PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851860

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851860

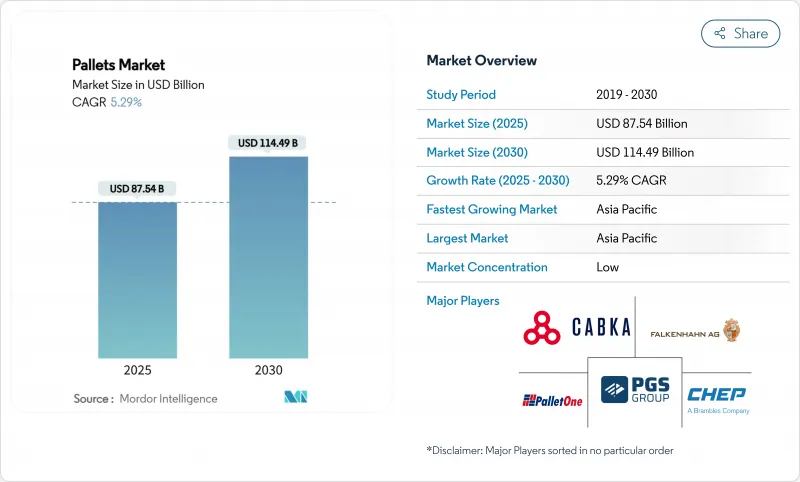

Pallets - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The pallets market size stood at USD 87.54 billion in 2025 and is forecast to reach USD 114.49 billion by 2030, reflecting a 5.29% CAGR during the period.

Robust e-commerce activity, automation-ready warehouse design and global alignment with ISPM-15 standards underpin demand. Companies are prioritizing block pallets to avoid costly recalibration of automated storage and retrieval systems, while plastics gain share in food, beverage and pharmaceutical chains that require non-porous contact surfaces. Regional pooling models are scaling rapidly in Asia-Pacific, helped by cross-border trade initiatives that favor certified, track-and-trace assets. At the same time, lumber price volatility and weak reverse-logistics for plastics in parts of South America and Africa hold growth below potential. Despite these frictions, technology-enabled pooling and bio-composite innovations continue to open cost-efficient and sustainable pathways for users.

Global Pallets Market Trends and Insights

E-commerce fulfilment centres driving block-pallet adoption

High-velocity omnichannel warehouses are standardising on block formats to secure four-way access and structural integrity. Deviation from the reference block specification can trigger USD 50,000-200,000 recalibration costs per site, locking operators into dimensionally consistent units.Throughput improvements of up to 30% and robotic mixed-case palletising gains of 288% have been recorded, reinforcing the preference for block designs.

Regulatory push for ISPM-15 pallets fuelling pooling in Asia-Pacific

The ISPM-15 framework now spans 182 countries and levies roughly USD 45 million in annual penalties, forcing shippers toward certified pooling networks that guarantee heat-treated assets. Pooling volumes in Asia-Pacific have risen 23% since 2024, aided by digital traceability devices that keep compliance data linked to each pallet.

Volatile lumber prices from US-Canada tariffs

A 14.54% duty on Canadian softwood swings wood input costs by as much as 40% per quarter, forcing manufacturers to hedge purchases and compress margins. The exposure encourages investment in alternative fibres such as corn stover panels now in pilot production.

Other drivers and restraints analyzed in the detailed report include:

- Hygienic plastic pallets demand from FSMA and EU 1935/2004 compliance

- RTP uptake in pharma cold-chain logistics across Oceania and India

- Weak reverse-logistics for plastic pallets in South America and Africa

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wood retained 69.45% of pallets market share in 2024, underpinned by a USD 8-12 unit price advantage. However, tariff-driven cost inflation, ISPM-15 heat-treatment fees and customer decarbonisation targets are eroding this lead. Brambles sources 78% certified timber and plants two trees for each harvested one to sustain its pool, yet users still seek lighter, recyclable options.

Plastic pallets are tracking a 7.2% CAGR through 2030 as hygiene and reusability requirements mount. Adoption accelerates where total cost of ownership offsets higher acquisition prices, especially in pharma and food sectors bound by strict contact-material rules. Bio-composites derived from rice husk and corn stover offer biodegradability within two months, meeting both regulatory and corporate carbon objectives. These attributes are gaining traction across Asia-Pacific, where agricultural residues are abundant and waste-reduction policies supportive.

Block formats commanded 55.34% of the pallets market in 2024 due to four-way access and robotic compatibility. Automated fulfilment floors report 15-20% faster handling relative to stringer alternatives.

Customized pallets are growing 7.5% CAGR as operators demand RFID inserts, sensor slots and deck surfaces tailored to specific conveyor coefficients. Hybrid builds that marry wooden decks to plastic runners balance friction optimisation with cost, supporting the rising automation installed base in grocery and apparel distribution.

The Pallets Market Report is Segmented by Material Type (Wood, Plastic, and More), Design (Block, Stringer, Customized), Pallet Type (Nestable, Rackable, Stackable, Other Pallet Types), Load Capacity (Light-Duty, and More, End-User Industry (Food and Beverage, Chemical, Pharmaceutical and Healthcare, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led with 45.12% of pallets market share in 2024 and is expected to post a 6.4% CAGR. Manufacturing hub consolidation in China and India, plus e-commerce acceleration in Southeast Asia, continue to lift volume. Loscam's pool expansion illustrates how cross-border asset rotation lowers repositioning miles and reduces imbalances.

North America ranks second as automation retrofits and near-shoring policy drive pallet upgrades. Lumber tariffs inject volatility but also promote alternative fibres and plastic adoption. Mexico's deeper integration into US supply chains generates fresh demand for ISPM-15-certified pallets serving both domestic and export lanes.

Europe's market benefits from circular-economy law, carbon pricing and high labour costs that favour automation. Implementation of reusable pallet schemes compresses waste, while bio-composite pilots in Germany and the Nordics test next-generation materials. Middle East, Africa and South America exhibit high latent potential yet remain constrained by reverse-logistics and standards fragmentation, although national logistics plans in Saudi Arabia and Brazil point to upside beyond 2027.

- Brambles Ltd (CHEP)

- PalletOne Inc.

- CABKA Group GmbH

- Craemer Holding GmbH

- Schoeller Allibert

- Rehrig Pacific Co.

- Loscam International Holdings

- UFP Industries Inc.

- ORBIS Corporation (Menasha)

- Pallet Logistics of America

- PECO Pallet LLC

- Falkenhahn AG

- World Steel Pallet Co. Ltd.

- Millwood Inc.

- PGS Group (Palettes Gestion Services)

- Euroblock Pallets

- Beijing LuckyStar Logistics

- Interpak Pallets

- Palletways Group

- Polymer Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Fulfilment Centres Driving Block-Pallet Adoption in North America and Europe

- 4.2.2 Regulatory Push for ISPM-15 Pallets Fuelling Pooling in Asia-Pacific

- 4.2.3 Hygienic Plastic Pallets Demand from FSMA and EU 1935/2004-Compliant FandB Plants

- 4.2.4 RTP Uptake in Pharma Cold-Chain Logistics across Oceania and India

- 4.2.5 Warehouse Robotics Requiring Dimensionally Consistent Composite Pallets

- 4.2.6 Net-Zero Targets Accelerating Bio-Composite Rice-Husk Pallets in China and SE-Asia

- 4.3 Market Restraints

- 4.3.1 Volatile Lumber Prices from US-Canada Tariffs

- 4.3.2 Weak Reverse-Logistics for Plastic Pallets in South America and Africa

- 4.3.3 High Cost and Weight Limiting Metal Pallets in EMEA Air-Freight

- 4.3.4 Fragmented ASEAN Standards Hindering Pooling Scalability

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Sustainability and Recycling/Reusability of Pallets

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Geopolitical Impact Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Wood

- 5.1.2 Plastic

- 5.1.3 Metal

- 5.1.4 Corrugated Paper/Composite

- 5.2 By Design

- 5.2.1 Block

- 5.2.2 Stringer

- 5.2.3 Customized

- 5.3 By Pallet Type

- 5.3.1 Nestable

- 5.3.2 Rackable

- 5.3.3 Stackable

- 5.3.4 Other Pallet Types

- 5.4 By Load Capacity

- 5.4.1 Light - Duty Pallets

- 5.4.2 Medium - Duty Pallets

- 5.4.3 High - Duty Pallets

- 5.5 By End-User Industry

- 5.5.1 Food and Beverage

- 5.5.2 Chemical

- 5.5.3 Pharmaceutical and Healthcare

- 5.5.4 Retail and E-Commerce

- 5.5.5 Logistics and Warehousing

- 5.5.6 Automotive

- 5.5.7 Other Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Egypt

- 5.6.4.2.4 Rest of Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Brambles Ltd (CHEP)

- 6.4.2 PalletOne Inc.

- 6.4.3 CABKA Group GmbH

- 6.4.4 Craemer Holding GmbH

- 6.4.5 Schoeller Allibert

- 6.4.6 Rehrig Pacific Co.

- 6.4.7 Loscam International Holdings

- 6.4.8 UFP Industries Inc.

- 6.4.9 ORBIS Corporation (Menasha)

- 6.4.10 Pallet Logistics of America

- 6.4.11 PECO Pallet LLC

- 6.4.12 Falkenhahn AG

- 6.4.13 World Steel Pallet Co. Ltd.

- 6.4.14 Millwood Inc.

- 6.4.15 PGS Group (Palettes Gestion Services)

- 6.4.16 Euroblock Pallets

- 6.4.17 Beijing LuckyStar Logistics

- 6.4.18 Interpak Pallets

- 6.4.19 Palletways Group

- 6.4.20 Polymer Logistics

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment