM) portfolios, giving installers a single specification path for roof, wall, and specialty foams. Product diversification frames cross-selling opportunities, with semi-rigid innovations aimed at solar-ready roofs and bridge decks, and intumescent-infused systems targeting fire-resistance regulations. Suppliers that maintain broad catalogs and regional technical centers remain best positioned to seize specification wins.

The Spray Polyurethane Foam Market Report is Segmented by Product Type (Two-Component High-Pressure Spray Foam, Two-Component Low-Pressure Spray Foam, and More), Application (Insulation, Waterproofing, Asbestos Encapsulation, Sealant, Other Application), End-Use Industry (Residential Buildings, Commercial Buildings, Industrial and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa).

Geography Analysis

Asia-Pacific captured 48.19% of spray polyurethane foam market share in 2024 and is forecast to climb at 7.66% CAGR, driven by rapid urbanization, factory expansions, and energy-code adoption. China's real-estate slowdown redirects stimulus toward urban renewal, boosting retrofit insulation spend, while India's HVAC sector is set to hit USD 30 billion by 2030 on a 15.8% CAGR pathway, raising demand for building envelope upgrades. Japan and South Korea enforce stringent envelope requirements in seismic zones, favoring lightweight, high-adhesion insulation such as spray foam. ASEAN nations expand cold-chain capacity for seafood and vaccine storage, pulling regional demand upward. BASF's multi-year USD 19.5 billion Asia-Pacific investment plan exemplifies supplier confidence in the region's absorption capacity.

North America remains a mature but stable arena where federal HFC phase-outs harmonize compliance and keep specification complexity low. Canada's cold climates sustain thick-layer attic spray foam usage, while Mexico emerges as the world's fourth-largest polyurethane consumer on near-shoring momentum and automotive manufacturing growth. Consolidation among contractors enables national builders to standardize envelope solutions across the US and Canada, reinforced by TopBuild's network expansion.

Europe's net-zero directives and renovation wave stimulate demand despite tepid macro-economics. Di-isocyanate training rules introduce friction but ultimately favor well-capitalized manufacturers with robust EHS programs. Covestro's DreamResource project introduces rigid foam containing 20% CO2 as feedstock, demonstrating European leadership in circular chemistry. University of Liege advances isocyanate-free foams with 70-90% biobased content, underscoring regional academic-industry collaboration. In South America and the Middle East and Africa, energy-efficiency codes are tightening gradually; early movers in Brazil, Saudi Arabia, and the UAE adopt spray foam in commercial megaprojects, signaling future volume uplift.

- BASF

- Accella Polyurethane Systems

- Carlisle Spray Foam Insulation

- Covestro AG

- Dow

- FOAM-LOK (Firestone)

- GACO

- Huntsman Corporation LLC

- ISOTHANE LTD

- Johns Manville

- NCFI Polyurethanes

- Rhino Linings

- SOPREMA Canada.

- SWD Urethane

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strict Building-Energy Codes and Retrofit Mandates

- 4.2.2 Rising Concerns over GHG Emissions

- 4.2.3 Growth in Cold-Chain and Refrigerated Logistics

- 4.2.4 ESG-linked green bond financing for SPF upgrades

- 4.2.5 High-lift Foam Demand for Solar-Ready Roofs

- 4.3 Market Restraints

- 4.3.1 Competition from Fiberglass and Cellulose

- 4.3.2 Regulations and Restrictions on Di-isocyanates

- 4.3.3 HFO Blowing-agent Supply Volatility

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Two-Component High-Pressure Spray Foam

- 5.1.2 Two-Component Low-Pressure Spray Foam

- 5.1.3 One-Component Foam (OCF)

- 5.1.4 Semi-Rigid Spray Foam

- 5.2 By Application

- 5.2.1 Insulation

- 5.2.2 Waterproofing

- 5.2.3 Asbestos Encapsulation

- 5.2.4 Sealant

- 5.2.5 Other Application (Concrete Lifting / Void Filling, etc.)

- 5.3 By End-use Industry

- 5.3.1 Residential Buildings

- 5.3.2 Commercial Buildings

- 5.3.3 Industrial and Infrastructure

- 5.3.4 Agriculture and Specialty

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Accella Polyurethane Systems

- 6.4.3 Carlisle Spray Foam Insulation

- 6.4.4 Covestro AG

- 6.4.5 Dow

- 6.4.6 FOAM-LOK (Firestone)

- 6.4.7 GACO

- 6.4.8 Huntsman Corporation LLC

- 6.4.9 ISOTHANE LTD

- 6.4.10 Johns Manville

- 6.4.11 NCFI Polyurethanes

- 6.4.12 Rhino Linings

- 6.4.13 SOPREMA Canada.

- 6.4.14 SWD Urethane

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment