PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911321

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911321

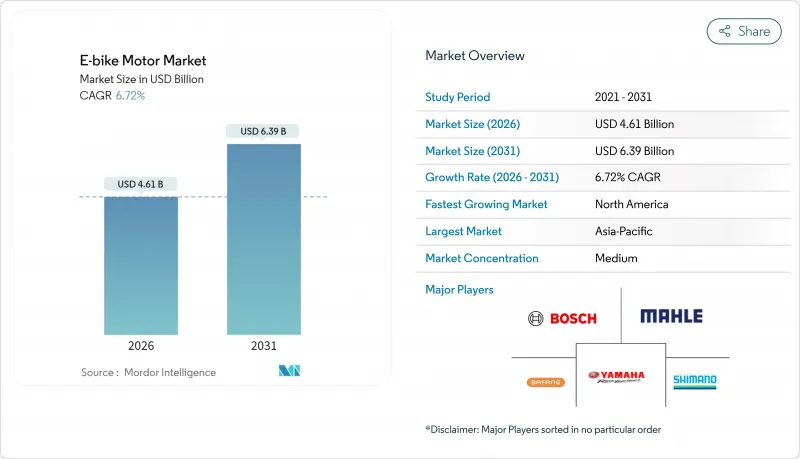

E-bike Motor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The e-bike motor market was valued at USD 4.32 billion in 2025 and estimated to grow from USD 4.61 billion in 2026 to reach USD 6.39 billion by 2031, at a CAGR of 6.72% during the forecast period (2026-2031).

Demand accelerates as cities tighten carbon-reduction mandates, logistics firms electrify fleets, and OEMs roll out software-defined drive units. The e-bike motor market benefits from falling battery prices, yet faces margin pressure from rare-earth magnet volatility that prompts suppliers to explore iron-nitride and ferrite alternatives. Intensifying consolidation-the Yamaha-Brose deal and Bosch's expanding smart-system portfolio-signals a shift toward vertically integrated offerings that blend hardware with over-the-air software. Asia-Pacific remains the primary production hub, but North America's appetite for high-power, throttle-enabled models drives fresh investment in local assembly lines.

Global E-bike Motor Market Trends and Insights

Soaring Urban-Commuter Uptake

Corporate bike-leasing programs fuel predictable, bulk demand that raises minimum quality thresholds for motor suppliers. Tax incentives lower end-user costs by up to 40%, channeling consumer preference toward premium drive units with onboard connectivity. As leasing spreads to France and the Nordics, the e-bike motor market secures an annuity-like volume stream anchored by fleet replacement cycles of three to four years. Motor makers leverage this stability to justify higher R&D outlays, especially for AI-based diagnostics that cut downtime. The growth of commuter e-bike lanes in major cities further reinforces baseline demand.

Stricter EU and China CO2 Targets

Revised European vehicle-emission rules and China's GB 17761-2024 standard press suppliers to maximize efficiency per kilogram, rather than peak wattage. Bosch's magnesium-housing Performance Line CX Gen 5 trims 100 g in weight yet maintains 85 Nm torque. China now mandates embedded battery-management systems, anti-tamper hardware, and satellite positioning, rewarding firms with advanced software stacks and penalizing low-end assemblers. These rulebooks also accelerate the industry's shift from lead-acid to lithium packs, cementing demand for compatible motor electronics. Compliance costs rise, but early movers gain a head start and access to high-regulation markets, reinforcing their brand equity in the e-bike motor market.

Dependence on NdFeB Magnets

China processes roughly 85% of global rare-earth output, leaving motor OEMs vulnerable to export restrictions and spot-price spikes. Setting up processing facilities beyond China's borders demands years of capital investment and environmental approvals, extending the period of vulnerability. This challenge is compounded by the complexities of navigating regulatory frameworks and securing sustainable supply chains. As the e-bike motor market grapples with margin risks linked to magnet supply fluctuations, it awaits the scaling of iron-nitride or ferrite alternatives, which could provide a more stable and cost-effective solution in the long term.

Other drivers and restraints analyzed in the detailed report include:

- OEM Push for Smart Integrated Systems

- Electrification of Delivery Fleets

- Speed-Cap Policy Divergence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hub motors retained a 67.58% e-bike motor market share in 2025, underpinned by low cost, plug-and-play installation, and widespread availability. Yet mid-drive units, projected to register an 8.36% CAGR, are reshaping premium categories through improved weight distribution and drivetrain synergy. Hub innovators answer back with features such as clutch-free coasting and sealed multi-speed gearboxes, prolonging their relevance in budget city bikes.

Shifts in component sourcing underscore the trajectory. Automotive-grade suppliers bring in IP-protected torque-sensor stacks and ASIC-based controllers that elevate mid-drive efficiency. Firmware updates enable user-selectable power maps, furthering personalization. While hub systems will dominate volume for entry-level and shared-mobility fleets, margin-rich mid-drive platforms will capture outsized profit pools, reinforcing the two-tier structure within the e-bike motor market.

Urban commuting bikes accounted for 42.86% of sales in 2025 and remain the anchor of the e-bike motor market size through mid-decade. City authorities add protected lanes and extend employer tax perks, magnifying baseline demand. At the same time, e-MTB shipments exhibit the fastest 8.02% CAGR as high-traction torque and adaptive suspension merge with 29-inch chassis standards. Motors designed for mountain bikes integrate barometric sensors to modulate power based on gradient, improving battery utilization. Fleet urban models emphasize weather sealing and predictive maintenance alerts that cut downtime for couriers.

The two segments differ on price elasticity; e-MTBs command ASPs approximately 1.7 times that of commuter units, justifying richer motor features. Urban platforms drive scale production, pushing down per-unit electronics cost, which then trickles into performance-oriented e-MTBs. This virtuous loop helps sustain volume growth across both segments, reinforcing the the overall robustness of the e-bike motor market.

The E-Bike Motor Market Report is Segmented by Motor Type (Hub Motor and Mid-Drive Motor), E-Bike Type (Urban/City, E-Mountain/EMTB, and E-Cargo), Power Rating (Below 250W, 250-500W, and Above 500W), Sales Channel (OEM/Factory-fit and Aftermarket/Retrofit), and Geography (North America, South America, Europe, Asia-Pacific, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated with 78.05% share in 2025 due to China's end-to-end supply chain that spans rare-earth mining to final assembly. Chinese electric two-wheeler exports exceeded CNY 40 billion (USD 5.5 billion) in 2024, underscoring regional capacity. Japan contributes premium drivetrain engineering, and India emerges as a fast-growing assembly node via joint ventures such as Musashi Seimitsu's partnership for integrated powertrains. Regional incentives-reduced VAT and urban congestion levies-bolster domestic ownership and export competitiveness, solidifying Asia-Pacific as the cornerstone of the e-bike motor market.

North America exhibits the fastest 9.14% CAGR through 2031 as consumer preferences tilt toward high-power, throttle-enabled models. Federal stimulus for domestic manufacturing and state-level rebates spur capacity additions like eBliss Global's New York plant. Regulatory heterogeneity across states creates niches for adaptable firmware and modular controller designs. Corporate fleet conversions and expanding trail access further diversify demand profiles, enhancing regional significance to the e-bike motor market.

Europe presents a mature but innovation-rich arena. Although unit sales tapered in 2024 amid macro headwinds, the continent remains technology-leading due to rigorous EN 15194 certification requirements. German leasing programs expand across the bloc, funneling steady orders for high-spec drive systems. Supply-chain localization efforts, notably battery-cell plants in Hungary and drive-unit factories in Poland, aim to offset Asian dependencies. As policymakers debate speed-cap harmonization, European OEMs refine motor efficiency within 250 W boundaries, reinforcing their premium brand cachet in the global e-bike motor market.

- Bafang Electric (Suzhou) Co., Ltd.

- Robert Bosch GmbH

- Shimano Inc.

- Yamaha Motor Co., Ltd.

- TDCM Corporation Limited

- Panasonic Holdings Corporation

- Nidec Corporation

- Mahle GmbH

- Suzhou Xiongda Electric Machine Co., Ltd.

- Jiangsu Dapu Motor Co., Ltd.

- TranzX

- Ananda Drive Techniques (Shanghai) Co., Ltd.

- Yadea Technology Group Co., Ltd.

- SportTech GmbH

- Valeo S.A.

- Polini Motori S.p.A.

- Fazua GmbH

- TQ-Systems GmbH

- Wuxi Truckrun Motor Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soaring Urban-Commuter Adoption of E-Bikes

- 4.2.2 Stricter EU and China CO2 Targets Favoring Lightweight Electric Propulsion

- 4.2.3 Rapid Transition of Pizza/Parcel Delivery Fleets To E-Bikes

- 4.2.4 OEM Demand for Integrated Smart-Motor and Sensor Packages

- 4.2.5 Venture Funding into Mid-Drive Start-Ups for Cargo and MTB Niches

- 4.2.6 Magnet-Material Breakthroughs Cut Rare-Earth Use by 40%

- 4.3 Market Restraints

- 4.3.1 High Upfront Motor/Battery Pairing Cost

- 4.3.2 Supply-Chain Vulnerability for NdFeB Magnets

- 4.3.3 Fire-Safety Recalls Triggering Insurance Premium Hikes

- 4.3.4 National E-Bike Speed-Cap Policy Divergence Delaying Platform Launches

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Motor Type

- 5.1.1 Hub Motor

- 5.1.2 Mid-drive Motor

- 5.2 By E-Bike Type

- 5.2.1 Urban / City

- 5.2.2 E-Mountain / EMTB

- 5.2.3 E-Cargo

- 5.3 By Power Rating

- 5.3.1 Below 250 W

- 5.3.2 250 - 500 W

- 5.3.3 Above 500 W

- 5.4 By Sales Channel

- 5.4.1 OEM / Factory-fit

- 5.4.2 Aftermarket / Retrofit

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Netherlands

- 5.5.3.7 Russia

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle-East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle-East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Bafang Electric (Suzhou) Co., Ltd.

- 6.4.2 Robert Bosch GmbH

- 6.4.3 Shimano Inc.

- 6.4.4 Yamaha Motor Co., Ltd.

- 6.4.5 TDCM Corporation Limited

- 6.4.6 Panasonic Holdings Corporation

- 6.4.7 Nidec Corporation

- 6.4.8 Mahle GmbH

- 6.4.9 Suzhou Xiongda Electric Machine Co., Ltd.

- 6.4.10 Jiangsu Dapu Motor Co., Ltd.

- 6.4.11 TranzX

- 6.4.12 Ananda Drive Techniques (Shanghai) Co., Ltd.

- 6.4.13 Yadea Technology Group Co., Ltd.

- 6.4.14 SportTech GmbH

- 6.4.15 Valeo S.A.

- 6.4.16 Polini Motori S.p.A.

- 6.4.17 Fazua GmbH

- 6.4.18 TQ-Systems GmbH

- 6.4.19 Wuxi Truckrun Motor Co., Ltd.

7 Market Opportunities & Future Outlook