PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852159

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852159

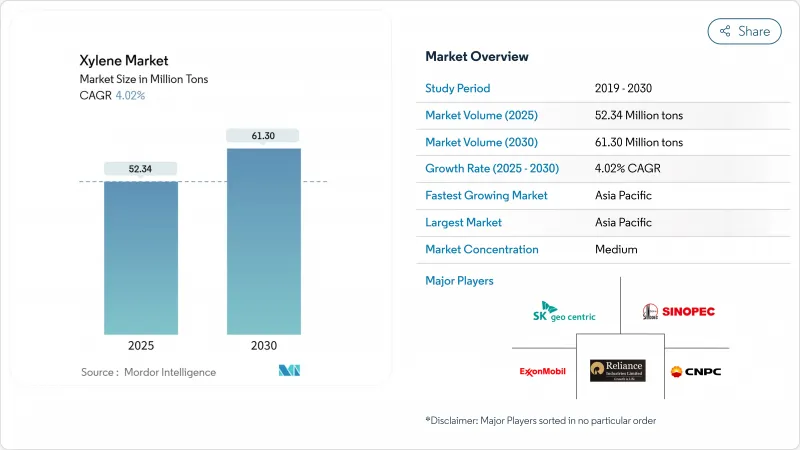

Xylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The xylene market size stands at 52.34 million tons in 2025 and is forecast to touch 61.3 million tons by 2030, advancing at a 4.02% CAGR.

Growth rests on para-xylene's dominant role in polyester production, large-scale integrated aromatics projects across Asia and the Middle East, and rising demand for engineering plastics in North America. Rapid equipment investments in Chinese and Indian complexes are lifting regional self-sufficiency, while bio-based chemistries gain early-stage momentum as regulatory and brand-owner pressures intensify. Margin outlook hinges on naphtha price volatility, yet backward-integrated producers capture value across refining, aromatics, and derivative chains. Competitive advantage is tilting toward firms that combine feedstock flexibility, digital optimization, and credible decarbonization roadmaps.

Global Xylene Market Trends and Insights

Surging PET Resin Demand Fueling Para-xylene Consumption in Asia

Massive polyester build-outs are realigning feedstock flows. China plans to massive para-xylene capacity between 2024-2028. The escalation secures PTA supply for rapidly growing PET film and bottle output. Producers are vertically integrating to manage cost and logistics exposure, while increasing naphtha imports backfill Asian shortfalls.

Capacity Expansions in Integrated Aromatics Complexes across Middle East and Asia

Projects such as Saudi Aramco's Amiral Complex couple refining with downstream aromatics to unlock feedstock savings and high para-xylene yields. Shared utilities, advanced catalysts, and real-time optimization cut unit costs and strengthen regional export competitiveness. These mega-sites are shifting supply balances and forcing older standalone plants to rationalize or upgrade.

Stringent VOC Norms Limiting Aromatic Solvent Use in Europe and North America

Regulators are extending VOC limits to consumer paints, cleaners, and indoor products. Compliance forces reformulators to cut xylene loadings or redesign entire chemistries, constraining growth in mature economies. Producers pivot toward low-aromatic or bio-based blends to retain market access.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Lightweighting Driving Engineering Plastics in North America

- Growing Usage of Xylene as Solvents and Monomers

- Health-toxicity Concerns Prompting Shift to Oxygenated Solvents

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Para-xylene held 90% of xylene market share in 2024, anchored by its indispensable role in PTA and PET chains. Robust downstream integration lets leading refiners hedge margin swings and assure captive demand. Ortho-xylene, though much smaller, leads growth at 4.09% CAGR on the back of flexible plasticizer demand in phthalic anhydride. Meta-xylene addresses niche coatings and specialty resins, while mixed xylene offers supply optionality for isomer separation. Catalyst advances and isomerization units let operators fine-tune output to price signals, enhancing profitability within an otherwise commoditized slate. This adaptive capability sustains para-xylene's centrality even as derivative trade flows reorganize.

Producers continue debottlenecking para-xylene extraction units in Asia to exploit economies of scale and meet swelling PET bottle orders. North American suppliers emphasize value-added grades for film applications that demand low acetaldehyde formation. European refiners increasingly channel mixed streams toward hydrogenated solvents to comply with tightening emission rules, a trend set to carve out specialized demand niches for each isomer through 2030.

Technical grade captured 85% of the xylene market in 2024 as coatings formulators, adhesive blenders, and industrial cleaners prioritize cost, availability, and mid-range solvency. Its straightforward production route from reformate and BTX pools yields abundant supply and competitive pricing. Bulk consumers in emerging economies absorb this volume for infrastructure and manufacturing surge phases, reinforcing its central role.

Conversely, high-purity 99.9% material is growing at 4.7% CAGR on semiconductor, pharmaceutical, and high-performance resin applications. Meeting its exacting specifications demands advanced crystallization, distillation, and on-stream analytics, creating high entry barriers and attractive margins. Producers with integrated lab services and robust quality systems capitalize on this specialized lane, carving higher EBITDA per ton against commodity counterparts.

The Xylene Market Report Segments the Industry by Type (Ortho-Xylene, Meta-Xylene, and More), Grade (Technical Grade and High-Purity Grade (99. 9%)), Source (Petroleum-Based Xylene and Bio-Based Xylene), Application (Solvent, Monomer, and Other Applications), End-User Industry (Plastics and Polymers, Paints and Coatings, Adhesives, and Other End-User Industries), and Geography (Asia-Pacific, North America, and More).

Geography Analysis

Asia-Pacific controlled 55% of the xylene market in 2024 and is growing 4.51% yearly to 2030. Chinese para-xylene capacity expansions of 25 million tons/year through 2028 underpin regional self-sufficiency, while Indian PET lines supply booming beverage demand. Major ASEAN economies import mixed xylenes to backfill shortfalls, sustaining intra-Asian trade flows. Intensifying competition is compressing spreads, spurring alliances and downstream PTA linkages.

North America shows stable albeit lower growth. Shale-based feedstock economics give refiners advantaged BTX yields. Automotive lightweighting regulations elevate engineering plastic use, fortifying derivative demand despite stringent VOC curbs in paints. Regulatory clarity combined with established logistics encourage incremental debottlenecks rather than greenfield builds.

Europe's mature demand landscape is reshaping under sustainability mandates. Germany's chemical clusters refine high-efficiency processes, the United Kingdom and France deploy circular solvent recovery units, and EU-wide REACH classifications prompt reformulation into lower-aromatic blends. Bio-based pilots supported by policy incentives aim to cement early footholds in renewable aromatics, with niche grades targeting premium coating and electronics markets.

- Braskem

- Chevron Phillips Chemical Company LLC

- China Petrochemical Corporation

- CNPC

- ENEOS Corporation

- Exxon Mobil Corporation

- Formosa Chemicals & Fibre Corp

- FUJAN REFINING & PETROCHEMICAL COMPANY LIMITED

- GS Caltex Corporation

- Indian Oil Corporation Ltd

- INEOS AG

- LOTTE Chemical Corporation

- Mangalore Refinery and Petrochemicals limited

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- Mitsui Chemicals, Inc.

- Petro Rabigh

- PTT Global Chemical Public Company Limited

- QatarEnergy

- Reliance Industries Limited

- SK Geocentric Co., Ltd.

- S-OIL CORPORATION

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging PET Resin Demand Fueling Para-xylene Consumption in Asia

- 4.2.2 Capacity Expansions in Integrated Aromatics Complexes across Middle east and Asia

- 4.2.3 Automotive Lightweighting Driving Engineering Plastics in North America

- 4.2.4 Growing Usage of Xylene as Solvents and Monomers

- 4.2.5 Strategic Stockpiling of Solvents by Pharma amid Supply-chain Volatility

- 4.3 Market Restraints

- 4.3.1 Stringent VOC Norms Limiting Aromatic Solvent Use in Europe and North America

- 4.3.2 Health-toxicity Concerns Prompting Shift to Oxygenated Solvents

- 4.3.3 Volatile Naphtha Prices Compressing Producer Margins

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Ortho-xylene

- 5.1.2 Meta-xylene

- 5.1.3 Para-xylene

- 5.1.4 Mixed xylene

- 5.2 By Grade

- 5.2.1 Technical Grade

- 5.2.2 High-Purity Grade (99.9 %)

- 5.3 By Source

- 5.3.1 Petroleum-based Xylene

- 5.3.2 Bio-based Xylene

- 5.4 By Application

- 5.4.1 Solvents

- 5.4.2 Monomer

- 5.4.3 Other Applications

- 5.5 By End-user Industry

- 5.5.1 Plastics and Polymers

- 5.5.2 Paints and Coatings

- 5.5.3 Adhesives

- 5.5.4 Other End-user Industries

- 5.6 Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 India

- 5.6.1.3 Japan

- 5.6.1.4 South Korea

- 5.6.1.5 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle East and Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Braskem

- 6.4.2 Chevron Phillips Chemical Company LLC

- 6.4.3 China Petrochemical Corporation

- 6.4.4 CNPC

- 6.4.5 ENEOS Corporation

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 Formosa Chemicals & Fibre Corp

- 6.4.8 FUJAN REFINING & PETROCHEMICAL COMPANY LIMITED

- 6.4.9 GS Caltex Corporation

- 6.4.10 Indian Oil Corporation Ltd

- 6.4.11 INEOS AG

- 6.4.12 LOTTE Chemical Corporation

- 6.4.13 Mangalore Refinery and Petrochemicals limited

- 6.4.14 MITSUBISHI GAS CHEMICAL COMPANY, INC.

- 6.4.15 Mitsui Chemicals, Inc.

- 6.4.16 Petro Rabigh

- 6.4.17 PTT Global Chemical Public Company Limited

- 6.4.18 QatarEnergy

- 6.4.19 Reliance Industries Limited

- 6.4.20 SK Geocentric Co., Ltd.

- 6.4.21 S-OIL CORPORATION

- 6.4.22 TotalEnergies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Bio-based Xylene Commercialization