PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906159

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906159

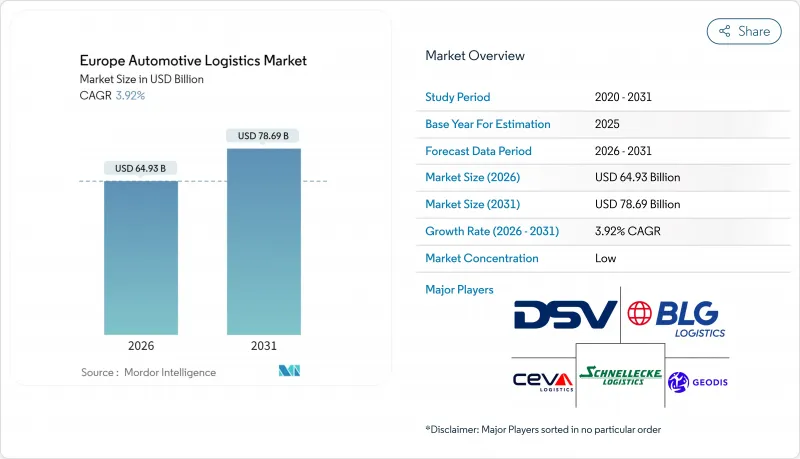

Europe Automotive Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Europe Automotive Logistics Market size in 2026 is estimated at USD 64.93 billion, growing from 2025 value of USD 62.48 billion with 2031 projections showing USD 78.69 billion, growing at 3.92% CAGR over 2026-2031.

The outlook emerges as OEMs, 3PLs, and technology specialists reshape networks around electrification, digital orchestration, and rigorous decarbonization mandates. Transportation services remain pivotal, yet rapid demand for temperature-controlled battery flows and high-frequency e-commerce parts fulfillment is refocusing investment toward value-added capabilities. Integrated 3PL/4PL partnerships, multimodal optimization, and automation adoption drive operational resilience while capacity constraints in road and rail continue to temper margin expansion. Germany anchors regional revenue, but Poland's warehouse boom underscores a geographic rebalancing that rewards agile providers with pan-European reach.

Europe Automotive Logistics Market Trends and Insights

OEMs' Rising Outsourcing to Integrated 3PL/4PL Specialists

European manufacturers increasingly channel end-to-end logistics to strategic partners that fuse physical and digital competencies. Volkswagen and BMW deepen multi-year agreements with providers capable of orchestrating inbound parts, just-in-sequence plant deliveries, and outbound finished-vehicle distribution across borders. Kuehne+Nagel and DHL Supply Chain answer by expanding Automotive Solution Centers that unify transport planning, control-tower analytics, and sustainability reporting. Certifications under ISO 14001 and IATF 16949 elevate selection thresholds, directing share toward providers with quality and environmental credentials. The Europe automotive logistics market benefits as OEM capital shifts from asset ownership to electrification R&D, leaving logistics innovation to specialized experts. Outsourcing also buffers production volatility by allowing variable-cost contracts that scale with demand peaks and troughs.

Surge in EV Production Requiring Temperature-Controlled Battery Logistics

Gigafactory clusters in Hungary, Germany, and Poland accelerate demand for 15-25 °C controlled supply chains that safeguard lithium-ion cell integrity. DHL's EV Centers of Excellence in Italy and the UK showcase purpose-built storage with fire-suppression systems, ADR-compliant packaging, and real-time thermal monitoring. Logistics providers invest in insulated swap bodies, electric shuttles, and redundant power backup to guarantee temperature stability during cross-border transits. The Europe automotive logistics market thus funnels capex into specialized fleet assets and warehouse retrofits that command premium pricing. Battery OEMs such as CATL extend direct control over inbound and reverse flows, leveraging in-region service hubs to curtail transit time and uphold warranty standards.

Driver & Capacity Shortages in European Road/Rail Freight

A deficit exceeding 80,000 professional drivers in Germany strains just-in-time automotive flows and inflates wage costs. Low appeal of long-haul careers among younger cohorts compounds attrition, while infrastructure works and passenger priority squeeze rail freight slots. Logistics firms adopt retention bonuses, flexible scheduling, and autonomous yard tractors to sustain service levels. The Europe automotive logistics market experiences spot-rate volatility as capacity swings trigger premium surcharges. OEMs respond by increasing safety-stock buffers and exploring cross-docking near plants to dampen schedule risk.

Other drivers and restraints analyzed in the detailed report include:

- After-Sales E-Commerce Boosting Small-Lot, High-Frequency Flows

- EU Green Deal Incentives for Multimodal Freight & CO2 Cuts

- Rising Fuel and Labor Costs Squeezing Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation accounted for a 61.35% share of the Europe automotive logistics market in 2025, anchored by road haulage flexibility that meets stringent just-in-sequence production cadences. Rail and short-sea alternatives gain relevance on longer corridors as carbon pricing steers modal recalibration. Meanwhile, value-added services, though smaller, are expanding at a 3.52% CAGR (2026-2031), driven by pre-delivery inspection, EV battery conditioning, and control-tower orchestration. Providers elevate service mix through robotics-enabled cross-docks and digital twins that optimize dwell time and yard capacity. By 2031, value-added offerings will underpin margin resilience as commoditized line-haul rates remain under pressure, thereby entrenching integrated partners across the Europe automotive logistics market.

A parallel upswing is visible in warehousing, where automation increases throughput for multi-SKU part inventories. ISO 9001 and IATF 16949 certifications govern provider selection, ensuring traceability across inbound, line-side sequencing, and aftermarket replenishment. Smart racking, AGV fleets, and RFID scanning compress cycle times, reinforcing the Europe automotive logistics market size growth trajectory for service layers beyond core transport.

The Europe Automotive Logistics Market Report is Segmented by Service (Transportation, Warehousing, Distribution & Inventory Management, and Value-Added Services), Type (OEM and Aftermarket), Cargo Type (Finished Vehicles, Auto Components, EV Batteries & Power-Electronics, and Other Cargo), Country (Germany, Spain, France, Italy, United Kingdom, Poland, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- BLG Logistics

- CEVA Logistics AG

- DSV

- Schnellecke Logistics

- GEODIS

- Nippon Express Co., Ltd

- XPO Logistics, Inc.

- DHL Supply Chain

- Kuehne + Nagel

- Hellmann Worldwide Logistics

- Wallenius Wilhelmsen Logistics

- Yusen Logistics

- CAT Group

- FIEGE Automotive

- Ryder System, Inc.

- Rohlig Logistics

- Rhenus Logistics

- Scan Global Logistics

- LOGISTEED Europe B.V.

- TOP AUTO Logistik GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 OEMs' rising outsourcing to integrated 3PL/4PL specialists

- 4.2.2 Surge in EV production requiring temperature-controlled battery logistics

- 4.2.3 After-sales e-commerce boosting small-lot, high-frequency flows

- 4.2.4 EU Green Deal incentives for multimodal freight & CO2 cuts

- 4.2.5 Semiconductor & software-defined vehicle parts creating new high-value flows

- 4.2.6 Emergence of regional battery-recycling corridors (OEM-to-gigafactory reverse loops)

- 4.3 Market Restraints

- 4.3.1 Driver & capacity shortages in European road/rail freight

- 4.3.2 Rising fuel and labor costs squeezing margins

- 4.3.3 Ro-Ro vessel scarcity causing port congestion for finished vehicles

- 4.3.4 Cyber-security vulnerabilities in connected logistics platforms

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape (Government Regulations & Initiatives)

- 4.6 Technological Outlook (Automation, IoT, AI, Blockchain)

- 4.7 Spotlight - E-commerce Impact on Automotive Logistics

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Impact of Geo-Political Events

5 Market Size & Growth Forecasts

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Air

- 5.1.1.4 Sea / Ro-Ro / Short-Sea

- 5.1.2 Warehousing, Distribution & Inventory Management

- 5.1.3 Value-added Services

- 5.1.1 Transportation

- 5.2 By Type

- 5.2.1 OEM

- 5.2.2 Aftermarket

- 5.3 By Cargo Type

- 5.3.1 Finished Vehicles

- 5.3.2 Auto Components

- 5.3.3 EV Batteries and Power-Electronics

- 5.3.4 Other Cargo

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 Spain

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Poland

- 5.4.6 United Kingdom

- 5.4.7 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.8 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.4.1 BLG Logistics

- 6.4.2 CEVA Logistics AG

- 6.4.3 DSV

- 6.4.4 Schnellecke Logistics

- 6.4.5 GEODIS

- 6.4.6 Nippon Express Co., Ltd

- 6.4.7 XPO Logistics, Inc.

- 6.4.8 DHL Supply Chain

- 6.4.9 Kuehne + Nagel

- 6.4.10 Hellmann Worldwide Logistics

- 6.4.11 Wallenius Wilhelmsen Logistics

- 6.4.12 Yusen Logistics

- 6.4.13 CAT Group

- 6.4.14 FIEGE Automotive

- 6.4.15 Ryder System, Inc.

- 6.4.16 Rohlig Logistics

- 6.4.17 Rhenus Logistics

- 6.4.18 Scan Global Logistics

- 6.4.19 LOGISTEED Europe B.V.

- 6.4.20 TOP AUTO Logistik GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment