PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852154

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852154

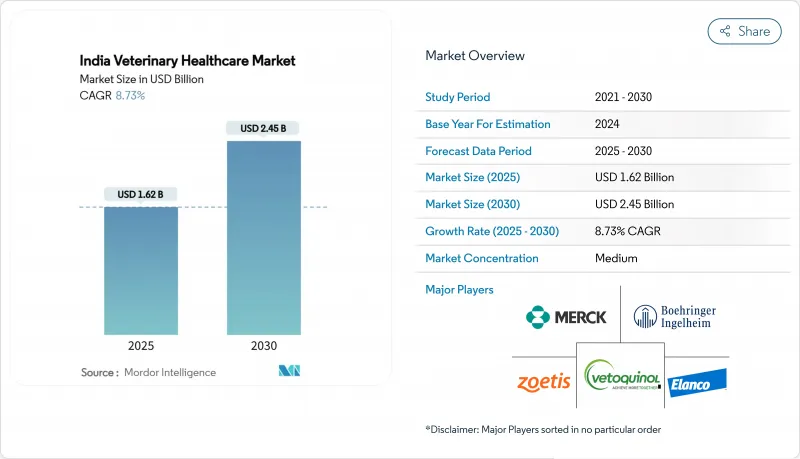

India Veterinary Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The India veterinary healthcare market size is USD 1.62 billion in 2025 and is projected to reach USD 2.45 billion in 2030, reflecting an 8.73% CAGR during the forecast period.

Growth is propelled by rising pet humanization, government-funded immunization programs, and AI-enabled diagnostic solutions that improve access to quality care in both urban and rural regions. India's status as the largest global livestock holder gives therapeutics scale, while a surge in companion animal ownership boosts premium services. Indigenous vaccine development, notably for lumpy skin disease, is strengthening supply security and lowering import reliance. Technology investments by multinationals in local AI centers are unlocking rapid point-of-care testing and telehealth models that narrow the urban-rural treatment gap.

India Veterinary Healthcare Market Trends and Insights

Growing Animal Population and Ownership

Pet dog numbers jumped from 12.6 million in 2014 to 33.6 million in 2023 and are projected to hit 51.5 million by 2028, driving sustained demand for wellness, diagnostics, and elective procedures. Urban households already show 25% pet penetration and are on track to reach 35% by 2025, shifting care expectations from basic vaccinations to multi-specialty services. Annual pet healthcare spending averages INR 70,000-80,000, with surgical episodes costing INR 20,000-30,000, underpinning premiumization across products and services. Parallel livestock expansion keeps demand broad-based as India's cattle herd touches 307.42 million, requiring mass immunization and nutritional support. This dual growth across companion and production animals sustains the India veterinary healthcare market by diversifying revenue streams.

Government-Led Immunization and Disease-Control Programs

The National Livestock Mission offers 50% capital subsidies up to INR 50 lakh for breeding farms, feed units, and clinics, directly stimulating purchases of vaccines and therapeutics. June 2024 saw the rollout of the indigenously produced lumpy skin disease vaccine that safeguards the country's 300 million-plus bovines. The National One Health Mission aligns human and animal disease surveillance, accelerating uptake of diagnostics that detect zoonoses early. April 2025 approvals of H9N2 poultry vaccines and stricter farm biosecurity rules reinforce the preventive health paradigm. Given India's status as the third-largest egg producer, these programs mitigate economic shocks from outbreaks and keep the India veterinary healthcare market growth trajectory intact.

Prevalence of Counterfeit or Substandard Veterinary Products

Dual oversight by central and state regulators creates enforcement blind spots that illicit manufacturers exploit by shifting production across jurisdictions. From January 2025, all drug approvals must be filed online with the CDSCO, a move expected to tighten traceability. Still, price-sensitive buyers in rural markets often favor cheaper products without verified quality, which can compromise treatment outcomes and erode trust in veterinary interventions. Smaller firms face high compliance costs under revised Schedule M GMP norms implemented in December 2023, increasing the risk of non-compliance among resource-constrained players. Substandard therapeutics hamper disease control, slow vaccination drives, and ultimately weigh on the India veterinary healthcare market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements in Veterinary Diagnostics and Telehealth

- Rising Adoption of Pet Insurance and Health Financing

- High Cost of Advanced Veterinary Treatments and Diagnostics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Therapeutics accounted for a 57.54% share of the India veterinary healthcare market in 2024 and remain foundational due to the country's 300 million-head cattle herd. Vaccine demand is buoyed by the domestic lumpy skin disease shot launched in 2024, while parasiticides gain traction from products like NexGard Spectra approved in April 2024. Vaccines dominate sub-category revenues, reflecting India's role as a 60% supplier of global doses, and policies such as the National Livestock Mission accelerate uptake. Parasiticides and anti-infectives keep production animals efficient and companion animals parasite-free. Medical feed additives help producers maintain productivity while managing antimicrobial resistance mandates.

Diagnostics is the fastest-growing product group at a 9.56% CAGR through 2030. The segment rides on point-of-care systems that allow rapid barn-side decision-making, critical in geographies lacking specialist labs. Immunodiagnostics remain the largest sub-segment, tapped by One Health surveillance programs. Molecular tests pair with AI image readers to deliver 86.54% accuracy in bovine lesion detection, minimizing economic losses. Clinical chemistry and imaging thrive as corporate vet chains upscale practices. IDEXX logged 700 orders for its inVue analyzer in Q3 2024, underscoring rising in-clinic diagnostics adoption. This tech momentum is positioning diagnostics to capture a rising proportion of the India veterinary healthcare market size over the forecast horizon.

Dogs & cats generated 45.32% of the India veterinary healthcare market in 2024, underpinned by high per-pet spending and growing insurance penetration. Average annual outlays of INR 70,000-80,000 include elective treatments, preventive care, and specialized nutrition, boosting provider margins. Mars Inc.'s 2024 investment in Crown Veterinary Services reflects the anticipated surge in urban pet healthcare demand. Equine care remains niche but gains visibility through welfare programs at fairs. Ruminants continue to underpin vaccine volume, driven by herd-level immunization initiatives.

Poultry is projected to be the fastest-growing animal segment at an 8.99% CAGR, reflecting India's third-place rank in global egg production. Virbac's 2024 purchase of Globion for its poultry vaccine line signals confidence in this category. Capacity is scaling to 267,800 birds per hour by 2026, increasing disease-prevention spending. Government-endorsed H9N2 vaccines plus farm registration mandates encourage broader adoption of preventive health programs. AI-enhanced flock monitoring tools improve feed conversion and disease prediction, propelling poultry's share of the India veterinary healthcare market upward.

The India Veterinary Healthcare Market Report is Segmented by Product (Therapeutics and Diagnostics), Animal Type (Dogs & Cats, Horses, Ruminants, and More), Route of Administration (Oral, Parenteral, and More), End User (Veterinary Hospitals & Clinics, Reference Laboratories, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Zoetis

- Boehringer Ingelheim

- Merck

- Elanco

- Virbac

- Vetoquinol

- IDEXX

- Indian Immunologicals

- Hester Biosciences Ltd.

- Zydus Animal Health

- Ceva Sante Animale

- Intas Pharma (Sequent Scientific)

- Phibro Animal Health

- Bayer Animal Health

- Neogen Corp.

- Cipla Vet

- Mankind Pharma (PetStar)

- Himalaya Animal Health

- Ayurvet Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Animal Population and Ownership

- 4.2.2 Government-Led Immunization and Disease-Control Programs

- 4.2.3 Technological Advancements in Veterinary Diagnostics and Telehealth

- 4.2.4 Rising Adoption of Pet Insurance and Health Financing

- 4.2.5 Expansion of Organized Veterinary Retail and E-Commerce Channels

- 4.2.6 Intensifying Focus on Livestock Productivity and Food Safety

- 4.3 Market Restraints

- 4.3.1 Prevalence of Counterfeit or Substandard Veterinary Products

- 4.3.2 High Cost of Advanced Veterinary Treatments and Diagnostics

- 4.3.3 Shortage of Skilled Veterinary Professionals and Support Staff

- 4.3.4 Inadequate Cold Chain and Rural Distribution Infrastructure

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Therapeutics

- 5.1.1.1 Vaccines

- 5.1.1.2 Parasiticides

- 5.1.1.3 Anti-Infectives

- 5.1.1.4 Medical Feed Additives

- 5.1.1.5 Other Therapeutics

- 5.1.2 Diagnostics

- 5.1.2.1 Immunodiagnostic Tests

- 5.1.2.2 Molecular Diagnostics

- 5.1.2.3 Diagnostic Imaging

- 5.1.2.4 Clinical Chemistry

- 5.1.2.5 Other Diagnostics

- 5.1.1 Therapeutics

- 5.2 By Animal Type

- 5.2.1 Dogs & Cats

- 5.2.2 Horses

- 5.2.3 Ruminants

- 5.2.4 Swine

- 5.2.5 Poultry

- 5.2.6 Other Animal Types

- 5.3 By Route Of Administration

- 5.3.1 Oral

- 5.3.2 Parenteral

- 5.3.3 Topical

- 5.3.4 Other Route of Administrations

- 5.4 By End User

- 5.4.1 Veterinary Hospitals & Clinics

- 5.4.2 Reference Laboratories

- 5.4.3 Point-Of-Care / In-House Testing Settings

- 5.4.4 Academic & Research Institutes

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Zoetis Inc.

- 6.3.2 Boehringer Ingelheim GmbH

- 6.3.3 Merck Animal Health

- 6.3.4 Elanco Animal Health

- 6.3.5 Virbac

- 6.3.6 Vetoquinol

- 6.3.7 IDEXX Laboratories Inc.

- 6.3.8 Indian Immunologicals Ltd.

- 6.3.9 Hester Biosciences Ltd.

- 6.3.10 Zydus Animal Health

- 6.3.11 Ceva Sante Animale

- 6.3.12 Intas Pharma (Sequent Scientific)

- 6.3.13 Phibro Animal Health

- 6.3.14 Bayer Animal Health

- 6.3.15 Neogen Corp.

- 6.3.16 Cipla Vet

- 6.3.17 Mankind Pharma (PetStar)

- 6.3.18 Himalaya Animal Health

- 6.3.19 Ayurvet Limited

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment