PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939741

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939741

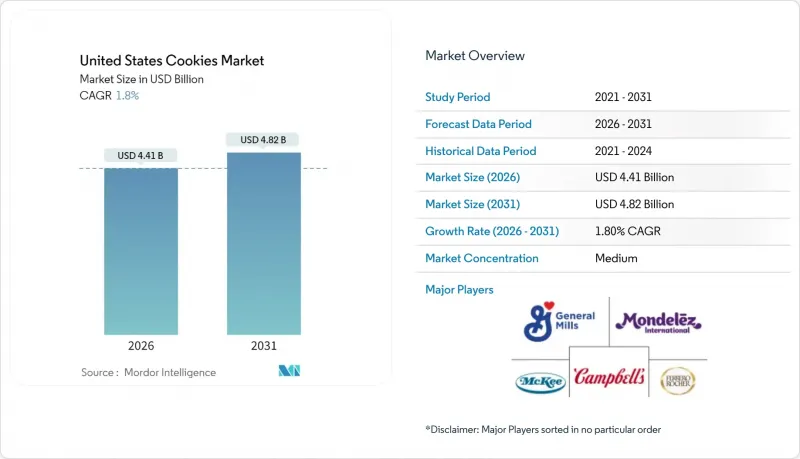

United States Cookies - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States cookies market is expected to grow from USD 4.33 billion in 2025 to USD 4.41 billion in 2026 and is forecast to reach USD 4.82 billion by 2031 at 1.8% CAGR over 2026-2031.

This measured growth trajectory reflects a maturing market where innovation and strategic positioning drive value creation rather than volume expansion. The sector's resilience stems from its ability to adapt to evolving consumer preferences while navigating regulatory complexities and supply chain pressures that have reshaped food manufacturing since 2024. Portion-controlled formats, nutrient fortification, and plant-based fat replacements attract wellness-minded consumers who still want indulgence, while gifting-oriented SKUs capitalize on seasonal demand in higher-income urban clusters. Regulatory shifts, especially the Food and Drug Administration's revised "healthy" definition and front-of-package (FOP) labeling, raise compliance costs but simultaneously create differentiation pathways for brands ready to reformulate. Consolidation continues to reshape competition as Mars integrates Kellanova and Ferrero prepares to fold WK Kellogg into its US snacking platform, heightening scale advantages in procurement, distribution, and shopper marketing. Retail channels evolve in parallel: hypermarkets remain critical for volume, yet direct-to-consumer subscriptions and e-grocery accelerate, giving premium newcomers low-barrier entry and rich consumer data pools.

United States Cookies Market Trends and Insights

Rising Demand for Portion-Controlled Indulgence Snacks

Consumer behavior analysis reveals a fundamental shift toward mindful consumption, where portion-controlled formats enable guilt-free indulgence without compromising health goals. This trend accelerates as urban professionals seek convenient snacking solutions that align with wellness objectives while satisfying taste preferences. The Northeast region leads this transformation, with higher disposable incomes supporting premium pricing for smaller, nutrient-dense formats. Food manufacturers respond by developing single-serve packaging and mini-cookie variants that deliver satisfying experiences within controlled caloric parameters. Campbell Soup Company's Pepperidge Farm launched limited-edition Holiday Cookie Jar Collections in 2025, featuring portion-controlled ceramic containers that reinforce mindful consumption while enhancing gift appeal. This strategic positioning captures growing consumer willingness to pay premiums for products that support lifestyle goals rather than merely satisfying hunger.

Accelerated Urban On-the-Go Breakfast Culture in Metropolitan Hubs

Metropolitan lifestyle changes drive demand for portable breakfast alternatives, with cookies increasingly substituting traditional morning meals among time-constrained consumers. This behavioral shift proves particularly pronounced in Northeast and West Coast urban centers, where commute patterns and work schedules prioritize convenience over conventional meal structures. The trend gains momentum as remote work arrangements create flexible eating schedules that blur traditional meal boundaries. Cookie manufacturers capitalize by developing breakfast-specific variants featuring whole grains, protein enhancement, and reduced sugar content that appeal to health-conscious morning consumers. Mondelez International's expansion of Oreo product lines in 2025 includes breakfast-positioned variants designed for morning consumption occasions. This strategic repositioning transforms cookies from afternoon snacks into legitimate breakfast options, expanding consumption occasions and driving incremental volume growth.

Fluctuating Raw Material Costs Impact Cookie Production Margins

Commodity price volatility creates significant margin pressure for cookie manufacturers, with wheat, sugar, and cocoa experiencing substantial fluctuations throughout 2024 and 2025. The World Bank forecasts wheat prices declining to USD 265 in 2025, providing some relief from previous highs, yet cocoa shortages drive prices up 30% in December 2024 due to a 14% global production decline . These input cost pressures force manufacturers to implement dynamic pricing strategies while managing consumer price sensitivity. Smaller manufacturers face disproportionate impact due to limited hedging capabilities and reduced negotiating power with suppliers. The pistachio shortage, driven by viral Dubai chocolate trends, exemplifies how social media can create unexpected supply chain disruptions, with prices increasing 35% from USD 7.65 to USD 10.30 per pound. Manufacturing efficiency improvements and ingredient substitution strategies become critical for maintaining profitability amid volatile input costs.

Other drivers and restraints analyzed in the detailed report include:

- Fortification and Nutrient Enhancement Drive Cookies Market Growth

- Plant-Based Fat Reformulation driving growth

- Increased HFSS Regulations Create Market Challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bar cookies command 31.62% market share in 2025, leveraging superior portability and extended shelf life that align with on-the-go consumption trends. Their rectangular format enables efficient packaging and portion control, making them ideal for single-serve applications and subscription box inclusion. Sandwich and Cream-Filled Cookies emerge as the fastest-growing segment at 1.88% CAGR through 2031, driven by flavor innovation and premium positioning strategies that command higher margins. Molded/Drop Cookies maintain steady performance through traditional appeal and manufacturing efficiency, while Wafer and Rolled Cookies benefit from texture differentiation and international flavor influences.

Mondelez International's strategic collaborations exemplify innovation within this segmentation, launching Oreo Reese's Cookies and Oreo Sour Patch Kids variants that blur category boundaries and expand consumption occasions. Butter/Shortbread and Plain varieties face pressure from health-conscious trends yet retain loyal consumer bases in traditional markets. The "Others" category encompasses emerging formats like protein-enhanced cookies and gluten-free alternatives that capture niche but growing market segments. Manufacturing automation enables cost-effective production of diverse formats, with AI-powered quality control systems reducing defect rates and improving consistency across product types.

The conventional segment maintains overwhelming dominance at 89.65% market share in 2025, reflecting established consumer preferences and price sensitivity that favor traditional formulations. However, the Free-From/Organic category's 2.93% CAGR through 2031 signals accelerating consumer migration toward clean-label alternatives, driven by health consciousness and environmental concerns. This growth trajectory suggests conventional products may face increasing pressure as organic alternatives achieve price parity through scale economies and supply chain optimization.

USDA organic certification requirements create compliance complexity but enable premium pricing that attracts manufacturers seeking margin expansion . Organic cookie production faces challenges in sourcing certified ingredients at scale, particularly for specialty items like organic chocolate chips and natural flavoring compounds. Free-from variants targeting gluten-free, dairy-free, and allergen-free segments capture growing consumer segments with specific dietary requirements. Flowers Foods' USD 795 million acquisition of Simple Mills in 2025 demonstrates a strategic commitment to the better-for-you category, leveraging Simple Mills' expertise in premium crackers, cookies, and baking mixes.

The US Cookies Market is Segmented by Product Type (Bar Cookies, Molded/Drop Cookies, Sandwich and Cream-Filled Cookies, Wafer and Rolled Cookies, Butter/Shortbread and Plain, Other Types), Category (Conventional and Free-From/Organic), Packaging Types (Pouches, Boxes, Others), and Distribution Channel (Hypermarkets/Supermarkets, Convenience Stores, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- General Mills Inc.

- Mondelez International

- Ferrero Group

- Mckee Foods Corporation

- The Campbell Soup Company

- PepsiCo Inc.

- Kellogg Co. (Kellanova)

- Grupo Bimbo S.A.B. de C.V.

- Hostess Brands, LLC

- Girl Scouts of the USA

- B&G Foods, Inc.

- Flowers Foods, Inc.

- Otis Spunkmeyer (ARYZTA)

- Partake Foods

- Tate's Bake Shop

- Voortman Cookies Limited

- Lofthouse Cookies (TreeHouse Foods)

- Nonni's Foods LLC

- Thinsters (J&J Snack Foods)

- Mrs. Fields Original Cookies, Inc.

- Vencomatic Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Portion-Controlled Indulgence Snacks

- 4.2.2 Accelerated Urban On-the-Go Breakfast Culture in Metropolitan Hubs

- 4.2.3 Fortification and Nutrient Enhancement Drive Cookies Market Growth

- 4.2.4 Plant-Based Fat Reformulation driving growth

- 4.2.5 Direct-to-Consumer Subscription Surge for Gourmet Cookies

- 4.2.6 Gifting and Premiumization as Emotional Positioning

- 4.3 Market Restraints

- 4.3.1 Fluctuating Raw Material Costs Impact Cookie Production Margins

- 4.3.2 Increased HFSS Regulations Create Market Challenges

- 4.3.3 Food Safety Compliance Requirements

- 4.3.4 Growing Market Share of Alternative Snacking Options

- 4.4 Supply Chain Analysis

- 4.5 Regualtory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Bar Cookies

- 5.1.2 Molded/Drop Cookies

- 5.1.3 Sandwich and Cream-Filled Cookies

- 5.1.4 Wafer and Rolled Cookies

- 5.1.5 Butter/Shortbread and Plain

- 5.1.6 Others

- 5.2 By Category

- 5.2.1 Conventional

- 5.2.2 Free-From/Organic

- 5.3 By Packaging Type

- 5.3.1 Pouches

- 5.3.2 Boxes

- 5.3.3 Others

- 5.4 By Distribution Channel

- 5.4.1 Hypermarkets/Supermarkets

- 5.4.2 Convenience Stores

- 5.4.3 Specialist Retailers

- 5.4.4 Online Retailers

- 5.4.5 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 Northeast

- 5.5.2 Midwest

- 5.5.3 South

- 5.5.4 West

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 General Mills Inc.

- 6.4.2 Mondelez International

- 6.4.3 Ferrero Group

- 6.4.4 Mckee Foods Corporation

- 6.4.5 The Campbell Soup Company

- 6.4.6 PepsiCo Inc.

- 6.4.7 Kellogg Co. (Kellanova)

- 6.4.8 Grupo Bimbo S.A.B. de C.V.

- 6.4.9 Hostess Brands, LLC

- 6.4.10 Girl Scouts of the USA

- 6.4.11 B&G Foods, Inc.

- 6.4.12 Flowers Foods, Inc.

- 6.4.13 Otis Spunkmeyer (ARYZTA)

- 6.4.14 Partake Foods

- 6.4.15 Tate's Bake Shop

- 6.4.16 Voortman Cookies Limited

- 6.4.17 Lofthouse Cookies (TreeHouse Foods)

- 6.4.18 Nonni's Foods LLC

- 6.4.19 Thinsters (J&J Snack Foods)

- 6.4.20 Mrs. Fields Original Cookies, Inc.

- 6.4.21 Vencomatic Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK