PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910642

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910642

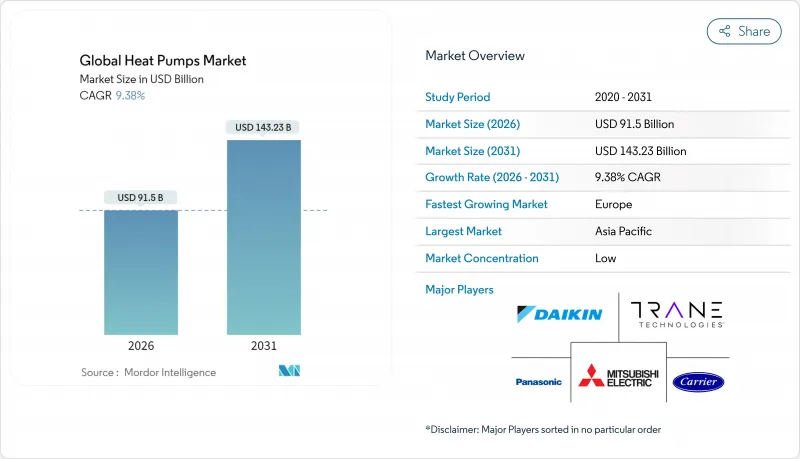

Global Heat Pumps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The heat pump market was valued at USD 83.66 billion in 2025 and estimated to grow from USD 91.5 billion in 2026 to reach USD 143.23 billion by 2031, at a CAGR of 9.38% during the forecast period (2026-2031).

Decarbonization mandates in Europe and North America, large federal and provincial incentive packages, and ever-larger utility-scale projects positioned the heat pump market as the leading replacement pathway for fossil-fuel-based space and water heating solutions. China's integrated manufacturing base held costs down while inverter-driven compressor advances narrowed performance gaps in sub-zero environments, setting the stage for rapid uptake in colder regions. Supply-chain localization efforts in the United States and Poland mitigated tariff and freight risks while growing "Heat-as-a-Service" finance models addressed steep upfront installation costs that had slowed adoption in existing buildings.

Global Heat Pumps Market Trends and Insights

Government decarbonization incentives and mandates

Aggressive policy frameworks created binding demand for heat pumps by tying building codes and subsidy levels directly to renewable heat outcomes. The US Inflation Reduction Act offered combined federal tax credits and state rebates as high as USD 14,000 per household, while Germany enforced its 65% renewable-heat requirement for all new heating systems starting in 2024. Canada's Oil to Heat Pump Affordability Program provided up to CAD 15,000 (USD 11,100) to lower-income homes, and the UK's Boiler Upgrade Scheme paid grants of up to GBP 7,500 (USD 9,400). These measures set artificial demand floors that shielded manufacturers from macroeconomic slowdowns and accelerated market penetration.

Electrification-driven HVAC replacement cycles

Local greenhouse gas caps in large cities condensed typical 15-20 year HVAC replacement intervals into fast-tracked retrofits that replace failing boilers with high-efficiency heat pumps. New York City's Local Law 97 triggered projects such as the retrofit of 345 Hudson Street, combining heat pumps and waste-heat recovery to hit a 70% emissions-cut target by 2030. Massachusetts Utilities launched the first US geothermal network in Framingham, connecting 135 customers in 2024 and demonstrating district-level electrification potential.

High installation and retrofitting costs in existing buildings

Total installed pricing diverged sharply by geography. Typical German row-house retrofits exceeded EUR 30,000 (USD 32,400), double France's post-subsidy cost because of higher labor expenses and stricter permitting rules. A New York multifamily case study showed that electrical panel upgrades alone amounted to 40% of the project cost, highlighting infrastructure hurdles that incentives cannot fully offset.

Other drivers and restraints analyzed in the detailed report include:

- Rapid cost declines in inverter-driven compressors

- Cold-climate heat pump technology breakthroughs

- Skilled installer shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air-source units held 73.12% heat pump market share in 2025 because of lower installation costs and product familiarity. However, the ground/geothermal category is forecast to post a 12.35% CAGR, the fastest within the spectrum, as utilities pilot networked loops such as the USD 14 million Framingham project that connected 135 customers in 2024. Advances in direct-expansion boreholes and shared ground loops improved COP stability above 4.0, increasing appeal in dense urban infill.

Air-source manufacturers continued to refine low-ambient algorithms, cutting performance drop-off at -20°F and unlocking northern growth. Meanwhile, utilities and large developers viewed geothermal systems as a hedge against grid-peak constraints because output is decoupled from outdoor temperature swings. These dynamics suggest gradual rebalancing, yet the heat pump market will still see air-source units dominate unit volumes through the forecast horizon.

Residential-scale systems up to 10 kW contributed 45.92% of 2025 shipments, reflecting the breadth of single-family adoption supported by consumer rebates. The above-30 kW class, however, is projected to outpace all others at a 12.18% CAGR as district heating and industrial process projects proliferate. Denmark's 70 MW Esbjerg seawater plant and Hamburg's 60 MW wastewater initiative highlight the momentum toward centralized mega-scale assets.

Small-capacity uptake will remain elevated because of standardized equipment and simplified permitting. Large-capacity momentum underscores the widening application perimeter that includes warehouses, food processing, and municipal networks aiming for carbon-neutral heat.

Heat Pump Market is Segmented by Source Type (Air-Source, Water-Source, and Ground/Geothermal Source), Rated Capacity (Up To 10 KW, 10-20 KW, and More), System Design (Split System, Monobloc, and Hybrid Heat Pump), End-User (Residential, Commercial, and More), Application (Space Heating and Cooling, Water Heating, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained a commanding 38.05% portion of the heat pump market in 2025, underpinned by China's 13% domestic sales growth and its 40% share of global production capacity, which yielded 12% unit-cost declines from factory automation gains. Japan's cautious 1% volume uptick and South Korea's compressor technology leadership stabilized regional shipments, while India remained nascent because tropical ambient conditions limited efficiency advantages for traditional designs.

Europe is on a rebound path, with an 10.92% CAGR projected after a 50% sales dip in early 2024 when Germany's heating-law debate dampened consumer confidence. France committed to producing 1 million units per year domestically, and Denmark showcased flagship district-scale projects, including the Esbjerg seawater plant, as part of its fossil-free-by-2030 pledge. The United Kingdom trailed installation targets despite rich GBP 7,500 grants, underscoring the role of infrastructure and skills barriers over pure economics.

North America entered a policy-assisted growth cycle after initial softness: US year-over-year sales climbed 15% by November 2024 following the Inflation Reduction Act incentives, while Canada processed more than 13,000 subsidy applications concentrated in Atlantic provinces. Supply-chain reshoring efforts, including Mitsubishi Electric's compressor factory and the Daikin-Copeland joint venture, aim to offset projected USD 250-275 million tariff exposure by localizing critical components.

- Daikin Industries, Ltd.

- Mitsubishi Electric Corporation

- Panasonic Holdings Corporation

- Trane Technologies plc

- Carrier Global Corporation

- NIBE Industrier AB

- Glen Dimplex Group

- Viessmann Climate Solutions SE

- Stiebel Eltron GmbH & Co. KG

- Midea Group Co., Ltd.

- Guangdong Gree Electric Appliances Inc. of Zhuhai

- Haier Smart Home Co., Ltd.

- Bosch Thermotechnology GmbH (Robert Bosch GmbH)

- LG Electronics Inc.

- Lennox International Inc.

- Ariston Holding N.V. (Ariston Group)

- Samsung Electronics Co., Ltd.

- Rheem Manufacturing Company

- Johnson Controls International plc

- Viomi Technology Co., Ltd.

- A. O. Smith Corporation

- Ecoforest Geotermia S.L.

- WaterFurnace International, Inc. (NIBE Group)

- Danfoss A/S

- Vaillant GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government decarbonization incentives and mandates

- 4.2.2 Electrification-driven HVAC replacement cycles

- 4.2.3 Rapid cost declines in inverter-driven compressors

- 4.2.4 Grid-interactive heat pumps enabling demand-response revenue

- 4.2.5 Cold-climate heat pump technology breakthroughs

- 4.2.6 Heat-as-a-Service business models unlocking financing

- 4.3 Market Restraints

- 4.3.1 High installation and retrofitting costs in existing buildings

- 4.3.2 Skilled installer shortage

- 4.3.3 Electrical-panel and grid-capacity constraints in older housing stock

- 4.3.4 Competitive risk from hybrid hydrogen boilers in specific countries

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Source Type

- 5.1.1 Air-Source

- 5.1.1.1 Air-to-Air

- 5.1.1.2 Air-to-Water

- 5.1.2 Water-Source

- 5.1.2.1 Surface Water

- 5.1.2.2 Open Loop

- 5.1.3 Ground / Geothermal Source

- 5.1.3.1 Closed Loop Vertical

- 5.1.3.2 Closed Loop Horizontal

- 5.1.3.3 Direct Expansion

- 5.1.1 Air-Source

- 5.2 By Rated Capacity

- 5.2.1 Up to 10 kW

- 5.2.2 10-20 kW

- 5.2.3 20-30 kW

- 5.2.4 Above 30 kW

- 5.3 By System Design

- 5.3.1 Split System

- 5.3.2 Monobloc

- 5.3.3 Hybrid Heat Pump

- 5.4 By End-User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.4.4 Institutional

- 5.5 By Application

- 5.5.1 Space Heating and Cooling

- 5.5.2 Water Heating

- 5.5.3 District Heating

- 5.5.4 Process and Industrial Heating

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 ASEAN

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Daikin Industries, Ltd.

- 6.4.2 Mitsubishi Electric Corporation

- 6.4.3 Panasonic Holdings Corporation

- 6.4.4 Trane Technologies plc

- 6.4.5 Carrier Global Corporation

- 6.4.6 NIBE Industrier AB

- 6.4.7 Glen Dimplex Group

- 6.4.8 Viessmann Climate Solutions SE

- 6.4.9 Stiebel Eltron GmbH & Co. KG

- 6.4.10 Midea Group Co., Ltd.

- 6.4.11 Guangdong Gree Electric Appliances Inc. of Zhuhai

- 6.4.12 Haier Smart Home Co., Ltd.

- 6.4.13 Bosch Thermotechnology GmbH (Robert Bosch GmbH)

- 6.4.14 LG Electronics Inc.

- 6.4.15 Lennox International Inc.

- 6.4.16 Ariston Holding N.V. (Ariston Group)

- 6.4.17 Samsung Electronics Co., Ltd.

- 6.4.18 Rheem Manufacturing Company

- 6.4.19 Johnson Controls International plc

- 6.4.20 Viomi Technology Co., Ltd.

- 6.4.21 A. O. Smith Corporation

- 6.4.22 Ecoforest Geotermia S.L.

- 6.4.23 WaterFurnace International, Inc. (NIBE Group)

- 6.4.24 Danfoss A/S

- 6.4.25 Vaillant GmbH

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-need Assessment