PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907265

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907265

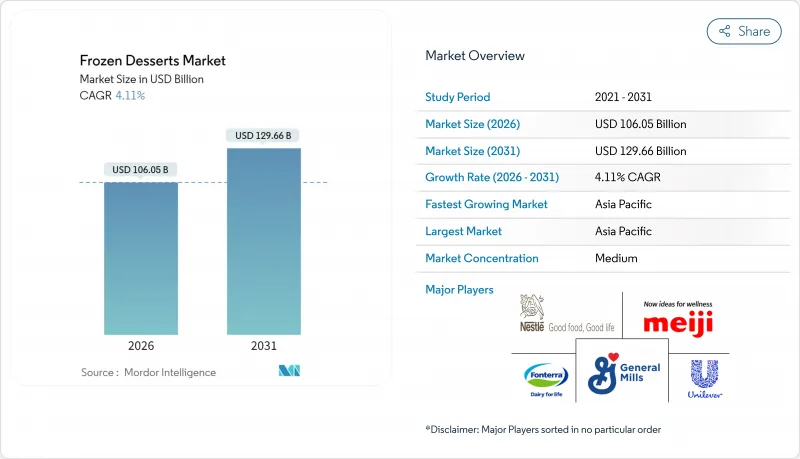

Frozen Desserts - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The frozen desserts market size in 2026 is estimated at USD 106.05 billion, growing from 2025 value of USD 101.86 billion with 2031 projections showing USD 129.66 billion, growing at 4.11% CAGR over 2026-2031.

This growth trajectory reflects the industry's resilience in the face of evolving consumer preferences and supply chain complexities. The market demonstrates remarkable adaptability as manufacturers pivot toward health-conscious formulations while maintaining indulgent appeal, creating a dual-track strategy that captures both wellness-focused and traditional consumer segments. Driven by a desire for healthier options, consumers are steering the frozen dessert market. They're gravitating towards treats that are low in sugar, high in protein, and often non-dairy or plant-based. At the same time, they're drawn to innovative, premium flavors and textures that tantalize the taste buds. Convenience remains a key factor, as ready-to-eat and single-serve options, along with broader availability across supermarkets, e-commerce platforms, and specialty stores, are making these products more accessible to consumers. Moreover, trends in sustainability and ethics, such as eco-friendly packaging, clean labels, and a push towards plant-based products, are playing a pivotal role in shaping both product development and consumer preferences.

Global Frozen Desserts Market Trends and Insights

Continuous Innovation in Unique Flavor Varieties

Flavor innovation drives market differentiation as manufacturers leverages global culinary trends to capture adventurous consumer palates. Unilever's 2025 product launches demonstrate this strategy with Talenti's bakery-inspired gelato layers and Good Humor's sustainable-farmed lime offerings. There's an increasing inclination of U.S consumers towards exotic fruit flavors like mango, guava, and dragon fruit, while younger generations drive demand for global street food-inspired varieties. Collaborative product development, exemplified by Baskin-Robbins' partnership with Trolli for sour-flavored ice cream, creates cross-category appeal and extends seasonal relevance beyond traditional summer peaks. This innovation cycle accelerates as manufacturers respond to social media-driven flavor discovery and cultural fusion trends. The strategic emphasis on limited-time offerings and co-branded flavors generates consumer urgency while testing market acceptance for permanent line extensions.

Rising Demand for Health-Conscious Options

Health-conscious positioning transforms product development as consumers seek indulgence without compromising wellness goals. Frozen yogurt outpaces traditional ice cream growth, while the organic segment is reflecting premiumization trends toward cleaner ingredients and functional benefits. Perfect Day's precision fermentation technology, integrated into Breyers' lactose-free chocolate ice cream, demonstrates how biotechnology addresses dietary restrictions while maintaining dairy-like sensory properties. Academic research on vegan ice cream formulations using fermented hazelnut cake reveals potential for upcycled ingredients that deliver enhanced protein digestibility and antioxidant activity post-digestion. Conagra's identification of GLP-1 medication users as a growing consumer segment drives the development of high-protein, low-calorie frozen desserts with "On Track" labeling for weight management support. This health-forward innovation creates premium pricing opportunities while expanding addressable market segments beyond traditional demographics.

Health Concerns Over Sugar and Additives

Consumer health consciousness creates formulation challenges as manufacturers balance taste expectations with nutritional demands. Regulatory pressure intensifies as FDA proposes revoking 23 food standards of identity, potentially affecting frozen dessert composition flexibility while maintaining consumer safety . The rise of GLP-1 medications among 15 million US adults drives demand for lower-calorie alternatives, forcing traditional manufacturers to reformulate core products or risk market share erosion to specialized health-focused brands. Sugar reduction initiatives face technical hurdles in maintaining texture and mouthfeel, particularly in ice cream where sugar contributes to freezing point depression and crystal formation. Alternative sweetener adoption requires extensive consumer education and regulatory compliance, while clean-label trends limit acceptable ingredient options. The challenge intensifies as younger consumers demonstrate higher health awareness yet maintain indulgence expectations, creating a narrow formulation window for successful product development.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Popularity of Ready-to-Eat Convenience

- Expansion of Online and Omnichannel Sales

- High Dependence on Cold-Chain Logistics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ice cream maintains its commanding 55.78% market share in 2025, yet frozen yogurt's accelerated 5.31% CAGR through 2031 signals shifting consumer preferences toward perceived healthier alternatives. The traditional ice cream segment benefits from established consumer habits and extensive distribution networks, while premium variants command higher margins through artisanal positioning and unique flavor innovations. Frozen yogurt capitalizes on health-conscious trends and probiotic marketing, with manufacturers like Conagra identifying gut-health products with pre/probiotic claims growing 33% over three years. Frozen cakes and pastries occupy specialized occasion-based consumption, primarily through foodservice channels and celebration markets.

The gelato subcategory within "Others" demonstrates premium positioning success through Italian authenticity and artisanal production methods, while sorbet and sherbet appeal to dairy-free consumers seeking fruit-forward options. Regulatory compliance under FDA standards requires ice cream to contain minimum 10% milkfat and 20% total milk solids, creating formulation constraints that frozen yogurt and alternative products can circumvent. Innovation opportunities emerge in hybrid products that combine ice cream indulgence with yogurt health positioning, while plant-based alternatives gain mainstream acceptance through improved taste and texture formulations.

Conventional products dominate with 82.08% market share in 2025, yet organic alternatives surge at 5.86% CAGR, reflecting consumer willingness to pay premium prices for perceived quality and environmental benefits. The organic segment benefits from clean-label positioning and sustainable sourcing narratives that resonate with environmentally conscious consumers, particularly in developed markets where disposable income supports premium pricing. Conventional products maintain cost advantages and broad accessibility, while facing pressure to adopt cleaner ingredient profiles and sustainable packaging initiatives. Ben & Jerry's commitment to eliminate petroleum-based plastic from 100% of packaging by 2025 illustrates how conventional brands integrate sustainability without organic certification.

Organic certification requires compliance with USDA National Organic Program standards, creating supply chain complexity and cost premiums that limit market penetration despite growth momentum. The category split reflects broader food industry trends toward transparency and traceability, with conventional manufacturers adopting organic-adjacent positioning through natural ingredients and sustainable practices. Cross-category innovation opportunities emerge as conventional brands test organic line extensions while organic specialists expand into mainstream distribution channels through strategic partnerships and private label arrangements.

The Frozen Dessert Market is Segmented by Product Type (Frozen Yogurt, Ice Cream, Frozen Cakes and Pastries, and Other Types), Category (Conventional and Organic), Packaging Format (Tubs/Pints, Bars/Sticks, and More), Distribution Channel (Foodservice/HoReCa and Retail), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific's 42.55% market share in 2025 and leading 5.63% CAGR through 2031 reflect the region's economic dynamism and evolving consumer preferences toward Western dessert categories. China's market complexity intensifies as local competitors like Mixue challenge established Western brands through aggressive pricing and cultural adaptation strategies, forcing international players to reconsider market entry approaches. Thailand emerges as a standout market where Dairy Queen achieved 23% same-store sales growth in 2023 through localized flavor development and strategic expansion, with potential to reach 1,000 stores as tropical climates support year-round consumption. India and Indonesia present significant growth opportunities through urbanization and rising disposable incomes, while Japan and Australia offer premium market positioning through quality-focused consumer segments. The region's growth trajectory benefits from infrastructure development and cold-chain logistics improvements that enable market penetration in previously inaccessible areas.

North America and Europe maintain substantial market positions through established consumption patterns and premium product innovation yet face market maturation challenges that constrain growth potential compared to emerging regions. The United States demonstrates market sophistication through health-conscious product development and omnichannel distribution strategies, with Conagra identifying approximately 15 million GLP-1 medication users as an emerging consumer segment driving demand for specialized frozen desserts. European markets emphasize artisanal positioning and sustainability initiatives, with Italian gelato operations generating EUR 3 billion (USD 3.2 billion) through 39,000 points of sale and demonstrating year-round consumption patterns . Regulatory frameworks in these developed markets drive innovation in clean-label formulations and sustainable packaging, creating competitive advantages for manufacturers that successfully navigate compliance requirements while maintaining consumer appeal.

South America, Middle East, and Africa represent emerging opportunities where economic development and infrastructure improvements support market expansion despite current smaller market shares. The Middle East demonstrates premium positioning success through Baskin-Robbins' GCC operations, where Galadari Ice Cream operates over 850 stores and maintains recognition as the largest global franchisee. These regions benefit from young demographics and increasing urbanization that drive adoption of Western dessert categories, while local flavor preferences and cultural considerations require product adaptation strategies. Infrastructure development in cold-chain logistics and retail modernization creates market access opportunities for international brands willing to invest in long-term market development and local partnership strategies.

- General Mills Inc.

- Fonterra Co-operative Group

- Meiji Holdings Co. Ltd

- Nestle S.A.

- Unilever

- Wells Enterprises

- Inner Mongolia Yili Industrial Group Co. Ltd

- Mars Inc.

- Amul (GCMMF)

- Blue Bell Creameries

- Lotte Confectionery

- Turkey Hill Dairy

- J&J Snack Foods Corp.

- Bulla Dairy Foods

- Yasso Inc.

- Dunkin' Brands

- Arun Ice Creams

- Mondelez International Inc.

- Baskin Robbins

- Hatsun Agro

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Continuous Innovation in Unique Flavor Varieties

- 4.2.2 Rising Demand for Health-Conscious Options

- 4.2.3 Increasing Popularity of Ready-to-Eat Convenience

- 4.2.4 Growth of Premium and Artisanal Desserts

- 4.2.5 Seasonal Campaigns Boosting Dessert Sales

- 4.2.6 Expansion of Online and Omnichannel Sales

- 4.3 Market Restraints

- 4.3.1 Health Concerns Over Sugar and Additives

- 4.3.2 High Dependence on Cold-Chain Logistics

- 4.3.3 Shift Toward Fresh and Alternative Desserts

- 4.3.4 Volatility in Raw Material Prices

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Ice Cream

- 5.1.2 Frozen Yogurt

- 5.1.3 Frozen Cakes and Pastries

- 5.1.4 Others

- 5.2 By Category

- 5.2.1 Conventional

- 5.2.2 Organic

- 5.3 By Packaging Format

- 5.3.1 Tubs/Pints

- 5.3.2 Bars/Sticks

- 5.3.3 Cones/Cups

- 5.3.4 Others

- 5.4 By Distribution Channel

- 5.4.1 Foodservice/HoReCa

- 5.4.2 Retail

- 5.4.2.1 Supermarkets/Hypermarkets

- 5.4.2.2 Convinience/Grocery Stores

- 5.4.2.3 Online Retail Stores

- 5.4.2.4 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 General Mills Inc.

- 6.4.2 Fonterra Co-operative Group

- 6.4.3 Meiji Holdings Co. Ltd

- 6.4.4 Nestle S.A.

- 6.4.5 Unilever

- 6.4.6 Wells Enterprises

- 6.4.7 Inner Mongolia Yili Industrial Group Co. Ltd

- 6.4.8 Mars Inc.

- 6.4.9 Amul (GCMMF)

- 6.4.10 Blue Bell Creameries

- 6.4.11 Lotte Confectionery

- 6.4.12 Turkey Hill Dairy

- 6.4.13 J&J Snack Foods Corp.

- 6.4.14 Bulla Dairy Foods

- 6.4.15 Yasso Inc.

- 6.4.16 Dunkin' Brands

- 6.4.17 Arun Ice Creams

- 6.4.18 Mondelez International Inc.

- 6.4.19 Baskin Robbins

- 6.4.20 Hatsun Agro

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK