PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910590

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910590

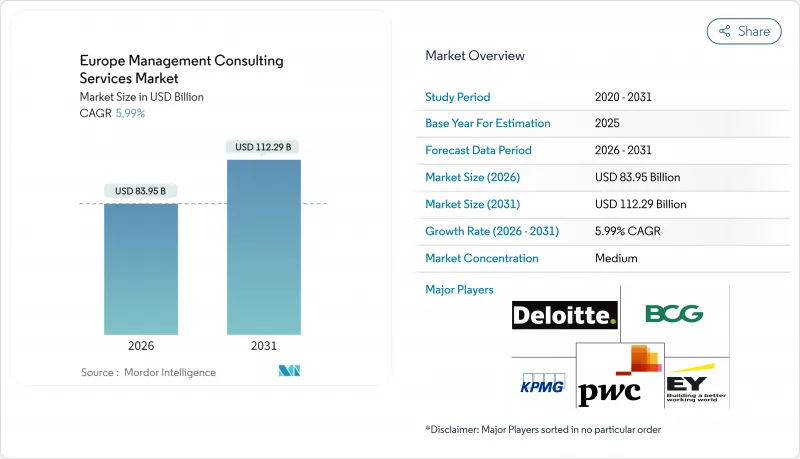

Europe Management Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Europe management consulting market size in 2026 is estimated at USD 83.95 billion, growing from 2025 value of USD 79.21 billion with 2031 projections showing USD 112.29 billion, growing at 5.99% CAGR over 2026-2031.

Surging digital-transformation investments, expanding ESG regulations, and accelerating AI adoption position consulting firms as indispensable partners for strategic realignment and operational efficiency. Operations excellence engagements dominate current spending, yet the rapid scale-up of generative-AI programs is shifting wallet share toward digital and analytics advisory. Regionally, DACH retains leadership on the back of Germany's strong industrial base, while Central and Eastern Europe (CEE) posts the quickest gains as EU funds flow toward modernization. Competitive intensity is rising as boutique specialists and freelance platforms pressure traditional fee structures, prompting the Big Four to double down on technology ecosystems and outcome-based pricing.

Europe Management Consulting Services Market Trends and Insights

Surge in Digital-Transformation Spending

European companies lifted digital-transformation outlays to USD 1.1 trillion in 2024, up 9% year on year, with software and IT services absorbing most of the budget . DACH businesses plan average generative-AI investments of USD 37 million during 2025, yet 71% concede progress is lagging due to talent gaps. Industrial icons such as Fresenius cut SAP administration time by 50% following cloud migration, proving hard ROI to boards. Nordic consultancies, now worth EUR 2.77 billion, attribute over one-third of revenue to digital projects. Manufacturing players like Evyap have shaved 23% scrap using IoT analytics, reinforcing demand for end-to-end technology advisory.

Escalating Demand for Advanced Analytics and AI Advisory

Generative-AI adoption moved from proof-of-concept to mission-critical, with 77% of European financial-services leaders expecting significant productivity lifts and 68% predicting job-role redesign within 12 months. Despite appetite, 35% lack concrete upskilling road-maps, opening advisory opportunities. UK consulting firms earmark GBP 1.9 million per firm for AI-capability build-outs through 2026. Partnership ecosystems are pivotal, illustrated by NTT Data's tie-up with Mistral AI to deliver sovereign enterprise AI for regulated sectors. The Big Four collectively plan more than USD 5 billion in AI platform investments by 2030, signaling long-run advisory capacity expansion.

Severe Talent Shortage and Attrition

Turnover in European consulting averages 13.25%, with junior attrition at the Big Four hitting 22%, fueled by long hours and burnout. The gap widens in cyber-security, where 76% of staff lack formal credentials, amplifying delivery risk. German firms are hiking salaries 2.5% on average for 2025 as part of retention pushes, with entry-level bumps of 3.5%. Persistent shortages limit project-ramp speed, compelling firms to prioritize margin-rich accounts and further squeeze growth in commoditized workstreams.

Other drivers and restraints analyzed in the detailed report include:

- ESG-linked Regulatory Complexity

- Cyber-security Compliance Mandates

- Fee-rate Pressure from Professional Procurement

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Operations Consulting captured 29.65% of the European management consulting market size in 2025 as companies aimed to streamline costs and future-proof supply networks amid volatile demand. Strategy Consulting, while foundational, now ranks behind digital engagements as boardrooms seek tangible quick wins from productivity projects. Digital/AI Consulting is scaling fastest, advancing at a 12.29% CAGR into 2031, fueled by AI roadmap design, data-platform integration, and cloud-migration mandates.

The Europe management consulting market increasingly values specialized sub-services such as sustainability advisory and risk compliance, which spike alongside new EU directives. Technology-centric mandates dominate procurement pipelines; banks like Credit Europe reduced onboarding time from two weeks to 15 minutes after micro-services re-platforming, illustrating payback from tech-led operational redesign . Risk and compliance work accelerates due to DORA and NIS2, while ESG advisory gains momentum under CSRD rules. Firms building cross-domain squads that blend sector expertise with analytics talent are winning multiyear retainer deals.

Financial Services commanded 33.05% of the Europe management consulting market share in 2025 on the back of regulatory complexity, fintech disruption, and multi-cloud modernization. Healthcare and Life Sciences posts the fastest 9.92% CAGR as providers digitize clinical pathways and pharma accelerates RandD analytics.

In banking, BBVA's fully digital acquisition engine delivered 11.1 million new customers and EUR 8.02 billion profit, underscoring advisory ROI. Manufacturing workloads emphasize Industry 4.0 retrofits, whereas public-sector projects focus on citizen-experience redesign. Energy, retail, and logistics segments increasingly seek decarbonization blueprints, bundling strategy with execution support. Integration of AI across verticals is broadening addressable spend for consultancies equipped with sectorized IP.

The European Management Consulting Market is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, Digital Consulting, and More), Client Industry (IT and Telecommunications, Manufacturing, and More), Firm Size (Large Enterprises, and SMEs), Delivery Model (On-Site Consulting, Hybrid, and Fully Remote Consulting), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Deloitte Touche Tohmatsu Limited

- PricewaterhouseCoopers International Limited

- Ernst and Young Global Limited

- KPMG International Limited

- McKinsey and Company, Inc.

- Boston Consulting Group, Inc.

- Bain and Company, Inc.

- Accenture plc

- Booz Allen Hamilton Holding Corporation

- Kearney, Inc.

- Capgemini SE

- BearingPoint Holding B.V.

- Roland Berger Holding GmbH

- Oliver Wyman Group

- Grant Thornton International Ltd

- BDO Global

- PA Consulting Group Limited

- CGI Inc. (CGI Business Consulting)

- Sopra Steria Group SA

- IBM Consulting (International Business Machines Corp.)

- Infosys Consulting (Infosys Ltd.)

- Atos Consulting (Atos SE)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in digital-transformation spending

- 4.2.2 Escalating demand for advanced analytics and AI advisory

- 4.2.3 ESG-linked regulatory complexity

- 4.2.4 Cyber-security compliance mandates

- 4.2.5 Subscription-based consulting uptake by mid-market firms

- 4.2.6 SME decarbonisation road-maps demand

- 4.3 Market Restraints

- 4.3.1 Severe talent shortage and attrition

- 4.3.2 Fee-rate pressure from professional procurement

- 4.3.3 AI-driven self-service strategy platforms

- 4.3.4 Rise of freelance consulting marketplaces

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Industry Ecosystem Analysis

- 4.9 Key Use Cases and Case Studies

- 4.10 Assessment of Macroeconomic Trends

- 4.11 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Consulting Service Line

- 5.1.1 Strategy Consulting

- 5.1.2 Operations Consulting

- 5.1.3 Technology / Digital Consulting

- 5.1.4 HR Consulting

- 5.1.5 Financial Advisory

- 5.1.6 Risk and Compliance Consulting

- 5.1.7 Sustainability and ESG Advisory

- 5.2 By Client Industry

- 5.2.1 IT and Telecommunications

- 5.2.2 Manufacturing

- 5.2.3 Energy and Resources

- 5.2.4 Public Sector

- 5.2.5 Retail and Consumer Goods

- 5.2.6 Healthcare and Life Sciences

- 5.2.7 Financial Services

- 5.2.8 Transportation and Logistics

- 5.3 By Firm Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By Delivery Model

- 5.4.1 On-site Consulting

- 5.4.2 Hybrid (On-site and Remote)

- 5.4.3 Fully Remote / Virtual Consulting

- 5.5 By Country

- 5.5.1 DACH (Germany, Austria, Switzerland)

- 5.5.2 UK and Ireland

- 5.5.3 France and Benelux (France, Belgium, Netherlands, Luxembourg)

- 5.5.4 Nordics (Sweden, Norway, Denmark, Finland)

- 5.5.5 Southern Europe (Spain, Italy, Portugal, Greece)

- 5.5.6 Central and Eastern Europe (Poland, Czech Republic, Hungary, etc.)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Deloitte Touche Tohmatsu Limited

- 6.4.2 PricewaterhouseCoopers International Limited

- 6.4.3 Ernst and Young Global Limited

- 6.4.4 KPMG International Limited

- 6.4.5 McKinsey and Company, Inc.

- 6.4.6 Boston Consulting Group, Inc.

- 6.4.7 Bain and Company, Inc.

- 6.4.8 Accenture plc

- 6.4.9 Booz Allen Hamilton Holding Corporation

- 6.4.10 Kearney, Inc.

- 6.4.11 Capgemini SE

- 6.4.12 BearingPoint Holding B.V.

- 6.4.13 Roland Berger Holding GmbH

- 6.4.14 Oliver Wyman Group

- 6.4.15 Grant Thornton International Ltd

- 6.4.16 BDO Global

- 6.4.17 PA Consulting Group Limited

- 6.4.18 CGI Inc. (CGI Business Consulting)

- 6.4.19 Sopra Steria Group SA

- 6.4.20 IBM Consulting (International Business Machines Corp.)

- 6.4.21 Infosys Consulting (Infosys Ltd.)

- 6.4.22 Atos Consulting (Atos SE)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment