PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906885

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906885

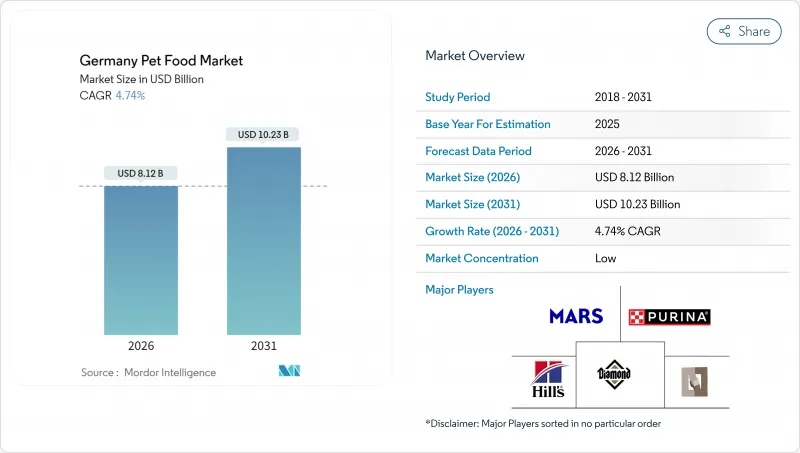

Germany Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Germany pet food market is expected to grow from USD 7.75 billion in 2025 to USD 8.12 billion in 2026 and is forecast to reach USD 10.23 billion by 2031 at 4.74% CAGR over 2026-2031.

This current size and growth trajectory reflect the country's position as the largest national segment within European pet care. In 2024, expansion is fueled by high ownership of 34.4 million companion animals and strong household spending on premium nutrition, functional treats, and veterinary-endorsed diets . Rising disposable income, demographic shifts toward single-person households, and the rapid uptake of digital purchase paths sustain demand momentum, while regulatory emphasis on clean-label ingredients reinforces consumer trust. Producers capitalize on premiumization, regenerative agriculture sourcing, and omnichannel reach, whereas discounters and private-label innovations intensify price competition. Cost volatility for poultry, grains, and specialty proteins introduces margin pressure, yet robust brand equity in premium formats enables selective price pass-through.

Germany Pet Food Market Trends and Insights

Premiumization and Human-Grade Formulations

The humanization of pet nutrition drives the most significant market expansion, as in 2023, 48% of German consumers expressed willingness to pay premium prices for sustainable and human-grade formulations. This trend transcends traditional price sensitivity, with pet owners increasingly scrutinizing ingredient transparency and sourcing practices similar to their own food choices. Mars Petcare's multi-year partnerships across European supply chains aim to target 20,900 hectares of regenerative agriculture by 2028, positioning the company to capture premium positioning through traceable, sustainable ingredients. The shift creates margin expansion opportunities for manufacturers who can demonstrate clean-label credentials, while traditional value-focused brands face pressure to reformulate or risk losing market share.

Surge in Single-Person Households

Germany's demographic shift toward single-person households is fundamentally reshaping pet ownership economics, with these households representing pet ownership rates of 34% compared to 23% in multi-person households in 2023. Single pet owners exhibit higher per-pet spending patterns, allocating a disproportionate share of their income to premium nutrition and health-focused products that serve as substitutes for human companionship needs. This demographic shift particularly benefits functional diet categories, as single households often view pets as primary family members deserving equivalent nutritional investment. The trend accelerates in urban centers where housing costs limit family formation, creating concentrated markets for premium pet nutrition.

Rising Raw-Meat and Grain Prices

Volatile commodity markets create margin compression pressures that manufacturers struggle to pass on to price-sensitive consumer segments, with fluctuations in poultry and cereal costs reducing industry profitability by an estimated 0.9% points annually . German pet food manufacturers face particular vulnerability due to high-quality ingredient sourcing requirements that limit substitution flexibility compared to human food applications. Supply chain disruptions stemming from geopolitical tensions and climate-related crop failures exacerbate price volatility, compelling manufacturers to implement hedging strategies or accept margin variability. The constraint particularly impacts value-oriented segments where price elasticity limits pass-through capabilities, while premium brands maintain pricing power through brand loyalty and perceived quality differentiation.

Other drivers and restraints analyzed in the detailed report include:

- Veterinary Endorsement of Functional Diets

- Expansion of Private-Label Super-Premium Lines

- Stringent German Feed Additive Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The traditional pet food segment maintains a dominant 67.85% market share in 2025, showing steady but moderate growth. This segment's stability stems from consistent pet feeding requirements and the ongoing transition from home-cooked to commercial pet food products. The market benefits from Germany's growing pet population and increased pet humanization, as owners prioritize high-quality commercial food products for their pets' daily nutrition. Dry pet food, including kibbles and alternative formats, adapts through premiumization strategies that incorporate functional ingredients, grain-free formulations, and human-grade sourcing to maintain relevance against the growing trends of fresh and raw feeding.

Pet treats are projected to demonstrate robust growth potential with a 7.28% CAGR through 2031. This growth is primarily driven by increased treat usage in dog training and reward systems. Product innovation, including dental treats, freeze-dried options, and functional varieties with health benefits, supports market expansion. Freeze-dried and jerky treats gain traction due to their use of human-grade ingredients and clean-label formulations, while dental treats benefit from veterinary recommendations. The segment's growth is further supported by rising awareness of positive reinforcement training methods and increasing demand for premium, natural treat options.

The Germany Pet Food Market Report is Segmented by Pet Food Product (Food, Pet Nutraceuticals/Supplements, Pet Treats, and Pet Veterinary Diets), by Pets (Cats, Dogs, and Other Pets), by Distribution Channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets, and Other Channels). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- Mars, Incorporated

- Nestle (Purina)

- Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.)

- General Mills Inc.

- Affinity Petcare S.A

- Schell & Kampeter, Inc. (Diamond Pet Foods)

- Heristo aktiengesellschaft

- Clearlake Capital Group, L.P. (Wellness Pet Company, Inc.)

- Alltech

- Virbac

- Mera Tiernahrung GmbH

- Farmina Pet Foods Holding Ltd. (Russo Family)

- Bosch Tiernahrung GmbH and Co. KG

- United Petfood Group

- Deuerer GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Consumer Trends

5 SUPPLY AND PRODUCTION DYNAMICS

- 5.1 Trade Analysis

- 5.2 Ingredient Trends

- 5.3 Value Chain & Distribution Channel Analysis

- 5.4 Regulatory Framework

- 5.5 Market Drivers

- 5.5.1 Premiumization and human-grade formulations

- 5.5.2 Surge in single-person households

- 5.5.3 Veterinary endorsement of functional diets

- 5.5.4 Expansion of private-label super-premium lines

- 5.5.5 In-store fresh frozen rollouts by German discounters

- 5.5.6 DTC subscription services with AI-based meal plans

- 5.6 Market Restraints

- 5.6.1 Rising raw-meat and grain prices

- 5.6.2 Stringent German feed additive regulations

- 5.6.3 Vet-Led pushback on grain-free diet claims

- 5.6.4 Consumer skepticism toward insect protein

6 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 6.1 Pet Food Product

- 6.1.1 Food

- 6.1.1.1 By Sub Product

- 6.1.1.1.1 Dry Pet Food

- 6.1.1.1.1.1 By Sub Dry Pet Food

- 6.1.1.1.1.1.1 Kibbles

- 6.1.1.1.1.1.2 Other Dry Pet Food

- 6.1.1.1.1.1 By Sub Dry Pet Food

- 6.1.1.1.2 Wet Pet Food

- 6.1.1.1.1 Dry Pet Food

- 6.1.1.1 By Sub Product

- 6.1.2 Pet Nutraceuticals/Supplements

- 6.1.2.1 By Sub Product

- 6.1.2.2 Milk Bioactives

- 6.1.2.3 Omega-3 Fatty Acids

- 6.1.2.4 Probiotics

- 6.1.2.5 Proteins and Peptides

- 6.1.2.6 Vitamins and Minerals

- 6.1.2.7 Other Nutraceuticals

- 6.1.3 Pet Treats

- 6.1.3.1 By Sub Product

- 6.1.3.1.1 Crunchy Treats

- 6.1.3.1.2 Dental Treats

- 6.1.3.1.3 Freeze-dried and Jerky Treats

- 6.1.3.1.4 Soft & Chewy Treats

- 6.1.3.1.5 Other Treats

- 6.1.3.1 By Sub Product

- 6.1.4 Pet Veterinary Diets

- 6.1.4.1 By Sub Product

- 6.1.4.1.1 Diabetes

- 6.1.4.1.2 Digestive Sensitivity

- 6.1.4.1.3 Oral Care Diets

- 6.1.4.1.4 Renal

- 6.1.4.1.5 Urinary tract disease

- 6.1.4.1.6 Derma Diets

- 6.1.4.1.7 Obesity Diets

- 6.1.4.1.8 Other Veterinary Diets

- 6.1.4.1 By Sub Product

- 6.1.1 Food

- 6.2 Pets

- 6.2.1 Cats

- 6.2.2 Dogs

- 6.2.3 Other Pets

- 6.3 Distribution Channel

- 6.3.1 Convenience Stores

- 6.3.2 Online Channel

- 6.3.3 Specialty Stores

- 6.3.4 Supermarkets/Hypermarkets

- 6.3.5 Other Channels

7 COMPETITIVE LANDSCAPE

- 7.1 Key Strategic Moves

- 7.2 Market Share Analysis

- 7.3 Brand Positioning Matrix

- 7.4 Market Claim Analysis

- 7.5 Company Landscape

- 7.6 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 7.6.1 Mars, Incorporated

- 7.6.2 Nestle (Purina)

- 7.6.3 Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.)

- 7.6.4 General Mills Inc.

- 7.6.5 Affinity Petcare S.A

- 7.6.6 Schell & Kampeter, Inc. (Diamond Pet Foods)

- 7.6.7 Heristo aktiengesellschaft

- 7.6.8 Clearlake Capital Group, L.P. (Wellness Pet Company, Inc.)

- 7.6.9 Alltech

- 7.6.10 Virbac

- 7.6.11 Mera Tiernahrung GmbH

- 7.6.12 Farmina Pet Foods Holding Ltd. (Russo Family)

- 7.6.13 Bosch Tiernahrung GmbH and Co. KG

- 7.6.14 United Petfood Group

- 7.6.15 Deuerer GmbH

8 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS