PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1905990

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1905990

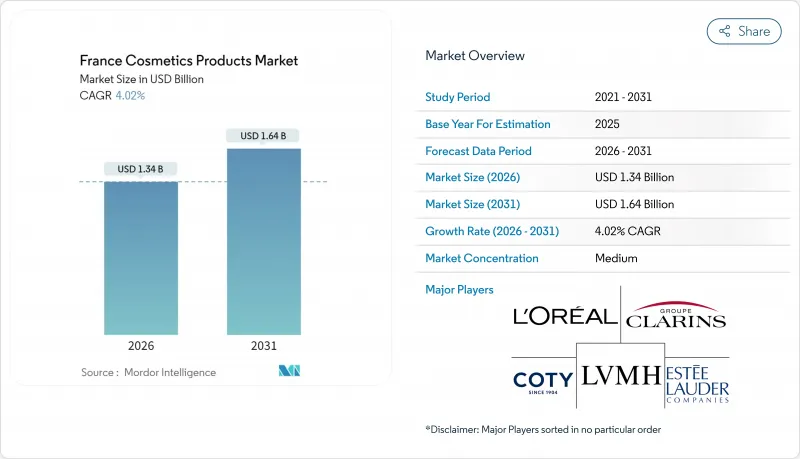

France Cosmetics Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The France cosmetics products market is expected to grow from USD 1.29 billion in 2025 to USD 1.34 billion in 2026 and is forecast to reach USD 1.64 billion by 2031 at 4.02% CAGR over 2026-2031.

Pharmacy sales continue to strengthen as consumers favor clinically backed actives and pharmacist recommendations, while digital channels expand reach and fuel direct-to-consumer growth; L'Oreal generated 28.2% of domestic sales online in 2024, and Yves Rocher aims to double its current 10% online share within three years. Innovation in ingredients remains a key catalyst, with launches such as BASF's Pepsensyal peptide and Clariant's CycloRetin providing evidence-based anti-aging benefits that support premium pricing.

France Cosmetics Products Market Trends and Insights

Surge in online beauty commerce

French health and beauty e-commerce expanded rapidly in 2024, with 32% of internet users purchasing online in Q2, and overall e-commerce grew 15% year-on-year. Cosmetics captured an outsized share, thanks to personalized diagnostics and subscription models that mass retailers cannot match, according to the French E-commerce Federation. L'Oreal's e-commerce penetration reached 28.2% in 2024, demonstrating how heritage brands are shifting online. Meanwhile, Yves Rocher's September 2024 marketplace launch aims to double its online revenue share to 20% within three years by aggregating third-party beauty labels. Digital acceleration is also fueling direct-to-consumer disruptors, such as Typology Paris, which are winning over younger consumers who prioritize ingredient transparency and interactive digital experiences over traditional branding. Amazon's move into physical parapharmacy further blurs channel boundaries, pressuring incumbents to invest in omnichannel fulfillment and real-time inventory visibility. Meanwhile, regulation is tightening: the European Commission's forthcoming Digital Product Passport, under the Ecodesign Regulation, will require end-to-end traceability, favoring digitally native brands that are already equipped with granular product data infrastructure.

Premiumization of make-up products

Louis Vuitton's Autumn 2025 debut of La Beaute, a collection comprising 55 lipsticks, 10 balms, and 8 eyeshadow palettes created in collaboration with Pat McGrath, illustrates how luxury fashion houses increasingly view makeup as a high-margin, brand-extending category that requires far less capital investment than leather goods, according to Vogue Business. Premium beauty products are expanding at a 5.96% CAGR through 2030, outpacing mass-market offerings because they command 2-3X higher price points while maintaining broadly similar formulation and packaging cost structures. Department stores report that in 2023, luxury items represented 50% of beauty sales, compared with 20% for premium and 11% for prestige products, underscoring the outsize spending power of the top consumer quintile, according to the International Association of Department Stores (IADS). This premiumization is especially evident in color cosmetics, where lip and eye makeup lead department-store beauty sales. Trends showcased during Paris Fashion Week 2025, including deep reds, burgundies, and plums, are fueling demand for high-ticket, limited-edition launches that routinely sell out within weeks.

Stringent EU and French ingredient regulations

The regulatory environment for cosmetics in France and the EU imposes a complex, multi-layered compliance burden that elevates market-entry costs and slows innovation. Oversight by France's ANSES, DGCCRF, and ANSM complements the European Commission's Cosmetics Regulation, with DGCCRF assuming responsibility for Good Manufacturing Practice controls in January 2024, adding a domestic enforcement layer atop EU-wide rules (DGCCRF). Safety Gate 2024 reported that 36% of product alerts involved cosmetics, frequently citing banned fragrance allergen butylphenyl methylpropional, undeclared allergens, microbiological contamination, and heavy metals, highlighting widespread compliance risks amid intensifying enforcement. Furthermore, the European Commission's Recommendation 2024/915 on anti-counterfeiting measures and the forthcoming Digital Product Passport under the Ecodesign Regulation will mandate end-to-end supply chain traceability, favoring large, digitally mature companies over smaller producers (ECHA). Ingredient-level regulatory changes, such as the ECHA Risk Assessment Committee's proposed classification of p-cymene as Repr. 1B would restrict essential oils and necessitate reformulation across hundreds of SKUs, demonstrating how granular regulations cascade through portfolios. While these measures enhance consumer safety, they impose an estimated -0.6% drag on CAGR by delaying product launches, raising formulation costs, and creating entry barriers that protect incumbents at the expense of innovation.

Other drivers and restraints analyzed in the detailed report include:

- Shift to natural and organic formulations

- Pharmacy-led dermocosmetic boom

- High cost of natural and sustainable inputs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Facial cosmetics accounted for 42.74% of the French market in 2025, remaining the largest segment due to foundations, concealers, and skincare-makeup hybrids that benefit from the dermocosmetic boom. However, eye cosmetics are projected to grow at a 5.52% CAGR through 2031, the fastest among product types, driven by Paris Fashion Week 2025 trends such as metallic accents, reverse eyeliner, and icy/frosted eyeshadows, which accelerate product innovation cycles (MakeUp in Paris). Luxury entrants are emphasizing this category: Louis Vuitton's La Beaute autumn 2025 launch includes 8 eyeshadow palettes alongside 55 lipsticks and 10 balms, reflecting the high-margin, high-repurchase potential of eye makeup (Vogue Business).

Shifts from glass skin to soft matte finishes and the return of brown tones are micro-trends that increase SKU proliferation and shorten product life cycles, favoring brands with agile supply chains and digital-first distribution. L'Oreal's mass-market adaptations, such as Cool Silver, Revitalift Laser, and Bright Reveal SPF50, illustrate how runway-inspired innovation quickly cascades to drugstore shelves, compressing the trend-to-market cycle. Facial-care innovation increasingly relies on mechanism-based formulations, as seen with Beiersdorf's Nivea Q10 Dual Action serum launched in April 2024, which incorporates anti-glycation technology and clinical substantiation, creating barriers that protect incumbents. By contrast, eye cosmetics are more trend-driven and lightly regulated, enabling faster product cycles and lower entry barriers, explaining their higher growth despite a smaller market share and why premium brands are disproportionately investing in this category to capture younger, trend-conscious consumers.

Mass cosmetics accounted for 56.10% of the French market in 2025, reflecting broad accessibility and appeal to price-sensitive consumers through supermarkets, hypermarkets, and drugstores. However, premium products are expanding at a 5.78% CAGR through 2031, driven by consumers trading up to higher-priced, efficacy-backed offerings even as mass volume growth slows. Luxury entrants signal this strategic pivot: Louis Vuitton's La Beaute launch, Balmain Beauty's EUR 250 (USD 272) fragrances, and Estee Lauder's Paris fragrance atelier opening in 2025 demonstrate that fashion houses are leveraging brand equity and customer loyalty to capture a greater share of the cosmetics market. French consumers' strong brand literacy and willingness to pay for provenance and craftsmanship reinforce this trend.

Mass brands retain a majority share because of their widespread distribution and affordability, yet growth is increasingly concentrated in premium and dermocosmetic segments. L'Oreal's Dermatological Beauty division grew 9.8% in 2024, outpacing its mass-market brands Garnier, Maybelline, and L'Oreal Paris, while Yves Rocher's EUR 1.2 billion (USD 1.31 billion) revenue and target to double online sales to 20% within three years highlight mid-tier brands' investment in digital channels to compete on convenience and personalization. The mass-to-premium shift varies by product type, sunscreen remains 50% pharmacy-distributed, maintaining a structural advantage for dermocosmetics, but overall, French consumers are increasingly willing to pay a premium for clinical efficacy, ingredient transparency, and brand prestige.

The France Cosmetics Products Market Report is Segmented by Product Type (Facial Cosmetics, Eye Cosmetics, Lip and Nail Make-Up Products), Category (Premium Products, Mass Products), Ingredient Type (Natural/Organic, Conventional/Synthetic), and Distribution Channel (Specialty Stores, Supermarkets/Hypermarkets, Online Retail Stores, Other Channels). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- L'Oreal S.A.

- LVMH Moet Hennessy Louis Vuitton

- Coty Inc.

- Groupe Clarins S.A.

- Pierre Fabre Dermo-Cosmetique

- Beiersdorf AG

- The Estee Lauder Companies

- Shiseido Co. Ltd.

- Yves Rocher (Groupe Rocher)

- L'Occitane International S.A.

- Nuxe Laboratoire

- Laboratoires NAOS

- Laboratoires Expanscience

- Kiko France SARL

- Typology Paris

- Unilever France

- The Procter & Gamble Company

- Puig SL

- Pulpe de Vie

- In'oya Laboratory

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in online beauty commerce

- 4.2.2 Premiumisation of make-up products

- 4.2.3 Shift to natural and organic formulations

- 4.2.4 Pharmacy-led dermocosmetic boom

- 4.2.5 Scientific and active ingredient innovation

- 4.2.6 Growth of microbiome-friendly and sensitive-skin products

- 4.3 Market Restraints

- 4.3.1 Stringent EU and French ingredient regulations

- 4.3.2 High cost of natural and sustainable inputs

- 4.3.3 Counterfeit products impact premium segments

- 4.3.4 Rising raw material price volatility

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Facial Cosmetics

- 5.1.2 Eye Cosmetics

- 5.1.3 Lip and Nail Make-up Products

- 5.2 By Category

- 5.2.1 Premium Products

- 5.2.2 Mass Products

- 5.3 By Ingredient Type

- 5.3.1 Natural/Organic

- 5.3.2 Conventional/Synthetic

- 5.4 By Distribution Channel

- 5.4.1 Specialty Stores

- 5.4.2 Supermarkets/Hypermarkets

- 5.4.3 Online Retail Stores

- 5.4.4 Other Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 L'Oreal S.A.

- 6.4.2 LVMH Moet Hennessy Louis Vuitton

- 6.4.3 Coty Inc.

- 6.4.4 Groupe Clarins S.A.

- 6.4.5 Pierre Fabre Dermo-Cosmetique

- 6.4.6 Beiersdorf AG

- 6.4.7 The Estee Lauder Companies

- 6.4.8 Shiseido Co. Ltd.

- 6.4.9 Yves Rocher (Groupe Rocher)

- 6.4.10 L'Occitane International S.A.

- 6.4.11 Nuxe Laboratoire

- 6.4.12 Laboratoires NAOS

- 6.4.13 Laboratoires Expanscience

- 6.4.14 Kiko France SARL

- 6.4.15 Typology Paris

- 6.4.16 Unilever France

- 6.4.17 The Procter & Gamble Company

- 6.4.18 Puig SL

- 6.4.19 Pulpe de Vie

- 6.4.20 In'oya Laboratory

7 MARKET OPPORTUNITIES AND FUTURE TRENDS