PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906915

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906915

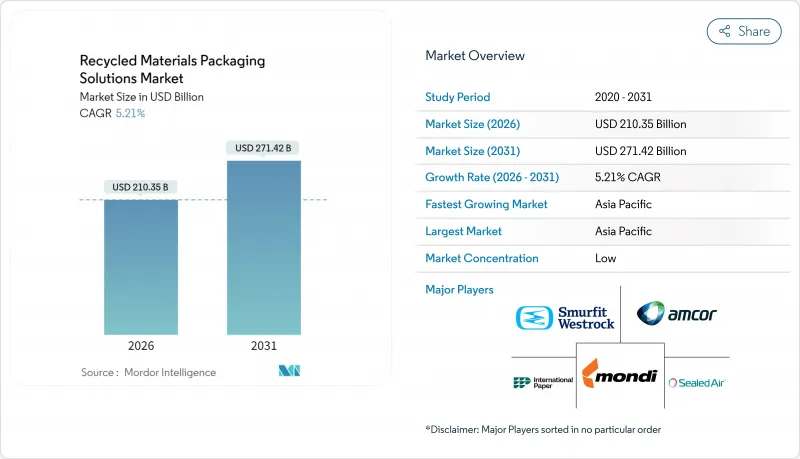

Recycled Materials Packaging Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The recycled materials packaging solutions market size in 2026 is estimated at USD 210.35 billion, growing from 2025 value of USD 199.93 billion with 2031 projections showing USD 271.42 billion, growing at 5.21% CAGR over 2026-2031.

Rising Extended Producer Responsibility mandates, brand-owner recycled-content targets, and investments in artificial-intelligence sortation are collectively positioning the recycled materials packaging solutions market for sustained growth. Asia-Pacific secures early-mover advantages through evolving regulations and large-scale infrastructure projects, while North America and Europe build capacity through chemical recycling and vertically integrated feedstock procurement. Demand is reinforced by consumers willing to pay premiums for low-carbon packaging, which smooths cost differentials between recycled and virgin materials. At the same time, supply-side innovations such as dissolution-based recycling and mono-material flexible pouches are narrowing performance gaps against incumbent virgin solutions.

Global Recycled Materials Packaging Solutions Market Trends and Insights

Extended Producer Responsibility (EPR) Mandates Expansion

EPR statutes shift end-of-life costs from municipalities to producers, making recycled content economically attractive. Vietnam's 2024 rules require 22% recycling for rigid PET and 40% material recovery rates, sparking rapid equipment upgrades. South Korea is boosting the required recycled plastic in PET bottles from 3% to 10% and targets 30% by 2030. Thailand's label-free PET initiative trims contamination and considers tax credits for recycled resin. The EU Packaging and Packaging Waste Regulation mandates 30% recycled PET in food packaging by 2030. India now allows specified recycled plastics in food packaging, requiring traceability labelling.

Brand-Owner 2025 Recycled-Content Targets

Global brands are voluntarily outpacing regulation. Estee Lauder seeks at least 25% PCR and to halve virgin plastic by 2030. Mars moved key confectionery jars to 100% recycled resin, cutting 1,300 tonnes of virgin plastic each year. Mondelez will package 300 million Cadbury sharing bars in 80% attributable recycled plastic. Cadbury Australia sourced 1,000 tonnes of chemically recycled polypropylene for Dairy Milk bars.

Volatile Supply of High-Quality Recycled Feedstock

Pricing for recycled PET and high-density polyethylene swings widely, imposing budgeting challenges for converters. Beverage brands recently queued 6-8 weeks for food-grade rPET while virgin alternatives were available in 3 weeks. Contamination means 15-25% of collected plastics fail food-grade tests, forcing some brands to under-fulfill recycled-content pledges. The volatility is most acute for barrier materials that demand specialty grades.

Other drivers and restraints analyzed in the detailed report include:

- Advanced Sortation Technologies: Reducing Contamination

- Consumer Preference for Low-Carbon Packaging

- Competing Demand from Fiber-Based Substitute Packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, paper commanded 44.25% of the recycled materials packaging solutions market share, reflecting mature fiber collection systems and corrugated recovery rates above 90% in North America. Plastic is projected to post a 6.03% CAGR through 2031 as chemical recycling improves food-grade quality and unlocks new applications. Glass continues serving premium beverage and cosmetic niches where brand equity values tactile heft. Metal offers infinite recyclability that attracts closed-loop purchasers, buttressing its role in aerosol, beverage, and cosmetics packaging even when volumes remain modest.

Paper maintains steady growth due to global e-commerce, but plastics claim future upside. Investment topping USD 8 billion accelerates chemical recycling to offset the shortfall in food-grade rPET. Examples such as Eastman's Gemini compact underscore plastics' progress into cosmetics using molecularly recycled resins. Consequently, the recycled materials packaging solutions market expects a gradual convergence in the material mix between paper and plastic solutions.

Food applications generated 36.20% of 2025 demand, but regulatory safety thresholds constrain growth. India's new allowance of specific recycled plastics in food packaging under strict traceability slightly relaxes barriers. Beverage brands such as PepsiCo demonstrate 50% recycled polypropylene snack packs, hinting at broader adoption where performance permits.

Home and personal care is set to rise at a 6.58% CAGR, as consumers accept premiums for low-carbon formats. Ball Corporation financed Meadow to launch fully recyclable aluminum cartridges for soaps and shampoos, showing brand readiness to switch materials swiftly. Secondary industries such as e-commerce and industrial packaging also incorporate more PCR as collection networks mature, broadening the recycled materials packaging solutions market.

The Recycled Materials Packaging Solutions Market Report is Segmented by Material Type (Plastic, Paper, Glass, and Metal), End-User Industry (Food, Beverage, Home and Personal Care, Healthcare, and More), Packaging Type (Rigid Packaging, and Flexible Packaging), Source of Recycled Material (Post-Consumer Recyclate, Post-Industrial Recyclate, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 45.80% of the recycled materials packaging solutions market size in 2025 and will grow at a 7.55% CAGR. Regulatory clarity, such as Vietnam's EPR targets, South Korea's recycled-content thresholds, and Thailand's tax incentives, is reinforcing investment flows. Infrastructure financing across ASEAN nations addresses collection bottlenecks, closing gaps that historically impeded supply consistency.

North America benefits from USD 8 billion in announced recycling expansions since 2017, adding capacity to process almost 9 million tonnes of waste annually. Extended Producer Responsibility laws in Oregon and Colorado that take effect in July 2025 clarify producer fees and spur redesign toward recyclability. Corporate procurement commitments secure offtake, supporting a stable investment outlook. Europe sustains regulatory leadership. Mandatory 30% recycled PET for food packaging by 2030 and design-for-recycling criteria foster innovation pipelines. Collaborative platforms such as 4evergreen and FINAT develop technical guidance for paper and label liner recycling, respectively. Moderate growth in South America and the Middle East & Africa reflects emerging grant funding and nascent EPR frameworks that gradually enlarge the recycled materials packaging solutions market.

- Amcor plc

- Kruger Inc.

- Smurfit WestRock plc

- Packaging Corporation of America

- Tetra Laval International S.A.

- International Paper Company

- Mondi plc

- Verallia SA

- Sealed Air Corporation

- Ardagh Group

- Plastipak Holdings, Inc.

- Billerud AB

- Stora Enso Oyj

- UPM-Kymmene Corporation

- Huhtamaki Oyj

- Graphic Packaging Holding Company

- Veolia Environnement S.A.

- Eco-Products, Inc.

- Loop Industries, Inc.

- Sonoco Products Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Extended Producer Responsibility (EPR) Mandates Expansion

- 4.2.2 Brand-Owner 2025 Recycled-Content Targets

- 4.2.3 Advanced Sortation Technologies: Reducing Contamination

- 4.2.4 Consumer Preference for Low-Carbon Packaging

- 4.2.5 Corporate Net-Zero Commitments Accelerating PCR Procurement

- 4.2.6 Surging Investment in Chemical Recycling Capacity

- 4.3 Market Restraints

- 4.3.1 Volatile Supply of High-Quality Recycled Feedstock

- 4.3.2 Competing Demand from Fiber-Based Substitute Packaging

- 4.3.3 Unfavorable Economics when Virgin Resin Prices Decline

- 4.3.4 Recycling Infrastructure Gaps in Emerging Markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Plastic

- 5.1.2 Paper

- 5.1.3 Glass

- 5.1.4 Metal

- 5.2 By End-User Industry

- 5.2.1 Food

- 5.2.2 Beverage

- 5.2.3 Home and Personal Care

- 5.2.4 Healthcare

- 5.2.5 Other End-user Industries

- 5.3 By Packaging Type

- 5.3.1 Rigid Packaging

- 5.3.2 Flexible Packaging

- 5.4 By Source of Recycled Material

- 5.4.1 Post-consumer Recyclate (PCR)

- 5.4.2 Post-industrial Recyclate (PIR)

- 5.4.3 Ocean-bound and Recovered Waste

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN Countries

- 5.5.4.6 Australia and New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Kruger Inc.

- 6.4.3 Smurfit WestRock plc

- 6.4.4 Packaging Corporation of America

- 6.4.5 Tetra Laval International S.A.

- 6.4.6 International Paper Company

- 6.4.7 Mondi plc

- 6.4.8 Verallia SA

- 6.4.9 Sealed Air Corporation

- 6.4.10 Ardagh Group

- 6.4.11 Plastipak Holdings, Inc.

- 6.4.12 Billerud AB

- 6.4.13 Stora Enso Oyj

- 6.4.14 UPM-Kymmene Corporation

- 6.4.15 Huhtamaki Oyj

- 6.4.16 Graphic Packaging Holding Company

- 6.4.17 Veolia Environnement S.A.

- 6.4.18 Eco-Products, Inc.

- 6.4.19 Loop Industries, Inc.

- 6.4.20 Sonoco Products Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment