PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851790

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851790

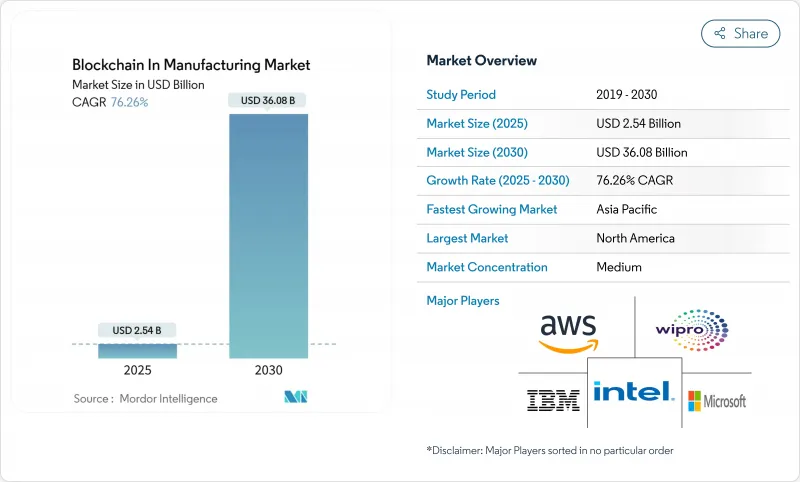

Blockchain In Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Blockchain In Manufacturing Market size is estimated at USD 2.54 billion in 2025, and is expected to reach USD 36.08 billion by 2030, at a CAGR of 76.26% during the forecast period (2025-2030).

Rising deployment of immutable ledgers for batch provenance, anti-counterfeiting, and equipment tokenization is accelerating the transition from pilot projects to enterprise-wide rollouts. Heightened regulatory scrutiny, especially under the Drug Supply Chain Security Act, is compelling manufacturers to adopt distributed ledgers that automate serialization and recall management. Equipment-as-a-service initiatives are unlocking new revenue streams, while cloud-based Blockchain-as-a-Service (BaaS) platforms lower entry barriers for small and mid-sized factories. Although fragmentation in standards and shortages of blockchain-skilled operational-technology talent temper near-term adoption, strategic partnerships between cloud hyperscalers and industrial OEMs are closing capability gaps.

Global Blockchain In Manufacturing Market Trends and Insights

Escalating Adoption of BaaS Across Discrete Manufacturing

Cloud-delivered BaaS now represents 61.8% of implementation preferences among discrete manufacturers, a share propelled by turnkey environments that eliminate the need for specialized node management. Microsoft's integration of blockchain telemetry into its Fabric analytics suite allows users to query production-line events alongside enterprise data, reducing system-integration time by 35%. Cost savings combine with simplified DevOps to ensure that BaaS gains traction in automotive, electronics, and industrial equipment factories that require rapid onboarding yet stringent uptime.

Supply-Chain Provenance and Traceability Mandates

The FDA extended its Food Traceability Rule deadline yet reaffirmed blockchain's suitability for immutable lot-level reporting requirements. Parallel EU Digital Product Passport rules reinforce the need for distributed records across every product lifecycle phase. Pharmaceutical, aerospace, and consumer electronics producers are embedding serialization data onto shared ledgers to automate recall, thereby trimming manual audit costs by 28%.

Fragmented Standards and Interoperability Gaps

The absence of universal data models forces suppliers to build costly middleware bridges for each trading partner. GS1 and ISO working groups are drafting common schemas, yet adoption lags fast-moving implementation deadlines. Consortium-based pilots in automotive and chemicals signal progress but remain pockets rather than norms.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Counterfeit Mitigation in High-Value Components

- Tokenization Enabling Equipment-as-a-Service Models

- Limited Blockchain Talent in OT Environments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Quality control and compliance tools are projected to post a 77.4% CAGR to 2030, outpacing logistics management despite the latter's 46% hold on the blockchain in manufacturing market share in 2024. Pharmaceutical firms running FDA serialization pilots report 30% faster deviation resolution when batch histories sit on a distributed ledger. Smart-contract workflows that auto-issue audit certificates replace paper record-keeping, cutting compliance hours by 40%. Second-wave applications include predictive maintenance logs and warranty adjudication, where immutable histories lower dispute rates. Counterfeit detection remains central as luxury-grade chemical tags feed authenticity hashes into public ledgers, enhancing consumer trust. As use cases multiply, the blockchain in the manufacturing market registers significant traction across both greenfield and brownfield plants.

Quality systems also form the backbone for emerging intellectual-property protection schemes in additive manufacturing, where zero-knowledge proofs confirm design compliance without revealing trade secrets. Electronic-component makers integrate on-device cryptographic signatures with the ledger, strengthening recall precision. This convergence of quality, compliance, and anti-counterfeiting accelerates enterprise interest in interoperable platforms, reinforcing the blockchain in the manufacturing market growth narrative.

Automotive factories dominated revenue with 31.2% in 2024, reflecting extensive part traceability obligations and mature Industry 4.0 investments. Nonetheless, life-sciences producers will expand the blockchain in the manufacturing market size for their segment at a 78.06% CAGR through 2030 as serialization, cold-chain tracking, and patient-level provenance become mandatory under global health regulations. Drug makers collaborating with IBM and Merck reported 25% faster recall execution during simulated audits. Aerospace and defense integrators adopt secure part genealogy ledgers for 3D-printed components, mitigating tampering risks. Consumer-electronics brands embed warranty tokens into products to streamline after-sales service, while food and beverage processors deploy farm-to-fork tracking to satisfy sustainability audits. Collectively, vertical diversification broadens the blockchain in the manufacturing industry footprint beyond early movers.

The Blockchain in Manufacturing Market Report is Segmented by Application (Logistics and Supply Chain Management, Counterfeit Management, Quality Control and Compliance, and More), End-User Vertical (Automotive, Aerospace and Defense, Pharmaceutical and Life Sciences, and More), Deployment Mode (On-Premises, Cloud/Blockchain-as-a-Service, and Hybrid/Edge), Blockchain Type (Public, Private/Permissioned, and More), and Geography.

Geography Analysis

North America held 44.3% of 2024 revenue owing to FDA mandates, established cloud infrastructure, and strong venture capital backing for ledger startups. Pharmaceutical serialization and aerospace part pedigree requirements drove early proofs that have since scaled to multi-plant deployments. State-level incentives further supported SME adoption.

Asia Pacific registers the highest 78.34% CAGR forecast between 2025 and 2030, reflecting sweeping digitization initiatives such as China's industrial blockchain pilots and Japan's Society 5.0 smart-factory roadmap. The Asian Development Bank's Project Tridecagon showcases regional commitment to inter-bank distributed settlements that align with manufacturing export-credit flows. India's electronics clusters and South Korea's battery-supply chain agreements add momentum, catalyzing adoption by Tier-2 suppliers.

Europe emerges as a sustainability-centric adopter, leveraging Digital Product Passports to document carbon footprints and circular-economy metrics. Germany's automotive OEMs employ joint ledgers to track recycled steel content, while France's aerospace primes adopt blockchain to manage additive-manufacturing powders. Nordic manufacturers power permissioned networks with hydro and wind energy, addressing ESG expectations. Cross-border data-spaces projects promote interoperability, suggesting that regional implementations will converge under common governance as the blockchain in the manufacturing market matures globally.

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Oracle Corporation

- Amazon Web Services Inc.

- Accenture PLC

- Wipro Limited

- Infosys Ltd

- Intel Corporation

- Advanced Micro Devices Inc.

- VeChain Technology

- Chronicled Inc.

- SyncFab

- Siemens AG

- Honeywell International Inc.

- General Electric

- R3 LLC

- ConsenSys

- Kaleido

- BlockApps Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating adoption of BaaS across discrete manufacturing

- 4.2.2 Supply-chain provenance and traceability mandates

- 4.2.3 Demand for counterfeit mitigation in high-value components

- 4.2.4 Tokenisation enabling equipment-as-a-service models

- 4.2.5 Integration with additive manufacturing for secure part genealogy

- 4.2.6 Privacy-preserving zero-knowledge-proof pilots for IP protection

- 4.3 Market Restraints

- 4.3.1 Fragmented standards and interoperability gaps

- 4.3.2 Limited blockchain talent in OT environments

- 4.3.3 Rising energy-use concerns for on-chain traceability

- 4.3.4 Uncertainty around post-quantum security requirements

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pandemic and Geopolitical Impact Assessment

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Logistics and Supply Chain Management

- 5.1.2 Counterfeit Management

- 5.1.3 Quality Control and Compliance

- 5.1.4 Predictive Maintenance and Asset Tracking

- 5.1.5 Smart Contracts for Procurement

- 5.1.6 Other Applications

- 5.2 By End-user Vertical

- 5.2.1 Automotive

- 5.2.2 Aerospace and Defense

- 5.2.3 Pharmaceutical and Life Sciences

- 5.2.4 Consumer Electronics

- 5.2.5 Industrial Machinery

- 5.2.6 Food and Beverage

- 5.2.7 Other Verticals

- 5.3 By Deployment Mode

- 5.3.1 On-premises

- 5.3.2 Cloud/Blockchain-as-a-Service (BaaS)

- 5.3.3 Hybrid/Edge

- 5.4 By Blockchain Type

- 5.4.1 Public

- 5.4.2 Private/Permissioned

- 5.4.3 Consortium

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Partnerships

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corporation

- 6.4.3 SAP SE

- 6.4.4 Oracle Corporation

- 6.4.5 Amazon Web Services Inc.

- 6.4.6 Accenture PLC

- 6.4.7 Wipro Limited

- 6.4.8 Infosys Ltd

- 6.4.9 Intel Corporation

- 6.4.10 Advanced Micro Devices Inc.

- 6.4.11 VeChain Technology

- 6.4.12 Chronicled Inc.

- 6.4.13 SyncFab

- 6.4.14 Siemens AG

- 6.4.15 Honeywell International Inc.

- 6.4.16 General Electric

- 6.4.17 R3 LLC

- 6.4.18 ConsenSys

- 6.4.19 Kaleido

- 6.4.20 BlockApps Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment