PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911734

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911734

PC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

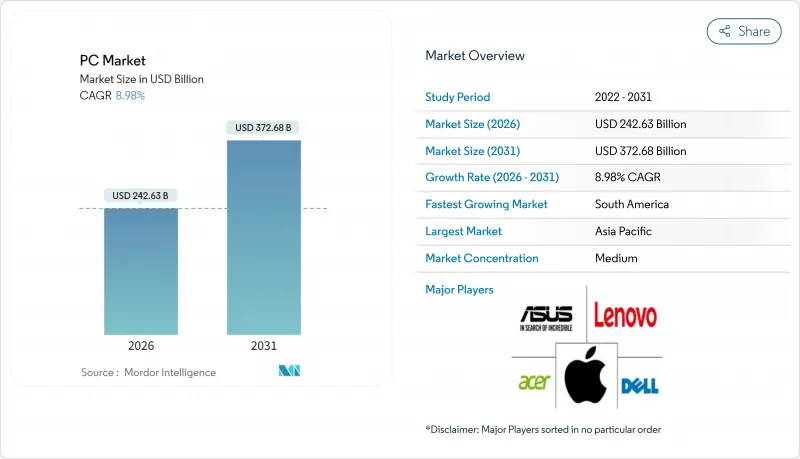

The PC Market was valued at USD 222.64 billion in 2025 and estimated to grow from USD 242.63 billion in 2026 to reach USD 372.68 billion by 2031, at a CAGR of 8.98% during the forecast period (2026-2031).

This revival follows the post-pandemic slump and rests on three pillars: enterprise-grade AI integration, the Windows 10 end-of-life deadline that forces device modernization, and a lasting shift toward hybrid work. Replacement decisions now hinge on performance specifications such as local AI acceleration, battery life, and thermals rather than on baseline functionality. Vendors react by refreshing portfolios with neural-processing-unit (NPU)-equipped notebooks, slimmer thermal designs, and greener materials to satisfy regulatory demands.

Key growth signals are already visible in the global PC market. Asia-Pacific, holding 37.00% 2024 share, anchors both supply and demand even as chip shortages and geopolitics disrupt logistics. Notebooks account for 78.20% of shipments, yet the fastest surge comes from AI-optimized laptops that rise at 11.8% CAGR. Commercial buyers generate 54.30% of demand, but gaming and esports devices post a stronger 10.9% CAGR because competitive play and streaming monetize hardware performance. Processor competition intensifies as ARM attempts 50% penetration by 2029, challenging x86's 94.60% 2024 dominance. Premium gaming systems above USD 1,200 grow 13.4% annually, while offline retail still controls 67.80% of sales in spite of a 14.44% CAGR for e-commerce channels.

Global PC Market Trends and Insights

Hybrid-work notebook refresh demand

Permanent hybrid work has shifted enterprise purchasing toward performance-optimized notebooks that sustain video-intensive meetings and cloud collaboration across variable networks. Microsoft reports that 30% of meetings already span multiple time zones, pushing firms to supply high-spec devices that enhance employee experience and retention. Battery endurance, integrated webcams, and thermal stability now influence refresh timing as much as warranty expiries. This driver favours premium notebooks where every watt-hour and cooling fin matter to remote productivity.

Gaming & esports performance race

Professional tournaments spotlight hardware as keenly as player skilll, highlighting trends in the PC market, turning frame-rate leadership into marketing currency. Typical pro setups pair Intel Core i7 or AMD Ryzen 7 CPUs with NVIDIA RTX 3070 GPUs, norms that cascade to mainstream buyers. Streaming revenue ties directly to visual fidelity, so creators invest in GPUs that support real-time ray tracing and AI-assisted upscaling. This arms race sustains a high-margin upgrade cycle and pushes component makers to accelerate launches.

Component supply-chain volatility

Hurricane Helene's disruption of Spruce Pine quartz mining exposed a single-point-of-failure for semiconductor crucibles. Although capacity normalizes by early 2025, fabs below 11 nm still struggle with tool lead times and labour shortages. OEMs hedge by pre-paying inventories and dual sourcing, yet elevated buffer stocks tie up working capital and cap promotional flexibility.

Other drivers and restraints analyzed in the detailed report include:

- Government digital-education rollouts

- On-device AI acceleration upgrade wave

- Smart-phone substitution for casual tasks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Notebooks delivered 77.45% of 2025 shipments, anchoring the PC market. AI-optimized laptops alone rise 11.65% CAGR, enabling mobile knowledge workers to run inference offline without draining batteries. Desktops retain roles in engineering labs and esports arenas where PCIe slots and superior thermals outshine portability. All-in-one systems carve a niche in front-office and classroom settings, while tablets and detachable bridge mobile and desktop workflows for field inspectors and creative professionals. Intel's recommended two- to four-year PC lifecycle illustrates how standardized fleets lower support burdens and warranty risk, further cementing notebooks as default corporate endpoints.

Second-order shifts emerge as thermal budgets tighten under sustained AI loads; vapor-chamber cooling, stacked-graphite heat spreaders, and low-power LPDDR5X memory become standard. Vendors also experiment with replaceable keyboard decks to ease recycling and limit e-waste, aligning with circular-economy mandates.

Commercial buyers supplied 53.85% of 2025 demand, underscoring the PC market's reliance on enterprise modernization. Hybrid work policies and cybersecurity controls elevate hardware budgets, steering firms toward BIOS-locked drives and built-in privacy shutters. Gaming and esports devices, though smaller, post 10.74% CAGR as streamers justify 240 Hz displays and AI-driven noise suppression that directly translate into audience engagement. Government and education buyers navigate funding cliffs by leveraging nationwide framework contracts, while SMBs adopt enterprise-grade warranties to minimize downtime. Consumer replacement cycles stretch unless tied to gaming or home-office performance gaps.

The PC Market Report Segmented by Form Factor (Laptops/Notebooks, Desktop Towers & SFF, All-In-One PCs and More), End User (Consumer, Small & Medium Business and More), Processor Architecture (x86, ARM-Based, RISC-V and More), Price Band, Distribution Channel (Offline Retail & VARs, E-Commerce & Direct-To-Consumer), Operating System and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region commanded 36.70% of 2025 PC market revenue, driven by high-density manufacturing clusters, a growing middle class, and aggressive government digitization plans. China and India anchor demand; Indian AI-PC volumes are expected to grow eight- to ten-fold in 2025 as refresh cycles align with enterprise generative AI rollouts. Discounted electricity and local assembly incentives maintain the region's cost advantage, although geopolitical tensions and currency fluctuations introduce volatility.

North America benefits from Windows 10 EOL upgrades and cybersecurity mandates, driving refresh demand in the PC market. Enterprises deploy NPUs to reduce cloud fees and enhance data sovereignty, thereby increasing average selling prices. U.S. federal strategic sourcing sets common specs-TPM 2.0, Wi-Fi 6E-that ripple through private-sector bids.

Europe grapples with stringent circular-economy laws. Digital product passports, repair-score labeling, and a destruction ban on unsold stock raise design complexity yet unlock premiums for sustainable models. OEMs that certify carbon-neutral factories win public-sector tenders, underscoring how regulation shapes competitive outcome.

South America emerges as the fastest-growing region at 8.58% CAGR. Brazil draws OEM investment such as Asus's local production of ExpertBook lines, blunting import tariffs and shortening delivery timelines. Gaming cafes and fintech startups fuel demand for performance notebooks. Currency volatility tempers consumer upgrades, but enterprise and government modernization pipelines stay resilient.

The Middle East and Africa record steady enterprise rollouts as oil economies diversify, and national "Vision 2030" programs digitize public services. Education ministries bulk-purchase Chromebooks and Windows laptops to lift digital literacy. Infrastructure gaps persist, yet mobile broadband and solar-powered classrooms expand addressable markets.

- Lenovo Group Limited

- HP Inc.

- Dell Technologies Inc.

- Apple Inc.

- ASUSTeK Computer Inc.

- Acer Incorporated

- Microsoft Corporation

- Samsung Electronics Co., Ltd.

- Micro-Star International Co., Ltd.

- Huawei Technologies Co., Ltd.

- Xiaomi Corporation

- LG Electronics Inc.

- Giga-Byte Technology Co., Ltd.

- Fujitsu Limited

- Panasonic Holdings Corporation

- Toshiba Electronic Devices & Storage Corporation

- CHUWI Innovation Technology Co., Ltd.

- Framework Computer Inc.

- NEC Corporation

- Purism SPC

- System76, Inc.

- Origin PC Corp.

- Valve Corporation

- Eluktronics, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hybrid-work notebook refresh demand

- 4.2.2 Gaming & E-sports performance race

- 4.2.3 Government digital-education rollouts

- 4.2.4 On-device AI acceleration upgrade wave

- 4.2.5 Windows 10 EOL 2025 mandated refresh

- 4.2.6 Enterprise green-PC procurement incentives

- 4.3 Market Restraints

- 4.3.1 Component supply-chain volatility

- 4.3.2 Smart-phone substitution for casual tasks

- 4.3.3 Cloud VDI lengthening refresh cycles

- 4.3.4 Circular-economy regulations & refurbishment

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Consumers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Form Factor

- 5.1.1 Laptops / Notebooks

- 5.1.2 Desktop Towers and SFF

- 5.1.3 All-in-One PCs

- 5.1.4 Tablets / Detachables

- 5.2 By End User

- 5.2.1 Consumer

- 5.2.2 Small and Medium Business

- 5.2.3 Large Enterprise

- 5.2.4 Government and Education

- 5.3 By Processor Architecture

- 5.3.1 x86 (Intel-AMD)

- 5.3.2 ARM-based

- 5.3.3 RISC-V and Other Processor Architectures

- 5.4 By Price Band

- 5.4.1 Entry-Level (<USD 600)

- 5.4.2 Mid-Range (USD 600-1200)

- 5.4.3 Premium / Gaming (> USD 1200)

- 5.5 By Distribution Channel

- 5.5.1 Offline Retail and VARs

- 5.5.2 E-commerce and Direct-to-Consumer

- 5.6 By Operating System

- 5.6.1 Windows

- 5.6.2 macOS

- 5.6.3 ChromeOS

- 5.6.4 Linux Distros

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Italy

- 5.7.3.2 France

- 5.7.3.3 Germany

- 5.7.3.4 United Kingdom

- 5.7.3.5 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 India

- 5.7.4.2 China

- 5.7.4.3 Japan

- 5.7.4.4 Rest of Asia-Pacifc

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 South Africa

- 5.7.5.3 United Arab Emirates

- 5.7.5.4 Rest of Middle East and Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Lenovo Group Limited

- 6.4.2 HP Inc.

- 6.4.3 Dell Technologies Inc.

- 6.4.4 Apple Inc.

- 6.4.5 ASUSTeK Computer Inc.

- 6.4.6 Acer Incorporated

- 6.4.7 Microsoft Corporation

- 6.4.8 Samsung Electronics Co., Ltd.

- 6.4.9 Micro-Star International Co., Ltd.

- 6.4.10 Huawei Technologies Co., Ltd.

- 6.4.11 Xiaomi Corporation

- 6.4.12 LG Electronics Inc.

- 6.4.13 Giga-Byte Technology Co., Ltd.

- 6.4.14 Fujitsu Limited

- 6.4.15 Panasonic Holdings Corporation

- 6.4.16 Toshiba Electronic Devices & Storage Corporation

- 6.4.17 CHUWI Innovation Technology Co., Ltd.

- 6.4.18 Framework Computer Inc.

- 6.4.19 NEC Corporation

- 6.4.20 Purism SPC

- 6.4.21 System76, Inc.

- 6.4.22 Origin PC Corp.

- 6.4.23 Valve Corporation

- 6.4.24 Eluktronics, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis