PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940566

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940566

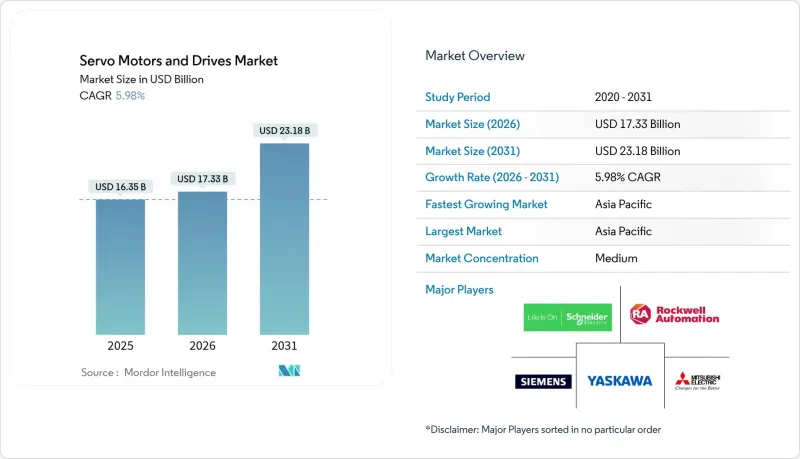

Servo Motors And Drives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The servo motors and drives market is expected to grow from USD 16.35 billion in 2025 to USD 17.33 billion in 2026 and is forecast to reach USD 23.18 billion by 2031 at 5.98% CAGR over 2026-2031.

Growth stemmed from factories upgrading to networked motion systems that combine silicon-carbide power electronics, digital twin simulation and collaborative robotics. Semiconductor plants and precision packaging lines adopted linear designs to eliminate mechanical conversions, while automotive producers invested in mid-voltage, high-power solutions for battery and e-axle assembly. Energy-efficiency legislation prompted manufacturers to replace induction units with IE4-class servo packages, and the expanding 800 V electric-vehicle architecture spurred demand for higher-voltage drives. Intensifying competition arrived from silicon-carbide specialists and cybersecurity vendors, pressuring traditional incumbents to blend mechanical expertise with digital intelligence.

Global Servo Motors And Drives Market Trends and Insights

Rapid industrial automation and smart-factory rollout

During 2024, automotive groups in Germany connected multi-axis robotic cells to digital-twin platforms, cutting line-change times and increasing throughput. Closure Systems International lifted overall equipment effectiveness to 97.5% after installing FANUC servo-driven lines that dropped unplanned downtime to 2.5%. EtherCAT-enabled drives synchronised motion within microseconds, supporting flexible manufacturing and paving the way for 5G-based machine coordination.

Rising adoption of collaborative and mobile robotics

Cobots require compact, safety-rated actuators with integrated torque sensing. Yaskawa's HC series met ISO/TS 15066:2016 force limits through embedded monitoring, allowing direct human interaction on assembly lines. High-torque-density motors supplied by Kollmorgen powered almost 1 million robotic joints worldwide, demonstrating the servo motors and drives market's shift toward lighter, user-friendly platforms.

High upfront cost vs. induction/stepper alternatives

Small manufacturers in India and Southeast Asia compared premium servo packages with variable-frequency-drive induction sets and frequently chose the latter. Yet studies by Packaging World showed lifetime energy and maintenance savings tilting favour back toward servos, with annual operating cost dropping from USD 7,320 to USD 388.8 when pneumatics were replaced by electric actuators.

Other drivers and restraints analyzed in the detailed report include:

- Stringent global and regional energy-efficiency mandates

- Electrification push in automotive manufacturing and EV platforms

- Supply-chain risk for high-grade rare-earth permanent magnets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AC units kept 65.02% of the servo motors and drives market in 2025 because three-phase grids and mature manufacturing lines favoured rotary designs. Linear variants captured semiconductor packaging, lithography and high-speed cartooning, expanding at 9.64% CAGR. Delkor's cartoning lines achieved higher throughputs by eliminating rotary-to-linear conversions.

Linear models extended beyond simple positioning. Tolomatic servo presses delivered 80% efficiency versus 50% for hydraulics, attracting packaging firms that needed hygienic, oil-free motion. Platform suppliers responded with distributed drives such as Rockwell Automation's ArmorKinetix, cutting cabling 90% and installation time 30%.

Low-voltage installations held 61.88% share but the 1-35 kV class grew 7.05% annually as plants adopted higher-voltage architectures to reduce cable size and heat. Arrow Electronics highlighted silicon-carbide MOSFETs running at higher switching frequencies with lower losses. Medium-voltage drives supported 100 kW-plus machine tools used for EV motor housings, matching growing torque demands.

Siemens introduced MICRO-DRIVE extra-low-voltage units for autonomous mobile robots that need safe 24-48 V levels. Conversely, 800 V EV lines deployed mid-voltage servos to shrink conductor diameters and lower resistive loss, holding a niche but rising share in the servo motors and drives market.

The Servo Motors and Drives Market Report is Segmented by Product Type (Motor, and Drive), Voltage Range (Low Voltage <=1kV, Medium Voltage 1kV-35kV, and High Voltage >35kV), End-User Industry (Automotive and EV Manufacturing, Oil and Gas, Healthcare and Medical Devices, Packaging and Labelling, and More), Power Rating (<=1kW, 1kW-5kW, 5kW-15kW, and >15kW), and Geography.

Geography Analysis

Asia-Pacific captured 45.92% of global revenue in 2025 on the back of Chinese electronics production, Japanese technology leadership and India's factory expansions. Regional growth remained the fastest at 7.62% CAGR as ASEAN nations incentivised automation to raise competitiveness. China's dominance in rare-earth supply lowered local costs but exposed foreign buyers to export controls. Japan's Harmonic Drive Systems aimed for JPY 90 billion net sales by FY 2026, reinforcing the technology cluster in Tokyo and Nagano.

North America increased its reshoring programmes to improve supply resilience. Mitsubishi Electric's USD 143.5 million compressor plant in Kentucky illustrated the trend toward localised production and shorter lead times. Hitachi's purchase of Joliet Electric Motors broadened aftermarket services, supporting lifecycle value across installed fleets. Rising collaborative-robot utilisation in the United States offset softness in heavy industry.

Europe focused on decarbonisation and digital-twin analytics. IE4 mandates spurred retrofits in Germany and the Nordics, while cybersecurity concerns prompted audits after CISA flagged vulnerabilities in ABB Drive Composer and Rockwell PowerFlex firmware. Medium-voltage drives penetrated automotive clusters in Bavaria and Piedmont as OEMs migrated to 800 V battery lines, sustaining mid-single-digit growth despite macroeconomic pressures.

- Yaskawa Electric Corporation

- Mitsubishi Electric Corporation

- Siemens AG

- Schneider Electric SE

- Rockwell Automation, Inc.

- ABB Ltd.

- Delta Electronics, Inc.

- FANUC Corporation

- Kollmorgen Corporation (Regal Rexnord Corporation)

- Bosch Rexroth AG

- Panasonic Holdings Corporation

- Nidec Corporation

- Omron Corporation

- Oriental Motor Co., Ltd.

- Lenze SE

- Parker-Hannifin Corporation

- Inovance Technology Co., Ltd.

- Moog Inc.

- WEG Equipamentos El-tricos S.A.

- Emerson Electric Co.

- AMETEK, Inc.

- TECO Electric & Machinery Co., Ltd.

- Nanotec Electronic GmbH & Co. KG

- SANYO DENKI Co., Ltd.

- Fuji Electric Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid industrial automation and smart-factory rollout

- 4.2.2 Rising adoption of collaborative and mobile robotics

- 4.2.3 Stringent global and regional energy-efficiency mandates

- 4.2.4 Electrification push in automotive manufacturing and EV platforms

- 4.2.5 Silicon-carbide power modules boosting servo-drive efficiency

- 4.2.6 Digital-twin-enabled predictive sizing and optimisation of servo systems

- 4.3 Market Restraints

- 4.3.1 High upfront cost vs. induction/stepper alternatives

- 4.3.2 Proliferation of low-cost stepper and VFD-controlled induction motors

- 4.3.3 Supply-chain risk for high-grade rare-earth permanent magnets

- 4.3.4 Cyber-vulnerabilities in networked servo drives causing downtime

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact Assessment of Key Stakeholders

- 4.9 Key Use Cases and Case Studies

- 4.10 Impact on Macroeconomic Factors of the Market

- 4.11 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Motor

- 5.1.1.1 AC Servo Motor

- 5.1.1.2 DC Brushless Servo Motor

- 5.1.1.3 Brushed DC Servo Motor

- 5.1.1.4 Linear Servo Motor

- 5.1.2 Drive

- 5.1.2.1 AC Servo Drive

- 5.1.2.2 DC Servo Drive

- 5.1.2.3 Adjustable / Multi-axis Servo Drive

- 5.1.1 Motor

- 5.2 By Voltage Range

- 5.2.1 Low Voltage (<=1 kV)

- 5.2.2 Medium Voltage (1 kV-35 kV)

- 5.2.3 High Voltage (>35 kV)

- 5.3 By End-user Industry

- 5.3.1 Automotive and EV Manufacturing

- 5.3.2 Oil and Gas (Up-, Mid-, Down-stream)

- 5.3.3 Healthcare and Medical Devices

- 5.3.4 Packaging and Labelling

- 5.3.5 Semiconductor and Electronics

- 5.3.6 Chemicals and Petrochemicals

- 5.3.7 Food and Beverage

- 5.3.8 Other Industries (Textile, Printing, etc.)

- 5.4 By Power Rating

- 5.4.1 ?1 kW

- 5.4.2 1 kW-5 kW

- 5.4.3 5 kW-15 kW

- 5.4.4 >15 kW

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Yaskawa Electric Corporation

- 6.4.2 Mitsubishi Electric Corporation

- 6.4.3 Siemens AG

- 6.4.4 Schneider Electric SE

- 6.4.5 Rockwell Automation, Inc.

- 6.4.6 ABB Ltd.

- 6.4.7 Delta Electronics, Inc.

- 6.4.8 FANUC Corporation

- 6.4.9 Kollmorgen Corporation (Regal Rexnord Corporation)

- 6.4.10 Bosch Rexroth AG

- 6.4.11 Panasonic Holdings Corporation

- 6.4.12 Nidec Corporation

- 6.4.13 Omron Corporation

- 6.4.14 Oriental Motor Co., Ltd.

- 6.4.15 Lenze SE

- 6.4.16 Parker-Hannifin Corporation

- 6.4.17 Inovance Technology Co., Ltd.

- 6.4.18 Moog Inc.

- 6.4.19 WEG Equipamentos El-tricos S.A.

- 6.4.20 Emerson Electric Co.

- 6.4.21 AMETEK, Inc.

- 6.4.22 TECO Electric & Machinery Co., Ltd.

- 6.4.23 Nanotec Electronic GmbH & Co. KG

- 6.4.24 SANYO DENKI Co., Ltd.

- 6.4.25 Fuji Electric Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment