PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911807

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911807

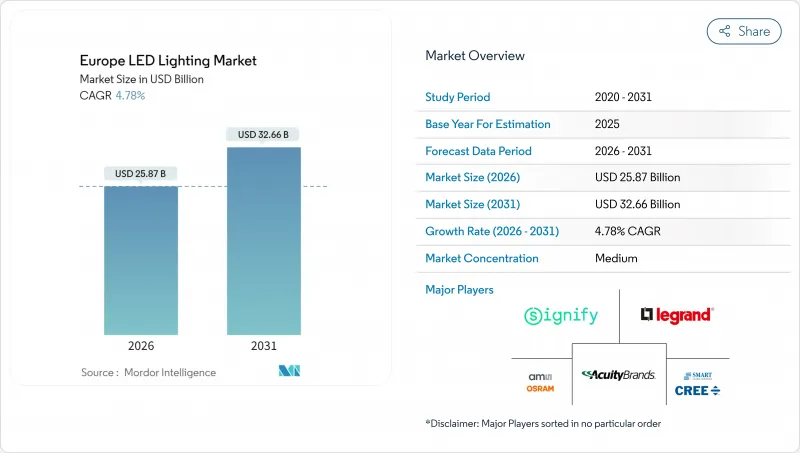

Europe LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The European LED lighting market was valued at USD 24.69 billion in 2025 and estimated to grow from USD 25.87 billion in 2026 to reach USD 32.66 billion by 2031, at a CAGR of 4.78% during the forecast period (2026-2031).

Growth reflects a mature, replacement-led cycle in which regulatory compliance and sustainability targets take precedence over the novelty of pure technology. EU-wide energy-efficiency mandates, phase-outs of halogen and fluorescent light bulbs, and corporate net-zero roadmaps keep retrofit momentum high, while falling costs per lumen and smart-city tenders expand new-installation opportunities. Incumbent suppliers capitalize on installation services, connected-lighting platforms, and circular-economy designs to defend share, though e-commerce channels lower barriers for niche entrants. Supply-chain risks surrounding rare-earth phosphors and the administrative burden of eco-design and WEEE obligations temper the near-term upside but also deter potential new competitors, keeping margins stable for scale players.

Europe LED Lighting Market Trends and Insights

Stringent EU Energy-Efficiency Regulations

The Ecodesign for Sustainable Products Regulation (ESPR), which took legal effect in July 2024, reshapes procurement by rewarding products with low energy use, long service life, and high repairability -attributes inherent to LED technology. Digital Product Passports, set for 2027, require manufacturers to document their environmental footprints, thereby increasing the compliance burden for legacy luminaires and strengthening supplier preference for established LED brands that already publish lifecycle data. The regulation also bans the destruction of unsold goods after 2026, compelling distributors to refine their inventory management and accelerate the clearance of non-compliant stock. Public-sector funding funnels into compliant lighting via instruments such as Italy's National Recovery and Resilience Plan, which allocated EUR 55.52 billion (USD 62.74 billion) for energy transition projects.

Rapid Phase-Out of Halogen and Fluorescent Lamps

EU and UK restrictions eliminate legacy lamps from circulation, obliging facilities to adopt LEDs regardless of budget cycles. Nordic countries enforce the shortest sunset dates and have triggered regional spikes in purchase orders that favor suppliers with well-stocked warehouses. Because integrated LED luminaires often replace entire housings, unit revenues rise even as unit counts remain stable, thereby lifting average selling prices. Manufacturers equipped with turnkey installation services capitalize on the urgency of compliance to bundle maintenance contracts, thereby deepening account lock-in.

Price-Sensitive Retrofit Payback Period in SMEs

Small enterprises defer upgrades when energy savings do not repay capital outlays within two years, thereby slowing retrofit volumes, even in the face of looming regulatory deadlines. Performance-contracting models, such as Denmark's Lumega scheme, remove upfront costs but impose qualification hurdles that discourage applicants, leaving a sizable portion of the installed base reliant on outdated lighting.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Net-Zero Commitments Driving Retrofits

- Falling LED Cost per Lumen

- Supply-Chain Volatilities for Rare-Earth Phosphors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The luminaires category secured 62.10 of % European LED lighting market share in 2025 through demand for fully engineered fixtures that merge light engines, optics, and controls. Segment revenues benefit from higher average selling prices and project-based installation services. Lamps, although smaller in absolute terms, are forecast to grow at a 7.45% CAGR to 2031 as costs decline and smart bulb features unlock retrofit spending. Track lighting and emergency luminaires are adopted in commercial offices where insurance regulations mandate compliant fittings. Circular-economy designs, such as LEDVANCE's EVERLOOP series, highlight how replaceable modules extend life cycles and satisfy ESPR repairability requirements.

In volume terms, lamp shipments rise faster because replacement work requires no rewiring, fitting SME cash-flow constraints. However, luminaire projects often integrate with building management systems, yielding data streams that facility managers monetize through occupancy analytics. This services layer supports premium pricing, reducing the risk of margin compression in an otherwise commoditized hardware landscape.

The wholesale and retail network maintained a 51.70% market share of the European LED lighting market in 2025, driven by electrical contractors who prefer bundled logistics and pre-sale design assistance. Yet e-commerce is expanding at a 5.75% CAGR, serving SMEs that value transparent pricing and rapid delivery. Manufacturers now deploy hybrid models; for instance, IKEA pairs online ordering of its JETSTROM smart panels with in-store support for configuration. Direct sales remain essential for large projects requiring site audits and bespoke photometric design.

Price transparency on digital platforms compresses distributor spreads while also providing suppliers with real-time demand data, thereby improving forecasting accuracy. Distributors respond by layering value-added services, such as on-site commissioning and warranty management, to protect their relevance.

The Europe LED Lighting Market Report is Segmented by Product Type (Lamps, and Luminaires/Fixtures), Distribution Channel (Direct Sales, Wholesale/Retail, and More), Installation Type (New Installation, and Retrofit Installation), Application (Commercial Offices, Retail Stores, and More), End User (Indoor, Outdoor, and More), and Country (United Kingdom, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Signify N.V.

- Zumtobel Group AG

- Osram Licht AG (ams-Osram)

- Schreder SA

- Fagerhult Group

- Acuity Brands Lighting Inc.

- Havells Sylvania Europe Ltd.

- Legrand S.A.

- Eaton Corporation plc (Cooper Lighting)

- TRILUX GmbH and Co. KG

- Thorn Lighting Ltd.

- FW Thorpe Plc

- LEDVANCE GmbH

- Helvar Oy Ab

- iGuzzini illuminazione S.p.A.

- Glamox AS

- Cree Lighting Europe S.p.A.

- ITECH LED Lighting

- Hella GmbH and Co. KGaA

- Nichia Europe GmbH

- Samsung Electronics Europe (LED business)

- LG Innotek Europe GmbH

- Valmont Industries (EU lighting poles)

- Opple Lighting Europe B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent EU energy-efficiency regulations

- 4.2.2 Rapid phase-out of halogen and fluorescent lamps

- 4.2.3 Corporate net-zero commitments driving retrofits

- 4.2.4 Falling LED cost per lumen

- 4.2.5 On-site renewable + DC micro-grids adoption

- 4.2.6 Smart-city tenders bundling IoT sensors

- 4.3 Market Restraints

- 4.3.1 Price-sensitive retrofit payback period in SMEs

- 4.3.2 Supply-chain volatilities for rare-earth phosphors

- 4.3.3 Complexity of EU eco-design / WEEE compliance

- 4.3.4 Lack of skilled installers for connected lighting systems

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Lamps

- 5.1.2 Luminaires / Fixtures

- 5.2 By Distribution Channel

- 5.2.1 Direct Sales

- 5.2.2 Wholesale / Retail

- 5.2.3 E-commerce

- 5.3 By Installation Type

- 5.3.1 New Installation

- 5.3.2 Retrofit Installation

- 5.4 By Application

- 5.4.1 Commercial Offices

- 5.4.2 Retail Stores

- 5.4.3 Hospitality

- 5.4.4 Industrial

- 5.4.5 Highway and Roadway

- 5.4.6 Architectural

- 5.4.7 Public Places

- 5.4.8 Hospitals

- 5.4.9 Horticulture Gardens

- 5.4.10 Residential

- 5.4.11 Automotive

- 5.4.12 Others (Chemicals, Oil and Gas, Agriculture)

- 5.5 By End User

- 5.5.1 Indoor

- 5.5.2 Outdoor

- 5.5.3 Automotive

- 5.6 By Country

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Netherlands

- 5.6.7 Sweden

- 5.6.8 Poland

- 5.6.9 Russia

- 5.6.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Signify N.V.

- 6.4.2 Zumtobel Group AG

- 6.4.3 Osram Licht AG (ams-Osram)

- 6.4.4 Schreder SA

- 6.4.5 Fagerhult Group

- 6.4.6 Acuity Brands Lighting Inc.

- 6.4.7 Havells Sylvania Europe Ltd.

- 6.4.8 Legrand S.A.

- 6.4.9 Eaton Corporation plc (Cooper Lighting)

- 6.4.10 TRILUX GmbH and Co. KG

- 6.4.11 Thorn Lighting Ltd.

- 6.4.12 FW Thorpe Plc

- 6.4.13 LEDVANCE GmbH

- 6.4.14 Helvar Oy Ab

- 6.4.15 iGuzzini illuminazione S.p.A.

- 6.4.16 Glamox AS

- 6.4.17 Cree Lighting Europe S.p.A.

- 6.4.18 ITECH LED Lighting

- 6.4.19 Hella GmbH and Co. KGaA

- 6.4.20 Nichia Europe GmbH

- 6.4.21 Samsung Electronics Europe (LED business)

- 6.4.22 LG Innotek Europe GmbH

- 6.4.23 Valmont Industries (EU lighting poles)

- 6.4.24 Opple Lighting Europe B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment