PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910876

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910876

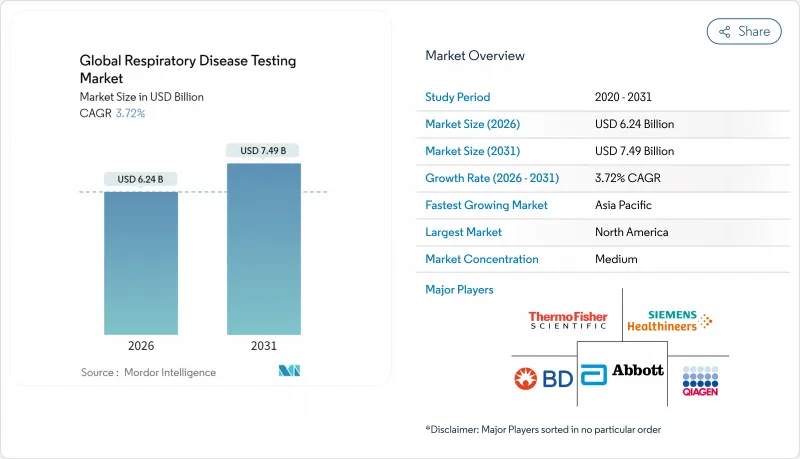

Global Respiratory Disease Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The respiratory disease testing market is expected to grow from USD 6.02 billion in 2025 to USD 6.24 billion in 2026 and is forecast to reach USD 7.49 billion by 2031 at 3.72% CAGR over 2026-2031.

The transition from pandemic-driven spikes to a steady expansion is anchored in chronic disease management programs, broader adoption of multiplex molecular diagnostics, and stronger digital integration across care settings. Post-COVID surveillance maintains elevated test volumes, while corporate wellness initiatives create fresh demand in occupational health environments. AI-enabled digital auscultation improves screening economics by reducing false positives and accelerating clinical decision-making, and growing home-care utilization fosters decentralized testing models that lower facility congestion. Major suppliers continue to invest in assay menu expansions and cloud-based workflow solutions that keep pace with evolving public health priorities. Consolidation, exemplified by Trudell Medical's acquisition of Vyaire's respiratory diagnostics business, signals an industry shift toward integrated respiratory solutions.

Global Respiratory Disease Testing Market Trends and Insights

Rising chronic respiratory disease burden

COPD affects more than 300 million people worldwide, prompting systematic screening programs that emphasize early detection to curb acute exacerbations and hospitalizations. Health systems recognize the cost savings generated by timely monitoring, which has driven routine spirometry and molecular testing adoption within primary care. AI-assisted COPD identification tools now improve diagnostic sensitivity in community clinics, helping clinicians stratify risk in aging populations and tailor intervention strategies. The demand for longitudinal respiratory data integrates seamlessly with population health platforms, positioning diagnostics as a preventive-care staple rather than an episodic measure.

Rapid uptake of home-based & POC diagnostic devices

Regulatory clearance of patient-operated spirometers, such as the FDA-approved NuvoAir device, enables reliable lung-function evaluation outside traditional clinics. Point-of-care PCR systems deliver bedside pathogen detection in under 40 minutes, streamlining triage and treatment at ambulatory sites. For underserved regions, portable instruments close access gaps and cut referral delays. Payers also benefit from lower emergency department utilization once respiratory conditions are managed closer to the patient. Home monitoring supports clinician oversight via telehealth dashboards, reinforcing adherence and triggering early interventions that mitigate severe flare-ups.

High capital cost of pulmonary diagnostic instruments

Purchasing advanced spirometry or plethysmography systems often exceeds USD 100,000, and annual service contracts add 15-20% to total ownership costs, deterring smaller providers. Facilities prolong equipment lifecycles beyond optimal performance, compromising accuracy and widening geographic disparities. Leasing models alleviate upfront spending but increase long-term outlays, compressing margins for budget-constrained clinics.

Other drivers and restraints analyzed in the detailed report include:

- Technological leaps in multiplex molecular diagnostics

- Post-COVID surveillance programs sustaining test volumes

- Complex reimbursement landscape for new tests

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Instruments captured 41.72% of the respiratory disease testing market in 2025 because hardware platforms remain essential for spirometry, PCR, and imaging workflows. Software & services are projected to grow at 4.05% CAGR through 2031, reflecting escalating demand for cloud analytics, AI interpretation, and remote device management. Assays & kits fuel recurring revenue as molecular panels widen, and consumables sustain baseline volume through replacement cycles. The respiratory disease testing market size for software & services is set to expand steadily as laboratories connect instruments to electronic medical records and population dashboards. Roche's navify platform illustrates how integrated informatics optimize throughput and support quality metrics.

Second, the respiratory disease testing market benefits from software that transforms diagnostic data into actionable insights. Cloud interfaces allow pulmonologists to view real-time spirometry results and receive automated alerts for declining lung function. Service contracts now bundle predictive maintenance, ensuring uptime and prolonging asset life. As telehealth normalization grows, secure APIs enable data flow from patient homes to clinical teams, underpinning remote care reimbursement models.

Molecular diagnostics delivered 46.85% respiratory disease testing market share in 2025 due to superior sensitivity and rapid turnaround. Syndromic multiplex panels should grow 4.82% CAGR through 2031 as clinicians favor single-swab identification of multiple pathogens. The respiratory disease testing market size for syndromic panels gains momentum as point-of-care adoption rises in urgent care and pediatric offices. Immunoassay/serology persists for surveillance, while imaging complements pathogen detection by visualizing lung sequelae. Pulmonary function tests hold strategic importance in chronic disease follow-up, and emerging breath-analysis technologies populate the "others" category, hinting at future competitive disruption.

Comprehensive panels reduce empirical antibiotic use and shorten isolation decisions. Laboratories leverage consolidated reagent inventories, lowering cost per target. Moreover, digital PCR lines extend detection limits for immunocompromised patients, expanding clinical utility. Industry innovators now explore cartridge-free formats that pair nanopore sequencing with AI analytics, tilting future competition toward sample-to-answer versatility.

The Respiratory Disease Testing Market Report is Segmented by Product Type (Instruments, Assays & Kits, and More), Test Type (Molecular Diagnostics, Immunoassay/Serology, and More), Disease Type (Asthma, COPD, Infectious Diseases, and More), End User (Hospitals & Clinics, Diagnostic Laboratories, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 41.67% of 2025 revenue, reflecting comprehensive insurance coverage, robust R&D ecosystems, and early adoption of AI-enhanced diagnostics. Federal procurement initiatives for influenza and RSV panels underpin baseline volumes, and employer-sponsored wellness programs expand occupational testing footprints. Academic-industry collaborations accelerate validation of novel assays, while CMS incentives favor hospitals that integrate rapid molecular diagnostics into antimicrobial stewardship protocols.

Europe exhibits steady expansion thanks to established universal healthcare and stringent quality standards. Germany drives demand for pulmonary function equipment in industrial safety programs, while the United Kingdom accelerates home-spirometry deployment through NHS digital pathways. France focuses on pediatric respiratory screening in urban pollution zones. GDPR imposes strict cloud-storage rules, compelling vendors to embed edge-processing capabilities that keep personal data local.

Asia-Pacific posts the fastest 5.18% CAGR, propelled by China's Healthy China 2030 targets and India's Ayushman Bharat digital health mission. Air-pollution-induced COPD prevalence intensifies screening volumes, and public-private partnerships finance mobile diagnostic vans in rural districts. Japan scales AI-auscultation in elder-care facilities to mitigate workforce shortages, while Australia adopts multiplex PCR panels to counter seasonal influenza surges. Government subsidies for indigenous manufacturing lower barriers for domestic suppliers, stimulating local production of molecular cartridges.

South America advances through Brazil's investments in respiratory surveillance after COVID-19. Colombia pilots home-care spirometry to decentralize congested urban hospitals. Argentina offers import duty relief on critical diagnostic reagents, nurturing adoption despite macroeconomic headwinds.

The Middle East & Africa leverage oil-financed healthcare infrastructure improvements. Saudi Arabia deploys cloud-connected point-of-care PCR across primary clinics, and the United Arab Emirates explores AI-driven lung sound analytics for expatriate worker screenings. South Africa integrates multiplex panels into tuberculosis programs, broadening differential diagnosis for co-infected patients.

- Roche

- Thermo Fisher Scientific

- Danaher

- Abbott Laboratories

- Beckton Dickinson

- Siemens Healthineers

- QIAGEN

- bioMerieux

- DiaSorin

- Hologic

- Illumina

- Revvity, Inc.

- Seegene

- Bio-Rad Laboratories

- Eurofins

- Oxford Nanopore Technologies plc

- Tecan Group

- Grifols

- Vyaire Medical

- GE HealthCare Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising chronic respiratory disease burden

- 4.2.2 Rapid uptake of home-based & POC diagnostic devices

- 4.2.3 Technological leaps in multiplex molecular diagnostics

- 4.2.4 Post-COVID surveillance programs sustaining test volumes

- 4.2.5 AI-enabled digital auscultation improving screening economics

- 4.2.6 Corporate wellness mandates expanding occupational lung testing

- 4.3 Market Restraints

- 4.3.1 High capital cost of pulmonary diagnostic instruments

- 4.3.2 Complex reimbursement landscape for new tests

- 4.3.3 Shortage of trained respiratory technologists

- 4.3.4 Data-privacy concerns over cloud-connected devices

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Threat of Substitutes

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Instruments

- 5.1.2 Assays & Kits

- 5.1.3 Consumables & Accessories

- 5.1.4 Software & Services

- 5.2 By Test Type

- 5.2.1 Molecular Diagnostics

- 5.2.2 Immunoassay / Serology

- 5.2.3 Imaging-based Tests

- 5.2.4 Pulmonary Function (Spirometry, Plethysmography)

- 5.2.5 Others

- 5.3 By Disease Type

- 5.3.1 Asthma

- 5.3.2 Chronic Obstructive Pulmonary Disease (COPD)

- 5.3.3 Infectious Diseases (Flu, RSV, COVID-19, TB)

- 5.3.4 Lung Cancer

- 5.3.5 Interstitial Lung Diseases

- 5.3.6 Others

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Diagnostic Laboratories

- 5.4.3 Physician Offices

- 5.4.4 Home-care Settings

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 F. Hoffmann-La Roche Ltd

- 6.3.2 Thermo Fisher Scientific Inc.

- 6.3.3 Danaher Corporation

- 6.3.4 Abbott Laboratories

- 6.3.5 Becton, Dickinson and Company

- 6.3.6 Siemens Healthineers AG

- 6.3.7 Qiagen N.V.

- 6.3.8 BioMerieux SA

- 6.3.9 DiaSorin S.p.A.

- 6.3.10 Hologic, Inc.

- 6.3.11 Illumina, Inc.

- 6.3.12 Revvity, Inc.

- 6.3.13 Seegene Inc.

- 6.3.14 Bio-Rad Laboratories Inc.

- 6.3.15 Eurofins Scientific SE

- 6.3.16 Oxford Nanopore Technologies plc

- 6.3.17 Tecan Group Ltd

- 6.3.18 Grifols, S.A.

- 6.3.19 Vyaire Medical, Inc.

- 6.3.20 GE HealthCare Technologies Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment