PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907257

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907257

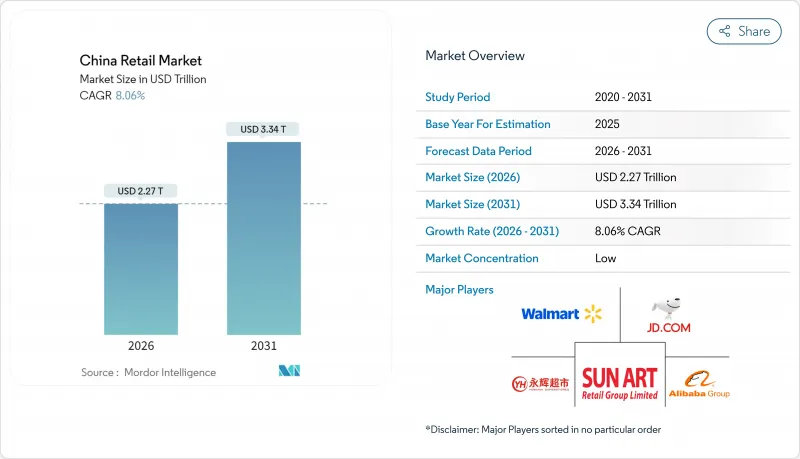

China Retail - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The China retail market is expected to grow from USD 2.1 trillion in 2025 to USD 2.27 trillion in 2026 and is forecast to reach USD 3.34 trillion by 2031 at 8.06% CAGR over 2026-2031.

This sustained expansion reflects resilient household demand, a steady rise in disposable income and deliberate public-policy efforts to encourage domestic consumption, including the designation of 2024 as "Consumption Promotion Year" and large-scale voucher programs in major cities. Live-stream commerce in lower-tier cities, warehouse-club expansion and tourism-linked duty-free spending add fresh momentum. Government pilots of the digital yuan and incentives for "Smart Retail" keep omnichannel investments high, while the silver-economy boom lifts premium health, wellness and leisure categories. A shrinking working-age population and tighter data-privacy rules act as headwinds, yet retailers that pivot to quality, service and technology still benefit from deep consumer pockets in key urban clusters.

China Retail Market Trends and Insights

Rapid Adoption of Social & Live-Stream Commerce in Lower-Tier Cities

Live-stream sales reached USD 694.5 billion in 2024 with interactive formats bridging trust gaps in smaller markets. More than 600 million shoppers tune in daily, fueling direct-to-consumer growth for brands that once relied on Tier 1 outlets. Scarcity messaging and real-time chat encourage impulse purchases, while lower logistics costs help retailers penetrate vast county-level areas. The model democratizes access to premium goods, sidesteps traditional hierarchies and lifts the overall China retail market through incremental demand.

Expansion of Membership-Based Warehouse Clubs Lifting Average Basket Size

Warehouse club sales topped CNY 300 billion in 2024, and Sam's Club alone added six outlets after notching 25% membership growth. High-quality, low-SKU assortments support bulk buying and predictable revenue streams. Curated imported food, smart appliances and private labels drive ticket sizes above traditional supermarkets, reinforcing the value-for-money narrative that resonates with the urban middle class.

Intensifying Price Wars on E-Commerce Platforms Eroding Retailer Margins

The escalation of price competition among China's e-commerce giants has created a destructive cycle that threatens long-term market sustainability, with the 618 shopping festival experiencing its first decline in eight years, dropping 7% to USD 102.3 billion in 2024. Market-cap erosion of USD 157 billion across consumer stocks illustrates investor concern over profitability. Major platforms now pivot to quality and merchant support, yet the margin squeeze persists as last-mile costs rise and consumers chase bargains.

Other drivers and restraints analyzed in the detailed report include:

- Growing Silver-Economy Demand Driving Premium Health & Wellness Categories

- Government Push for "Smart Retail" and Digital-Yuan Pilots Boosting Omnichannel Investment

- Demographic Headwinds: Shrinking Working-Age Population

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Food & Beverages held 30.72% of China's retail market share in 2025. Consumer Electronics & Appliances is projected to grow at a 9.23% CAGR on subsidies for smart-home upgrades. The segment captures rising interest in energy-efficient refrigerators and AI voice-controlled devices. Personal & Household Care rides premium skincare and hygiene habits, while sports gear gains from outdoor lifestyles. Furniture and toys enjoy stay-at-home demand, and luxury pet care emerges as a niche. The China retail market size for electronics is forecast to widen as disposable income shifts from daily essentials to functional upgrades. Apparel and accessories lag amid cautious spending, yet online-only labels use live streams to offset footfall drops.

A quality-over-quantity mindset drives willingness to pay for durable appliances and health-centric foods. Electric-vehicle peripherals such as home chargers spur cross-category bundles. Retailers leverage AI promotions tailored to product-usage scenarios, lifting attachment rates. As the silver-economy scales, ergonomic appliances, and nutritional foods strengthen loyalty. Food safety regulation improves trust in premium grocery, further anchoring Food & Beverages at the core of the China retail market.

E-commerce claimed 34.15% of China retail market size in 2025 through frictionless payments and social-commerce integration. Membership-club stores grow 13.35% annually by curating imports, offering value packs and enhancing in-store tasting. Consumers accept annual fees for exclusive SKUs and superior cold-chain reliability. Supermarkets experiment with smaller, service-oriented setups. Convenience stores benefit from urban densification and instant-delivery apps that extend shelf space virtually. Department stores rationalize floor space toward experiential zones. Other channels like vending and community group-buy diversify reach in peri-urban districts.

The warehouse-club boom pushes omnichannel incumbents to open pick-up lockers and partner with clubs for joint promotions. Live-stream features inside club aisles create hybrid experiences. E-commerce pure-plays roll out offline showrooms to humanize engagement. Resulting channel convergence enriches consumer choice and fuels overall China retail market growth.

The China Retail Market Report is Segmented by Product Category (Food & Beverages, Personal & Household Care, and More), by Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, and More), by City Tier (Tier 1, Tier 2, Tier 3, Tier 4 & Below), by Store Format Size (Large-Format, Mid-Sized, and More), and by Geography (East China, North China, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Alibaba Group Holding Ltd.

- JD.com Inc.

- Sun Art Retail Group Ltd.

- Walmart Inc.

- Yonghui Superstores Co. Ltd.

- Suning Holdings Group

- GOME Retail Holdings Ltd.

- Costco Wholesale (China) Ltd.

- Hema Fresh (Freshippo)

- Carrefour China

- Metro China (Wumart)

- Vipshop Holdings Ltd.

- Pinduoduo Inc.

- Meituan Select

- Yonghui Yunchuang

- Tencent Smart Retail

- Dashang Group

- Better Life Retail

- Bubugao (BBG)

- Pagoda

- Lawson China

- Seven-Eleven China

- MINISO Group

- Dixintong (D.Phone)

- Xiaomi YouPin

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of social & live-stream commerce in lower-tier cities

- 4.2.2 Expansion of membership-based warehouse clubs lifting average basket size

- 4.2.3 Growing silver-economy demand driving premium health & wellness categories

- 4.2.4 Government push for 'Smart Retail' and digital-yuan pilots boosting omnichannel investment

- 4.2.5 Rising penetration of autonomous convenience stores & community group-buy models

- 4.2.6 Rebound in experiential retail (duty-free & themed malls) via tourism revival policies

- 4.3 Market Restraints

- 4.3.1 Intensifying price wars on e-commerce platforms eroding retailer margins

- 4.3.2 Demographic headwinds: shrinking working-age population

- 4.3.3 Regulatory crack-downs on data privacy & influencer marketing raising compliance cost

- 4.3.4 Rural-urban logistics gaps limiting cold-chain coverage for fresh grocery

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces Bargaining Power of Suppliers

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Threat of New Entrants

- 4.6.3 Threat of Substitutes

- 4.6.4 Intensity of Competitive Rivalry

- 4.7 Impact of COVID-19 on the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Category

- 5.1.1 Food & Beverages

- 5.1.1.1 Fresh Food

- 5.1.1.2 Packaged Food

- 5.1.1.3 Beverage - Alcoholic

- 5.1.1.4 Beverage - Non-Alcoholic

- 5.1.2 Personal & Household Care

- 5.1.2.1 Beauty & Personal Care

- 5.1.2.2 Home Care

- 5.1.3 Apparel, Footwear & Accessories

- 5.1.3.1 Apparel

- 5.1.3.2 Footwear

- 5.1.3.3 Accessories & Luxury Goods

- 5.1.4 Furniture, Toys & Hobby

- 5.1.4.1 Furniture & Home Decor

- 5.1.4.2 Toys & Baby Products

- 5.1.4.3 Sports & Leisure Equipment

- 5.1.5 Consumer Electronics & Appliances

- 5.1.5.1 Mobile & IT

- 5.1.5.2 Home Appliances

- 5.1.5.3 Other Electronics

- 5.1.6 Other Products

- 5.1.1 Food & Beverages

- 5.2 By Distribution Channel

- 5.2.1 Supermarkets & Hypermarkets

- 5.2.2 Convenience Stores

- 5.2.3 Department Stores

- 5.2.4 Specialty Stores

- 5.2.5 Discount & Membership Club Stores

- 5.2.6 E-commerce Online Marketplaces

- 5.2.7 Other Channels (Direct selling, vending, community group-buy)

- 5.3 By City Tier Tier 1 Cities

- 5.3.1 Tier 2 Cities

- 5.3.2 Tier 3 Cities

- 5.3.3 Tier 4 & Below

- 5.4 By Store Format Size

- 5.4.1 Large-Format

- 5.4.2 Mid-Sized

- 5.4.3 Small-Format

- 5.5 By Region (China)

- 5.5.1 East China

- 5.5.2 North China

- 5.5.3 Northeast China

- 5.5.4 South China

- 5.5.5 Central China

- 5.5.6 Southwest China

- 5.5.7 Northwest China

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Alibaba Group Holding Ltd.

- 6.4.2 JD.com Inc.

- 6.4.3 Sun Art Retail Group Ltd.

- 6.4.4 Walmart Inc.

- 6.4.5 Yonghui Superstores Co. Ltd.

- 6.4.6 Suning Holdings Group

- 6.4.7 GOME Retail Holdings Ltd.

- 6.4.8 Costco Wholesale (China) Ltd.

- 6.4.9 Hema Fresh (Freshippo)

- 6.4.10 Carrefour China

- 6.4.11 Metro China (Wumart)

- 6.4.12 Vipshop Holdings Ltd.

- 6.4.13 Pinduoduo Inc.

- 6.4.14 Meituan Select

- 6.4.15 Yonghui Yunchuang

- 6.4.16 Tencent Smart Retail

- 6.4.17 Dashang Group

- 6.4.18 Better Life Retail

- 6.4.19 Bubugao (BBG)

- 6.4.20 Pagoda

- 6.4.21 Lawson China

- 6.4.22 Seven-Eleven China

- 6.4.23 MINISO Group

- 6.4.24 Dixintong (D.Phone)

- 6.4.25 Xiaomi YouPin

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment