PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852141

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852141

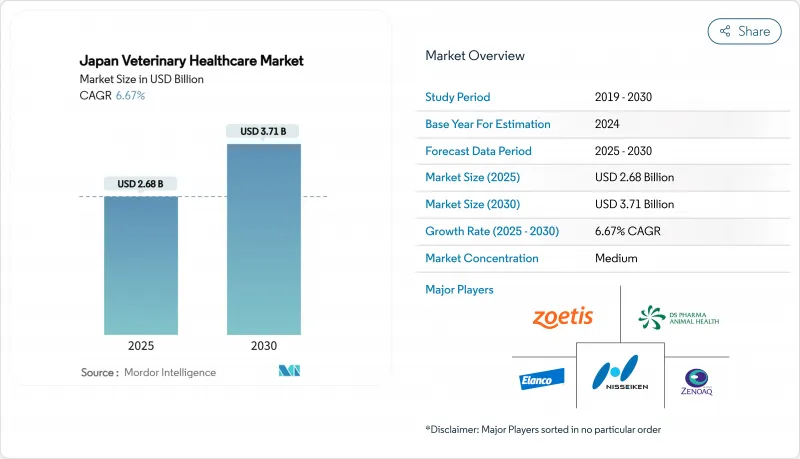

Japan Veterinary Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Japan veterinary healthcare market size stood at USD 2.68 billion in 2025 and is projected to reach USD 3.71 billion by 2030, advancing at a 6.67% CAGR.

This expansion reflects the country's rapid shift from a livestock-centric model to a companion-animal focus, with pets now outnumbering children under fifteen. Growth catalysts include the steady rollout of digital diagnostics, wider pet-insurance adoption, and supportive government biosecurity budgets. The Japan veterinary healthcare market also benefits from rising demand for premium therapeutics such as monoclonal antibodies and cannabidiol supplements, together with new workflow software that shortens diagnosis-to-treatment cycles. At the same time, declining domestic meat consumption curbs farm-animal revenue, prompting companies to diversify toward high-margin companion-animal services while leveraging the same distribution channels for both segments.

Japan Veterinary Healthcare Market Trends and Insights

Rising Companion Animal Expenditure

Lifetime ownership costs climbed to JPY 2.446 million (USD 16,300) for dogs and JPY 1.499 million (USD 10,000) for cats in 2025, underscoring household readiness to fund complex oncology, cardiology, and orthopedic care. Heightened spending links to strong pet-insurance coverage, with Anicom Insurance supporting more than 7,000 partner clinics nationwide. Owners of pets under one year accept treatment bills of USD 800-1,200 per ingestion incident, reaffirming healthcare as a core component of pet well-being.

Government Vaccination Campaigns for Livestock Biosecurity

The Ministry of Agriculture, Forestry and Fisheries maintains a 6.2 million-dose avian-influenza reserve and mandates 24-hour reporting of suspect cases, a legacy of the 2010 foot-and-mouth crisis in which 289,000 animals were culled. Regular surveillance and movement controls ensure reliable demand for vaccines and rapid tests across 4.56 million cattle, 9.61 million pigs, and 294 million chickens.

Escalating Veterinary Service Costs

Clinic fees have risen 60% faster than consumer inflation since 2005, driven by workforce shortages and imported-drug price hikes. Nearly 48.4% of owners name cost as the main deterrent to vet visits, with 13.7% foregoing annual check-ups entirely. Rural closures amplify access gaps, prompting clinics to adopt installment payments and teleconsults to sustain care quality while moderating price growth.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements in Veterinary Diagnostics

- Expansion of Pet-Insurance Analytics Ecosystems

- Counterfeit Pharmaceutical Distribution

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Therapeutics accounted for 61.43% of the Japan veterinary healthcare market share in 2024, anchored by vaccine mandates and the popularity of parasiticides. Monoclonal antibody products for osteoarthritis and parenteral analgesics register double-digit clinic uptake, reflecting owner readiness to pay for human-grade care. Companion-animal vaccines post high adherence, while livestock biologics rely on government procurement that smooths annual demand.

Diagnostics, the fastest-growing category at a 7.12% CAGR, benefits from in-house PCR, immunoassay, and digital imaging platforms that deliver immediate results and raise practice revenue. As value-based preventive care gains traction, diagnostic vendors emphasize return-on-investment metrics such as reduced follow-up visits and higher client satisfaction. Market consolidation emerges as distributors bundle equipment leasing, reagent supply, and cloud analytics, shortening time to profit for clinics.

Dogs and cats captured 43.67% of the Japan veterinary healthcare market size in 2024. Specialized oncology, orthopedic, and cardiology procedures expand, and subscription wellness packages that bundle check-ups with nutritional advice secure recurring income at clinics. Insurers reimburse advanced imaging such as CT and MRI, which lifts adoption rates in urban hospitals.

Poultry is forecast to grow at a 6.53% CAGR, propelled by mandatory vaccination and PCR monitoring in intensive layer and broiler farms across Kyushu. Larger producers integrate sensor-enabled barns and employ analytics to predict disease outbreaks, sustaining demand for biologics and realtime diagnostic kits. Swine and cattle segments see mild expansion as domestic meat consumption stabilizes; however premium Wagyu breeders still invest heavily in reproductive and genomic services.

The Japan Veterinary Healthcare Market Report is Segmented by Product (Therapeutics and Diagnostics), Animal Type (Dogs & Cats, Horses, and More), Route of Administration (Oral, Parenteral, and More), End User (Veterinary Hospitals & Clinics, Reference Laboratories, Point-Of-Care/In-House Testing Settings, Academic & Research Institutes). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Elanco

- Boehringer Ingelheim

- Kyoritsu Seiyaku Corporation

- FUJIFILM

- Merck & Co., Inc. (MSD Animal Health)

- Nihon Nohyaku Co., Ltd.

- Nippon Zenyaku Kogyo Co., Ltd.

- Nisseiken

- Sumitomo Pharma Co., Ltd.

- Virbac

- Zoetis

- IDEXX

- Ceva Sante Animale SA

- Anicom

- Vetoquinol

- Canon

- Sumika Enviro-Science Co., Ltd.

- Chugai Pharmaceutical

- Nihon Pet Food Co., Ltd.

- Kyodo Milk Industry Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Companion Animal Expenditure

- 4.2.2 Government Vaccination Campaigns for Livestock Biosecurity

- 4.2.3 Technological Advancements in Veterinary Diagnostics

- 4.2.4 Expansion of Pet Insurance Data Analytics Ecosystems

- 4.2.5 Emerging Demand For Alternative Therapies such as CBD Nutraceuticals

- 4.3 Market Restraints

- 4.3.1 Escalating Veterinary Service Costs

- 4.3.2 Counterfeit Pharmaceutical Distribution

- 4.3.3 Shrinking Domestic Livestock Population Due to Dietary Shifts

- 4.3.4 Regulatory Approval Delays for Novel Therapeutics

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Buyers/Consumers

- 4.5.3 Bargaining Power Of Suppliers

- 4.5.4 Threat Of Substitute Products

- 4.5.5 Intensity Of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Therapeutics

- 5.1.1.1 Vaccines

- 5.1.1.2 Parasiticides

- 5.1.1.3 Anti-Infectives

- 5.1.1.4 Medical Feed Additives

- 5.1.1.5 Other Therapeutics

- 5.1.2 Diagnostics

- 5.1.2.1 Immunodiagnostic Tests

- 5.1.2.2 Molecular Diagnostics

- 5.1.2.3 Diagnostic Imaging

- 5.1.2.4 Clinical Chemistry

- 5.1.2.5 Other Diagnostics

- 5.1.1 Therapeutics

- 5.2 By Animal Type

- 5.2.1 Dogs & Cats

- 5.2.2 Horses

- 5.2.3 Ruminants

- 5.2.4 Swine

- 5.2.5 Poultry

- 5.2.6 Other Animal Types

- 5.3 By Route Of Administration

- 5.3.1 Oral

- 5.3.2 Parenteral

- 5.3.3 Topical

- 5.3.4 Other Route of Administrations

- 5.4 By End User

- 5.4.1 Veterinary Hospitals & Clinics

- 5.4.2 Reference Laboratories

- 5.4.3 Point-Of-Care / In-House Testing Settings

- 5.4.4 Academic & Research Institutes

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Elanco Animal Health Incorporated

- 6.3.2 Boehringer Ingelheim GmbH

- 6.3.3 Kyoritsu Seiyaku Corporation

- 6.3.4 FUJIFILM Holdings Corporation

- 6.3.5 Merck & Co., Inc. (MSD Animal Health)

- 6.3.6 Nihon Nohyaku Co., Ltd.

- 6.3.7 Nippon Zenyaku Kogyo Co., Ltd.

- 6.3.8 Nisseiken Co., Ltd.

- 6.3.9 Sumitomo Pharma Co., Ltd.

- 6.3.10 Virbac SA

- 6.3.11 Zoetis Inc.

- 6.3.12 IDEXX Laboratories Inc.

- 6.3.13 Ceva Sante Animale SA

- 6.3.14 Anicom Holdings Inc.

- 6.3.15 Vetoquinol SA

- 6.3.16 Canon Medical Systems Corp.

- 6.3.17 Sumika Enviro-Science Co., Ltd.

- 6.3.18 Chugai Pharmaceutical Co., Ltd.

- 6.3.19 Nihon Pet Food Co., Ltd.

- 6.3.20 Kyodo Milk Industry Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment