PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910927

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910927

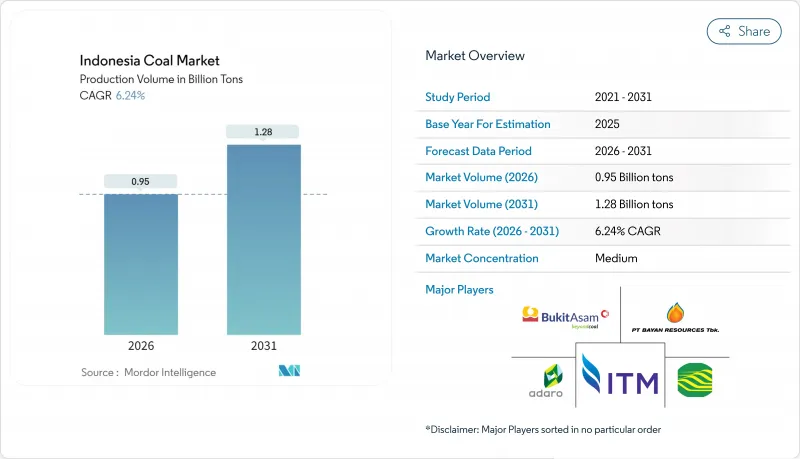

Indonesia Coal - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Indonesia Coal market is expected to grow from 0.89 Billion tons in 2025 to 0.95 Billion tons in 2026 and is forecast to reach 1.28 Billion tons by 2031 at 6.24% CAGR over 2026-2031.

The market's scale reflects Indonesia's position as the world's largest thermal-coal exporter and its entrenched role in the country's power mix. Ongoing PLN baseload demand, a nickel smelting boom, and a widening China-plus-One strategy collectively underpin demand growth, despite intensifying decarbonization rhetoric. Integrated miners continue to secure long-term offtake contracts that stabilize cash flows, while strategic reserve quality gives premium-grade producers additional pricing power. At the same time, regulatory reforms encouraging gasification and dimethyl-ether projects are opening new domestic outlets for low-rank coal. These parallel trends signal that the Indonesian coal market will remain resilient even as global capital costs for coal rise.

Indonesia Coal Market Trends and Insights

Prolonged PLN-led Baseload Demand for Low-CV Thermal Coal

PLN's limited headroom for rapid renewable build-out keeps coal in the core of Indonesia's power dispatch stack. Subsidized electricity tariffs require the utility to prioritize the lowest-cost generation fuel, and sub-bituminous coal remains the most cost-effective option delivered to Java-Bali load centers. Grid stability needs further reinforcement of dispatch preference because coal plants provide frequency and voltage services at a lower marginal cost than battery storage. Financially, PLN's budget allocation for coal procurement is predictable, reducing counterparties' credit risk and enabling miners to structure multi-year offtake agreements that lock in volumes. Consequently, the Indonesian coal market benefits from a structural demand floor that persists even as renewable penetration rises incrementally.

Surge in Coal-fired Captive Power for Nickel & EV-battery Smelters

Indonesia's 2020 nickel-ore export ban sparked capital inflows exceeding USD 15 billion into nickel processing complexes that require uninterrupted power for electric-furnace operations. Chinese-backed smelters routinely install on-site coal plants sized at 200-350 MW, providing a dedicated market immune to PLN's dispatch priorities. Captive arrangements typically involve dollar-linked power-purchase agreements, which grant miners higher realizations than utility deliveries. The business model thus secures premium margins while diversifying revenue streams. Demand expands further as downstream players move into precursor-cathode and battery materials, linking coal usage paradoxically to the low-carbon economy. These trends keep industrial offtake growth ahead of national average consumption through 2030.

Mandatory Domestic Market Obligation (DMO) Price Caps

Indonesia's DMO mechanism obliges miners to sell 25% of annual output at a government-set benchmark that trails export parity by up to USD 30 per ton during high-price cycles. This enforced discount compresses margin expansion opportunities and incentivizes firms to skew production toward higher-CV grades, which are earmarked exclusively for export. Financiers increasingly mark down reserve valuations that are exposed to DMO ceilings, complicating debt-raising for expansion. Although the policy shields PLN and industrial buyers from price spikes, it reduces investment appetite in new low-rank coal projects, thereby dampening incremental supply growth in the Indonesian coal market.

Other drivers and restraints analyzed in the detailed report include:

- China-plus-One Strategy Shifting Seaborne Demand to Indonesia

- Government "Gasification & DME" Incentives for Low-rank Coal

- Accelerated Coal-plant Retirement under JETP Funding

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sub-bituminous coal accounted for 46.85% of the Indonesian coal market in 2025, leveraging abundant East and South Kalimantan seams that deliver cost-competitive fuel to both domestic and export buyers. Despite this current dominance, bituminous and coking coal output is forecast to grow at an 7.86% CAGR between 2026 and 2031, lifting its share of the Indonesian coal market from 26.40% in 2025 to nearly one-third by 2031. Higher-CV grades unlock premiums of USD 15-20 per ton and align with emerging ultra-supercritical power-plant specifications in Asia. Metallurgical coal demand from regional blast furnaces further reinforces pricing power for producers with suitable reserve quality. Lignite remains oriented toward domestic gasification pilots and legacy low-efficiency boilers, implying flat growth. Production geography mirrors grade distribution; East Kalimantan operators, such as Kaltim Prima Coal, focus on premium grades, whereas Sumatra miners largely supply sub-bituminous coal to PLN. This quality segmentation enables portfolio balancing, as companies hedge against market swings by adjusting blend ratios between grades according to price differentials and logistics economics.

The Indonesia Coal Market Report is Segmented by Coal Grade (Lignite/Low-Rank, Sub-Bituminous, and Bituminous and Coking) and Application (Power Generation, Iron, Steel, and Metallurgy, and Cement and Other Applications). The Market Size and Forecasts are Provided in Terms of Production Volume (Tons).

List of Companies Covered in this Report:

- PT Bumi Resources Tbk

- PT Adaro Energy Indonesia Tbk

- PT Bayan Resources Tbk

- PT Bukit Asam Tbk

- PT Indo Tambangraya Megah Tbk

- PT Kaltim Prima Coal

- PT Arutmin Indonesia

- PT Kideco Jaya Agung

- PT Berau Coal Energy Tbk

- PT Indika Energy Tbk

- Golden Energy & Resources Ltd

- BlackGold Natural Resources

- PT Bhakti Energi Persada

- PT Bayan International

- PT Multi Harapan Utama

- Adani Indonesia (Adaro JV)

- Glencore (PT Balangan Coal)

- PT Petrosea Tbk

- PT Delta Dunia Makmur Tbk

- PT Resource Alam Indonesia Tbk

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Prolonged PLN-led baseload demand for low-CV thermal coal

- 4.2.2 Surge in coal-fired captive power for nickel & EV-battery smelters

- 4.2.3 China-plus-One strategy shifting seaborne demand to Indonesia

- 4.2.4 Government "Gasification & DME" incentives for low-rank coal

- 4.2.5 CCUS pilots unlocking high-CV export premiums

- 4.3 Market Restraints

- 4.3.1 Mandatory Domestic Market Obligation (DMO) price caps

- 4.3.2 Accelerated coal-plant retirement under JETP funding

- 4.3.3 Provincial moratoria on new mining permits (Kalimantan, Sumatra)

- 4.3.4 Rising ESG-driven trade financing costs for Indonesian coal

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Coal Grade

- 5.1.1 Lignite/Low-Rank

- 5.1.2 Sub-bituminous

- 5.1.3 Bituminous and Coking

- 5.2 By Application

- 5.2.1 Power Generation

- 5.2.2 Iron, Steel, and Metallurgy

- 5.2.3 Cement and Other Applications

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 PT Bumi Resources Tbk

- 6.4.2 PT Adaro Energy Indonesia Tbk

- 6.4.3 PT Bayan Resources Tbk

- 6.4.4 PT Bukit Asam Tbk

- 6.4.5 PT Indo Tambangraya Megah Tbk

- 6.4.6 PT Kaltim Prima Coal

- 6.4.7 PT Arutmin Indonesia

- 6.4.8 PT Kideco Jaya Agung

- 6.4.9 PT Berau Coal Energy Tbk

- 6.4.10 PT Indika Energy Tbk

- 6.4.11 Golden Energy & Resources Ltd

- 6.4.12 BlackGold Natural Resources

- 6.4.13 PT Bhakti Energi Persada

- 6.4.14 PT Bayan International

- 6.4.15 PT Multi Harapan Utama

- 6.4.16 Adani Indonesia (Adaro JV)

- 6.4.17 Glencore (PT Balangan Coal)

- 6.4.18 PT Petrosea Tbk

- 6.4.19 PT Delta Dunia Makmur Tbk

- 6.4.20 PT Resource Alam Indonesia Tbk

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment