PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910656

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910656

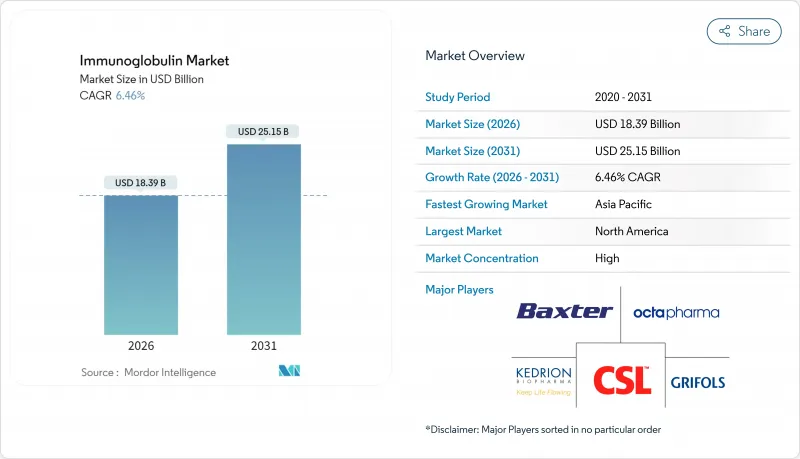

Immunoglobulin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The immunoglobulin market was valued at USD 17.27 billion in 2025 and estimated to grow from USD 18.39 billion in 2026 to reach USD 25.15 billion by 2031, at a CAGR of 6.46% during the forecast period (2026-2031).

Robust growth reflects widening use of plasma-derived and recombinant immunoglobulin therapies for primary immunodeficiency diseases (PID), chronic inflammatory demyelinating polyneuropathy (CIDP), and several hematological and neurological disorders. IgG formulations dominate because of their long half-life and broad clinical utility, while IgM and subcutaneous products are advancing fastest as manufacturers refine purification processes and develop high-concentration 20% solutions. Demand strength is amplified by sustained investments that lift global plasma-fractionation capacity, increasing clinical adoption in Asia-Pacific, and the shift to home-based care models that favor subcutaneous self-administration. On the supply side, structural barriers such as donor-eligibility rules, cold-chain logistics, and high capital costs reinforce the competitive positions of integrated producers.

Global Immunoglobulin Market Trends and Insights

Rising prevalence of PID

Global PID diagnosis has climbed to roughly 1 in 1,200 live births, propelled by wider genetic testing and stronger clinical awareness. Substantial unmet need remains: pooled analyses show 67.7% pneumonia prevalence among common variable immunodeficiency patients and 59.0% upper-respiratory infection prevalence, emphasizing the indispensable role of lifelong IgG replacement. Rising detection rates in developing regions are unlocking new patient pools, while health-economic data indicate hospitalizations for severe infections average USD 122,739-heightening payer incentives for prophylactic immunoglobulin therapy. Consequently, the immunoglobulin market enjoys durable demand as health systems shift toward prevention.

Growing IVIG use in neurology (CIDP)

Seventy-six percent of treatment-naive CIDP patients improve clinically after IVIG therapy. FDA approval of GAMMAGARD LIQUID for adults with CIDP in 2024 legitimized immunoglobulin as a front-line neurological therapy. Long-term studies confirm stable strength and motor function when patients transition from intravenous to subcutaneous dosing; 16 of 17 patients preferred home-based regimens. Expanded neurological protocols widen revenue streams and reinforce product pipelines.

High therapy cost & reimbursement gaps

Median IVIG spend sits at USD 133,334 over two years for CIDP, dwarfing USD 3,101 for steroid-only care. Insurance coverage can require stringent diagnostic proof, delaying therapy initiation. Global price disparities compel physicians in low-income regions to ration doses, potentially limiting the immunoglobulin market's full addressable population.

Other drivers and restraints analyzed in the detailed report include:

- Expanded plasma-fractionation capacity

- Emerging recombinant/plant-based Ig platforms

- Stringent donor-screening regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

IgG led with 67.88% immunoglobulin market share in 2025 due to its pharmacokinetic advantages and broad label coverage. IgM's 7.12% CAGR signals rising clinical acceptance for early-stage infection management and oncological indications. Yield-enhancement protocols-such as ADMA Biologics' FDA-filed supplement-promise a 20% uptick in IgG output, which may ease cost pressures. IgA therapies target mucosal immunity for selective deficiencies, while niche IgE products serve severe allergic conditions. Methodologies that achieve 95% purity and 90% yield in IgG through bathophenanthroline complexes underscore ongoing process intensification, underpinning sustained leadership of IgG in the immunoglobulin market.

Second-generation chromatography resins and improved virus-inactivation steps also benefit IgM by delivering greater consistency, fueling the fastest segment growth. Research into IgD's immunoregulatory role could eventually seed new subsegments, although commercial relevance remains nascent. Across all classes, tighter pharmacovigilance and post-marketing surveillance support broader payer acceptance and facilitate life-cycle extensions such as higher-concentration or co-formulated options.

The Immunoglobulin Market Report is Segmented by Product (IgG, Iga, Igm, Ige, Igd), Mode of Delivery (Intravenous, Subcutaneous, Intramuscular), Application (Hypogammaglobulinemia, CIDP, Primary Immunodeficiency Disease, Myasthenia Gravis, ITP, Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 43.85% of the immunoglobulin market in 2025, reflecting dense plasma-collection infrastructure, clear Medicare reimbursement, and rapid uptake of subcutaneous formulations. The United States alone hosted over 1,000 plasma centers in 2025, ensuring domestic supply resiliency even as donor-screening rules tighten. CSL Behring's 15% sales surge in the first half of 2025 validated persistent clinical demand. Policy momentum-such as bipartisan support for the Plasma Donation Modernization Act-should further streamline donor recruitment.

Asia-Pacific is the fastest-expanding region at 7.22% CAGR. Indonesia's forthcoming Karawang fractionator will lessen import reliance, while Japan sponsors region-specific studies of Takeda's subcutaneous TAK-771 to address local PID populations. China's environment is shifting as CSL divests Wuhan assets, creating entry points for domestic plasma players. Broader insurance coverage in South Korea and rising private-sector hospitals in India combine with a growing middle class to swell patient volumes, driving upward momentum for the immunoglobulin market.

Europe exhibits steady, policy-anchored growth. Biotest's EUR 300 million expansion to 1.4 million L and Grifols' pan-European rollout of XEMBIFY exemplify commitment to both capacity and product innovation. Sustainability metrics, such as Grifols' 70-point CSA score, resonate with European Union green ambitions, encouraging cold-chain optimization and lower-carbon packaging. While Middle East and Africa remain smaller today, Gulf Cooperation Council investment in specialty care anchors future demand, and South America's nascent fractionation projects may shorten supply lines over the next decade.

- CSL Behring

- Grifols

- Takeda Pharmaceutical Co.

- Octapharma

- Kedrion Biopharma

- Baxter

- Bio Products Laboratory (BPL)

- LFB Group

- ADMA Biologics

- China Biologic Products

- Biotest

- Emergent Bio Solutions

- Sanquin

- Kamada Ltd.

- GC Biopharma

- Sichuan Yuanda Shuyang Pharma

- Kedrion Biopharma

- Pfizer

- AbbVie (Orchard Tx)

- Argenx SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of PID

- 4.2.2 Growing IVIG Use in Neurology (CIDP)

- 4.2.3 Expanded Plasma-fractionation Capacity

- 4.2.4 Emerging Recombinant/Plant-based Ig Platforms

- 4.2.5 Home-based High-concentration SCIg Push Infusions

- 4.2.6 AI-driven Plasma-supply Forecasting

- 4.3 Market Restraints

- 4.3.1 High Therapy Cost & Reimbursement Gaps

- 4.3.2 Stringent Donor-screening Regulations

- 4.3.3 Fc-engineered mAbs as Clinical Alternatives

- 4.3.4 Carbon-intensity Scrutiny of Cold-chain Logistics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value - USD)

- 5.1 By Product

- 5.1.1 IgG

- 5.1.2 IgA

- 5.1.3 IgM

- 5.1.4 IgE

- 5.1.5 IgD

- 5.2 By Mode of Delivery

- 5.2.1 Intravenous (IVIG)

- 5.2.2 Subcutaneous (SCIG)

- 5.2.3 Intramuscular

- 5.3 By Application

- 5.3.1 Hypogammaglobulinemia

- 5.3.2 Chronic Inflammatory Demyelinating Polyneuropathy (CIDP)

- 5.3.3 Primary Immunodeficiency Disease

- 5.3.4 Myasthenia Gravis

- 5.3.5 Immune Thrombocytopenia Purpura (ITP)

- 5.3.6 Other Applications

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products, and Recent Developments)

- 6.3.1 CSL Behring

- 6.3.2 Grifols S.A.

- 6.3.3 Takeda Pharmaceutical Co.

- 6.3.4 Octapharma AG

- 6.3.5 Kedrion Biopharma

- 6.3.6 Baxter International Inc.

- 6.3.7 Bio Products Laboratory (BPL)

- 6.3.8 LFB Group

- 6.3.9 ADMA Biologics

- 6.3.10 China Biologic Products

- 6.3.11 Biotest AG

- 6.3.12 Emergent BioSolutions

- 6.3.13 Sanquin

- 6.3.14 Kamada Ltd.

- 6.3.15 GC Pharma

- 6.3.16 Sichuan Yuanda Shuyang Pharma

- 6.3.17 Kedrion Biopharma

- 6.3.18 Pfizer Inc.

- 6.3.19 AbbVie (Orchard Tx)

- 6.3.20 Argenx SE

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment