PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852200

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852200

CRISPR Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

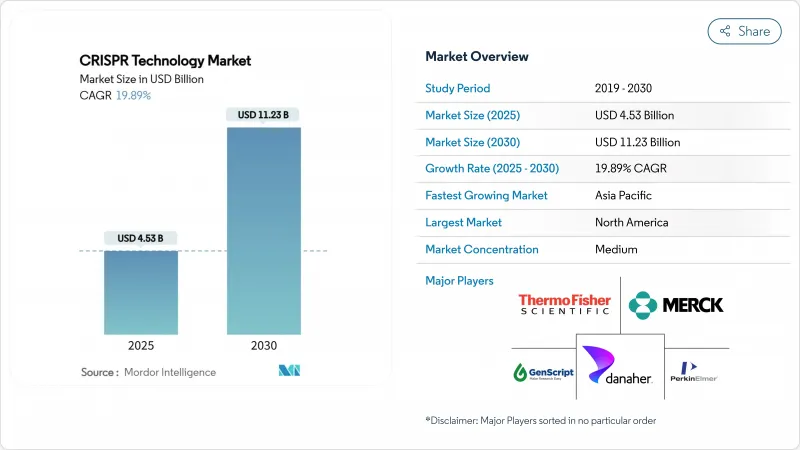

The CRISPR technology market size stood at USD 4.53 billion in 2025 and is projected to reach USD 11.23 billion by 2030, reflecting a 19.89% CAGR.

Rapid growth follows the December 2023 FDA clearance of CASGEVY, the first CRISPR therapy for B-thalassemia and sickle-cell disease. Capital inflows continue as prime-editing trials report positive human data and falling reagent costs widen the user base. Consolidation around delivery know-how is visible through investments such as Regeneron's stake in Mammoth Biosciences, while public bioeconomy initiatives in the United States, United Kingdom, China, and Australia support downstream manufacturing. The CRISPR technology market benefits from clearer regulatory guidance and a growing pipeline that now spans hematology, oncology, neurological, and agricultural use cases.

Global CRISPR Technology Market Trends and Insights

Expanding Clinical Pipeline for Genetic Disorders

More than 40 CRISPR-based medicines are in active trials worldwide. CASGEVY generated USD 200 million in first-year sales, validating premium pricing models for severe blood disorders. Prime-editing achieved functional immune restoration in chronic granulomatous disease without serious safety issues during its 2025 first-in-human study. The FDA's January 2024 guidance clarified biodistribution and off-target study expectations, shortening regulatory uncertainty. Early lung-cell work corrected 60% of cystic-fibrosis mutations, expanding respiratory prospects. Several programs targeting oncology and ophthalmology now enroll patients, backed by alliances that pair editing expertise with capital-rich pharma partners.

Strategic Pharma-Biotech Alliances for In-Vivo CRISPR Therapies

Regeneron's USD 95 million upfront payment to Mammoth Biosciences exemplifies capital-sharing to solve delivery bottlenecks. Sanofi's collaboration with Scribe Therapeutics carries USD 1.2 billion in milestones for compact Cas enzymes suited to neurological targets. CRISPR Therapeutics and Capsida joined forces to deploy AAV vectors against ALS. Danaher funds the Innovative Genomics Institute's Beacon for CRISPR Cures to industrialize manufacturing pipelines. These alliances combine delivery, regulatory, and GMP capabilities, accelerating clinical timelines across the CRISPR technology market.

Stringent Regulatory Scrutiny and Evolving Compliance Frameworks

The FDA now requires genome-wide off-target profiling plus long-term monitoring for human trials, extending timelines and budgets. The EMA mandates parallel but non-identical datasets, forcing developers to craft region-specific filings. US environmental tools must satisfy EPA, USDA, and FDA, complicating field-trial approvals for engineered microbes. Large companies build in-house compliance teams, whereas start-ups outsource to specialist CROs, raising operating costs across the CRISPR technology market. Until inter-agency harmonization progresses, smaller firms face higher capital hurdles to reach clinical or commercial scale.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Functional-Genomics Discovery Acceleration

- Government Bioeconomy Programs Supporting Synthetic-Biology Scale-Up

- Unresolved Ethical Concerns Around Germline Editing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Kits & Reagents accounted for 43.23% revenue in 2024, reflecting essential consumables like guide RNAs, nucleases, and delivery mixes used in every experiment. The segment delivers recurring sales that smooth research-funding cycles. Design Tools/Software is the fastest-growing category with a 21.34% CAGR, propelled by AI-assisted platforms that simplify experimental planning. Enzymes maintain steady demand as improved fidelity variants launch yearly, while custom guide-RNA catalogs expand to meet precision-therapy needs. CRISPR libraries support pooled screens in drug discovery, and other specialized delivery reagents address tissue-specific challenges.

Historical growth from 2019-2024 emphasized consumable expansion, while the 2025-2030 horizon focuses on integrated platforms bundling cloud design, lab automation, and reagent fulfillment. Vendors differentiate on workflow performance rather than standalone product specs. The CRISPR technology market size for kits & reagents is projected to surpass USD 5.4 billion by 2030, equal to roughly 48% of total revenue. Bundled subscriptions lock customers into single-vendor ecosystems, sustaining margins despite commodity pressure.

The Kits & Reagents segment is projected to exhibit the highest growth rate of approximately 21% during the forecast period 2024-2029. This accelerated growth is attributed to the increasing research and development activities and growing awareness about CRISPR technology across various applications. The segment's expansion is supported by the wide-ranging presence of innovative tools and CRISPR gene editing kits for gene modification experiments, fulfilling the growing need for genome editing solutions. The development of comprehensive CRISPR kits that enhance the efficiency of gene editing processes has also contributed to the segment's rapid growth. Furthermore, several companies are actively engaged in launching new products and forming strategic partnerships to expand their CRISPR kits and reagents portfolio, driving the segment's exceptional growth trajectory.

The CRISPR Technology Market Report is Segmented by Product (Enzymes, and More), Service (gRNA Design & Synthesis, Cell Line Engineering, and More), Technology (CRISPR/Cas9, and More), Application (Biomedical, and More), End User (Pharmaceutical & Biotechnology Companies, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 42.56% of 2024 revenue, driven by mature venture funding, favorable reimbursement, and clear FDA guidance that de-risks clinical investment. Boston, San Francisco, and San Diego anchor ecosystems where CRISPR Therapeutics, Editas Medicine, and Beam Therapeutics run multi-indication pipelines. The 2025 National Biotechnology Initiative Act expands tax credits for GMP capacity, strengthening domestic supply chains and cementing regional dominance.

Asia-Pacific is the fastest-growing region at 20.34% CAGR to 2030, led by China's multi-billion-dollar synthetic-biology parks and relaxed rules for gene-edited crops. Australia's roadmap foresees AUD 30 billion value by 2040 and funds industrial enzymes, while Singapore subsidizes GMP suites to lure global clinical-trial production. India's contract-research sector leverages cost advantages and skilled labor to capture discovery outsourcing, broadening regional participation in the CRISPR technology market.

Europe remains influential through deep regulatory expertise and generous public grants. The United Kingdom's GBP 100 million Engineering Biology fund finances fermentation hubs, and the EU-backed SYNBEE accelerator spans 25 nations, nurturing start-ups in food and environmental editing. EMA guidelines standardize genome-editing submissions, providing predictability despite stringent data demands. Central-eastern EU members court agricultural trials on climate-resilient wheat and maize, reflecting a pan-continental spread of CRISPR technology market applications.

- Thermo Fisher Scientific

- Merck

- Danaher (IDT)

- Agilent Technologies

- Genscript

- PerkinElmer (Horizon Discovery)

- New England Biolabs

- Cellecta

- Origene Technologies

- Synthego

- CRISPR Therapeutic

- Editas Medicine

- Intellia Therapeutics

- Caribou Biosciences

- Beam Therapeutics

- Sangamo Therapeutics

- Precision Biosciences

- ERS Genomics

- Takara Bio

- Integrated Micro-Biome Therapeutics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope Of The Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Clinical Pipeline For Genetic Disorders

- 4.2.2 Surge In Agri-Biotech Gene-Edited Crop Approvals

- 4.2.3 Falling Genome Editing Costs And Tool Democratization

- 4.2.4 Strategic Pharma-Biotech Alliances For In-Vivo CRISPR Therapies

- 4.2.5 AI-Enabled Functional Genomics Discovery Acceleration

- 4.2.6 Government Bioeconomy Programs Supporting Synthetic Biology Scale-Up

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Scrutiny And Evolving Compliance Frameworks

- 4.3.2 Unresolved Ethical Concerns Around Germline Editing

- 4.3.3 Complex Intellectual Property Landscape And Litigation Risks

- 4.3.4 Limited Delivery Modalities For In-Vivo Editing

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat Of New Entrants

- 4.6.2 Bargaining Power Of Buyers

- 4.6.3 Bargaining Power Of Suppliers

- 4.6.4 Threat Of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Enzymes

- 5.1.2 Kits & Reagents

- 5.1.3 Guide RNA

- 5.1.4 CRISPR Libraries

- 5.1.5 Design Tools / Software

- 5.1.6 Other Products

- 5.2 By Service

- 5.2.1 gRNA Design & Synthesis

- 5.2.2 Cell Line Engineering

- 5.2.3 Animal Model Generation

- 5.2.4 CRISPR Screening Services

- 5.2.5 Other Services

- 5.3 By Technology

- 5.3.1 CRISPR/Cas9

- 5.3.2 CRISPR/Cas12

- 5.3.3 CRISPR/Cas13

- 5.3.4 Base Editing

- 5.3.5 Prime Editing

- 5.3.6 Other Technologies

- 5.4 By Application

- 5.4.1 Biomedical

- 5.4.2 Agricultural

- 5.4.3 Industrial Biotechnology

- 5.4.4 Environmental & Synthetic Biology

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Pharmaceutical & Biotechnology Companies

- 5.5.2 Academic & Government Research Institutes

- 5.5.3 Contract Research Organizations

- 5.5.4 Other End Users

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Thermo Fisher Scientific

- 6.3.2 Merck KGaA

- 6.3.3 Danaher (IDT)

- 6.3.4 Agilent Technologies

- 6.3.5 GenScript

- 6.3.6 PerkinElmer (Horizon Discovery)

- 6.3.7 New England Biolabs

- 6.3.8 Cellecta

- 6.3.9 Origene Technologies

- 6.3.10 Synthego

- 6.3.11 CRISPR Therapeutics

- 6.3.12 Editas Medicine

- 6.3.13 Intellia Therapeutics

- 6.3.14 Caribou Biosciences

- 6.3.15 Beam Therapeutics

- 6.3.16 Sangamo Therapeutics

- 6.3.17 Precision Biosciences

- 6.3.18 ERS Genomics

- 6.3.19 Takara Bio

- 6.3.20 Integrated Micro-Biome Therapeutics

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment