PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851782

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851782

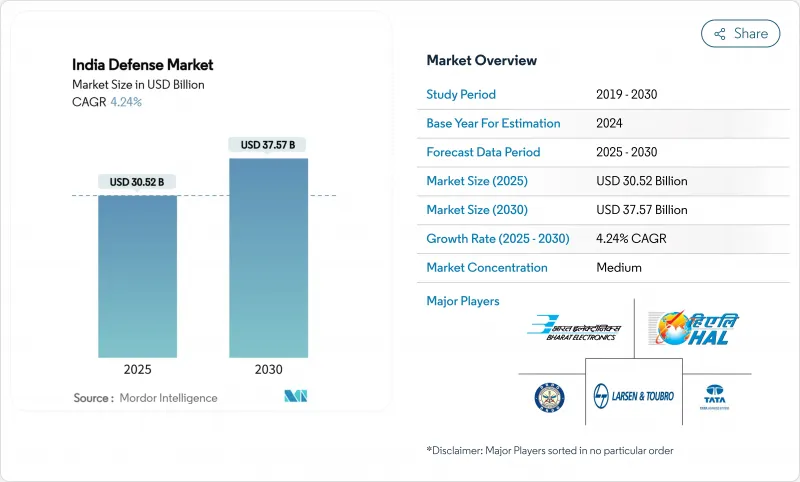

India Defense - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The India defense market is valued at USD 30.52 billion in 2025 and is forecasted to reach a market size of USD 37.57 billion by 2030, expanding at a 4.24% CAGR.

Robust funding, a 75% domestic-procurement mandate, and steady private-sector entry fuel the market's measured growth. Rising border tensions with China and Pakistan are accelerating near-term acquisitions, while the 2025 "Year of Reforms" program prioritizes integrated modernization across land, sea, air, cyber, and space domains. Record-high domestic production in FY 2024 underscores how localization policies reshape supply chains. At the same time, export successes such as BrahMos missile deals highlight India's emergence as a technology provider in the wider Indo-Pacific region.

India Defense Market Trends and Insights

Expanding Defense Budget and Localization Drive

The FY 2025-26 Union Budget allocates INR 6.81 trillion (USD 78.7 billion) to defense, a 9.5% rise over the previous year. Three-quarters of the modernization outlay is ring-fenced for domestic sourcing, pressing global OEMs to partner locally or cede market access. DRDO's INR 26,816.82 crore (USD 3.13 billion) research budget backs 100 priority projects, while 509 import-prohibited items anchor captive demand for Indian suppliers. Although capital spending hit INR 1.8 trillion (USD 21 billion), defense still absorbs only 1.9% of GDP, prompting innovative financing such as a proposed non-lapsable modernization fund. Together, these measures widen the addressable Indian defense market for homegrown firms and nudge foreign players toward deeper technology transfer.

Accelerated Investment in AI-Enabled Combat and Autonomous Swarm Technologies

The Defence Artificial Intelligence Project Agency receives USD 12 million annually to prototype cognitive radar and autonomous swarms. Exercises such as Dakshin Shakti showcased human-in-the-loop swarms that align with India's doctrinal emphasis on operator oversight. Startup engagement via the iDEX program has onboarded 194 firms, shortening innovation cycles and easing entry barriers. However, limited access to high-end semiconductors-constrained by US export controls-creates a technology gap that India's USD 10 billion Semiconductor Mission seeks to close. The ability to indigenize chips will ultimately determine whether AI capabilities migrate from demonstrations to line units, shaping the long-run trajectory of the Indian defense market.

Vulnerabilities in Critical Alloy and Semiconductor Supply Chains

India imports 82% of lithium and 76% of silicon from China, risking production delays for precision weapons and avionics. Semiconductor shortages postponed Tejas Mk-1A deliveries by eight months, exposing cascading effects on downstream programs. The National Critical Mineral Mission earmarks INR 16,000 crore (USD 1.87 billion) to secure 50 overseas mines, yet geopolitical frictions could restrict access. Tata Electronics' fab, expected online in 2026, will narrow but not eliminate short-term supply gaps. Dual-sourcing and the India-US TRUST initiative offer mitigation, but ITAR curbs limit technology depth, tempering growth across the Indian defense market.

Other drivers and restraints analyzed in the detailed report include:

- Escalating Geopolitical Tensions Along the Borders

- Emergence of Dual-Use Space Assets Driving C4ISR Capability Demand

- Inefficient and Bureaucratic Defense Procurement Framework

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Army commanded 46.78% of the Indian defense market in 2024, a position earned through extensive modernization needs across 6,811 km of disputed borders. Yet the Navy's 5.26% forecast CAGR signals growing maritime focus as India asserts Indo-Pacific influence. INS Vikrant, INS Surat, and INS Vaghsheer entered service in 2025 with 75% indigenous content, underlining local shipbuilding maturity. Project 75I's INR 43,000 crore (USD 5.02 billion) AIP-enabled submarine program further elevates naval technological complexity.

The Air Force, hampered by a 31-squadron fleet versus an authorized 42, sees slower budget traction despite urgent requirements. HAL's AMCA program-a joint venture with four private firms-marks a pivot toward collaborative high-technology development. Concurrently, the Navy's Sprint initiative aims to field 75 new Indigenous technologies each year, outpacing peer services in R&D intensity. Upcoming Integrated Theatre Commands could realign resource flows, but the Army's land-centric imperatives will remain the anchor of the Indian defense market.

Vehicles held 28.76% of 2024 revenue as the Indian defense market size favored platforms such as main battle tanks, artillery carriers, and transport aircraft. High-altitude demands prompted the Zorawar light tank program tailored for Ladakh terrains. However, unmanned systems are set to outpace all other categories at a 7.35% CAGR. Recent military operations show that AI-enabled swarm drones proved cost-effective force multiplication, and the domestic drone market could reach USD 11 billion by 2030.

Training and protection systems are scaling alongside the Agnipath tour-of-duty model, which demands accelerated skill pipelines. C4ISR and electronic warfare (EW) suites gain prominence as multi-domain operations require unified situational awareness. Smart munitions and domestically produced ammunition address supply security as imports taper. Backed by dedicated doctrine, emerging space and cyber procurements compel legacy contractors to diversify portfolios or risk obsolescence in the evolving Indian defense market.

The India Defense Market Report is Segmented by Armed Forces (Air Force, Army, and Navy), Type (Personnel Training and Protection, C4ISR and Electronic Warfare, Vehicles, Weapons and Ammunition, Unmanned Systems, and Space and Cyber Systems), Domain (Land, Air, Naval, and More), and Procurement Nature (Indigenous Production and Foreign Procurement). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Hindustan Aeronautics Limited (HAL)

- Defence Research & Development Organisation (DRDO)

- Bharat Electronics Ltd.

- Bharat Dynamics Limited (BDL)

- Larsen & Toubro Ltd.

- Tata Advanced Systems Limited (Tata Group)

- Kalyani Strategic Systems Ltd. (Bharat Forge Limited)

- Mahindra & Mahindra Limited

- Adani Group

- Alpha Design Technologies Pvt Ltd.

- Goa Shipyard Limited

- Garden Reach Shipbuilders & Engineers Ltd (GRSE)

- Cochin Shipyard limited

- Swan Defence and Heavy Industries Limited

- Data Patterns (India) Ltd.

- Paras Defence and Space Technologies Limited

- Rafael Advanced Defense Systems Ltd.

- Israel Aerospace Industries Ltd.

- Airbus SE

- The Boeing Company

- Reliance Infrastructure Ltd.

- Mazagon Dock Shipbuilders Limited (MDL)

- Directorate of Ordnance (Coordination & Services)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding defense budget and localization drive

- 4.2.2 Accelerated investment in AI-enabled combat and autonomous swarm technologies

- 4.2.3 Escalating geopolitical tensions along the borders

- 4.2.4 Emergence of dual-use space assets driving C4ISR capability demand

- 4.2.5 Increased private sector participation enabled by liberalized FDI policies

- 4.2.6 Structural modernization of the Army, Navy, and Air Force

- 4.3 Market Restraints

- 4.3.1 Vulnerabilities in critical alloy and semiconductor supply chains

- 4.3.2 Inefficient and bureaucratic defense procurement framework

- 4.3.3 Cybersecurity breaches and IP theft are hindering indigenous R&D progress

- 4.3.4 High pension and salary expenditures limiting capital investment

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Armed Forces

- 5.1.1 Air Force

- 5.1.2 Army

- 5.1.3 Navy

- 5.2 By Type

- 5.2.1 Personnel Training and Protection

- 5.2.2 C4ISR and Electronic Warfare

- 5.2.3 Vehicles

- 5.2.4 Weapons and Ammunition

- 5.2.5 Unmanned Systems

- 5.2.6 Space and Cyber Systems

- 5.3 By Domain

- 5.3.1 Land

- 5.3.2 Air

- 5.3.3 Naval

- 5.3.4 Space

- 5.3.5 Cyber and Electromagnetic Spectrum

- 5.4 By Procurement Nature

- 5.4.1 Indigenous Production

- 5.4.2 Foreign Procurement

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Hindustan Aeronautics Limited (HAL)

- 6.4.2 Defence Research & Development Organisation (DRDO)

- 6.4.3 Bharat Electronics Ltd.

- 6.4.4 Bharat Dynamics Limited (BDL)

- 6.4.5 Larsen & Toubro Ltd.

- 6.4.6 Tata Advanced Systems Limited (Tata Group)

- 6.4.7 Kalyani Strategic Systems Ltd. (Bharat Forge Limited)

- 6.4.8 Mahindra & Mahindra Limited

- 6.4.9 Adani Group

- 6.4.10 Alpha Design Technologies Pvt Ltd.

- 6.4.11 Goa Shipyard Limited

- 6.4.12 Garden Reach Shipbuilders & Engineers Ltd (GRSE)

- 6.4.13 Cochin Shipyard limited

- 6.4.14 Swan Defence and Heavy Industries Limited

- 6.4.15 Data Patterns (India) Ltd.

- 6.4.16 Paras Defence and Space Technologies Limited

- 6.4.17 Rafael Advanced Defense Systems Ltd.

- 6.4.18 Israel Aerospace Industries Ltd.

- 6.4.19 Airbus SE

- 6.4.20 The Boeing Company

- 6.4.21 Reliance Infrastructure Ltd.

- 6.4.22 Mazagon Dock Shipbuilders Limited (MDL)

- 6.4.23 Directorate of Ordnance (Coordination & Services)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment