PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934692

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934692

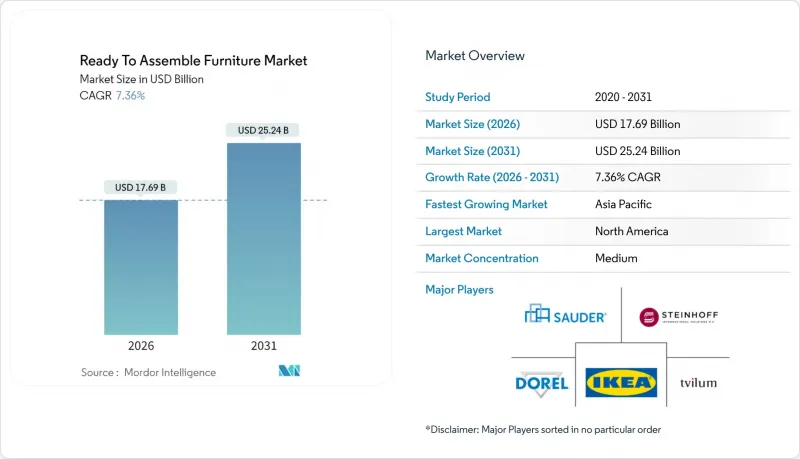

Ready To Assemble Furniture - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Ready To Assemble Furniture market is expected to grow from USD 16.48 billion in 2025 to USD 17.69 billion in 2026 and is forecast to reach USD 25.24 billion by 2031 at 7.36% CAGR over 2026-2031.

The expansion reflects rising demand for cost-efficient, space-saving furnishings, deeper e-commerce reach, and the logistics savings that flat-pack models deliver. Millennials and Gen Z continue to favor do-it-yourself assembly, while urbanization keeps average home footprints small, sustaining interest in compact modular pieces. Digital visualization tools now convert browsers to buyers at higher rates, helping retailers move inventory without large showrooms. Supply-chain investments in automated packaging and nearshored production further strengthen price competitiveness and delivery speed, reinforcing the growth outlook for the Ready to Assemble Furniture market.

Global Ready To Assemble Furniture Market Trends and Insights

Growing E-commerce Penetration for Furniture

E-commerce penetration in furniture retail has reached a tipping point where digital-first strategies are reshaping traditional showroom models and driving RTA adoption through enhanced visualization capabilities. Online furniture conversion rates have increased up to 200% for retailers implementing 3D and AR technologies, with 84% of consumers expressing preference for brands offering product visualization tools. This digital transformation particularly benefits RTA manufacturers as flat-pack products photograph and render more effectively than bulky assembled pieces, enabling superior online presentation. The shift is most pronounced in North America and Europe where established logistics infrastructure supports last-mile delivery of compact packages, while emerging markets leverage mobile-first shopping behaviors to bypass traditional retail constraints. IKEA's strategic price reductions totaling EUR 2.1 billion in 2024 specifically targeted online channels, demonstrating how market leaders are investing in digital penetration to capture share from traditional retailers .

Urbanisation & Shrinking Living Spaces

Urban density increases are fundamentally altering furniture design requirements, creating structural demand for modular, space-efficient solutions that favor RTA formats over traditional bulky alternatives. Global urbanization rates reached 56.2% in 2024, with Asia-Pacific leading at 68% urban population growth, directly correlating with increased demand for multi-functional furniture that maximizes limited square footage . This demographic shift particularly benefits RTA manufacturers as urban consumers prioritize furniture that can be easily transported through narrow staircases, small elevators, and compact doorways, constraints that assembled furniture cannot navigate. The trend is most pronounced in megacities where average living space per person has decreased by 15-20% over the past decade, forcing consumers to seek furniture solutions that offer storage integration and convertible functionality. Subscription furniture rental platforms like Feather and Fernish have capitalized on this trend by offering RTA-heavy catalogs that enable frequent relocation without assembly complexity, generating turnover rates 3-4 times higher than traditional ownership models.

Perceived Low Durability of Particleboard Items

Consumer perceptions of particleboard durability continue to constrain RTA market expansion, particularly in premium segments where buyers associate flat-pack formats with disposable furniture despite technological advances in engineered wood products. This perception challenge is most acute in developed markets where consumers have experienced early-generation particleboard products that failed prematurely, creating lasting brand associations that manufacturers struggle to overcome through marketing alone. The durability concern is being addressed through material innovations, including particleboard manufactured from organic waste that demonstrates improved moisture resistance and structural integrity, though consumer education remains a significant challenge. Premium RTA manufacturers are responding by offering extended warranties and using solid wood veneers to improve perceived quality, but these solutions increase costs and reduce the price advantage that drives RTA adoption.

Other drivers and restraints analyzed in the detailed report include:

- Cost Advantage of Flat-Pack Logistics

- Expansion of DIY & Big-Box Retail Formats

- Raw-Material Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Home furniture applications command 61.02% market share in 2025 while delivering the strongest growth at 8.12% CAGR through 2031, reflecting consumers' prioritization of residential comfort investments over commercial spending during economic uncertainty. The segment's dominance is driven by millennials and Gen Z demographics who view furniture as lifestyle expressions rather than purely functional purchases, creating demand for customizable, Instagram-worthy pieces that RTA formats can deliver cost-effectively. Office furniture maintains steady demand at approximately 15% market share, driven by hybrid work arrangements that require home office setups, though growth rates remain moderate as corporate spending on traditional office furniture declines.

Hospitality, educational, and healthcare furniture segments collectively represent 20-25% of the RTA market, with hospitality showing strength as hotels and restaurants seek cost-effective furnishing solutions that can withstand frequent use and easy replacement. The healthcare segment benefits from infection control requirements that favor furniture with smooth surfaces and minimal crevices, characteristics that align well with RTA manufacturing techniques. Ashley Furniture's partnership with Samsung to launch Connected Home Experiences demonstrates how home furniture manufacturers are integrating technology to create differentiated value propositions that justify premium pricing.

Wood retained 47.05% share of the Ready to Assemble Furniture market in 2025 thanks to natural aesthetics and consumer familiarity. Enhanced engineered panels sourced from agricultural waste now claim stronger moisture resistance, extending life cycles.

Plastic and polymer materials are gaining traction through innovations in injection molding and composite manufacturing that enable furniture grade strength and finish quality previously achievable only with traditional materials. The segment's growth is particularly strong in outdoor furniture applications where weather resistance is paramount, and in children's furniture where safety and easy cleaning are prioritized over traditional aesthetics. Other materials, including glass, fabric, and composite materials, collectively represent 15-20% of the market with specialized applications in premium and niche segments.

The Ready To Assemble Furniture Market Report is Segmented by Application (Home Furniture, Office Furniture, Hospitality Furniture, and Other), Material (Wood, Metal, Plastic & Polymer, Other Materials), Price Range (Economy, Mid-Range, Premium), Distribution Channel (B2C/Retail, B2B/Project), and Geography (North America, and Other). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 38.20% of 2025 revenue, propelled by entrenched DIY culture and an expansive network of home-improvement superstores. U.S. consumers purchase desk and storage kits for remote work setups, while Canadian buyers favor modular wardrobes for condo living. Nearshoring to Mexico trims transit days and buffers currency swings, enabling responsive replenishment. Tenants in major metros subscribe to rental platforms that keep demand flowing year-round.

Asia-Pacific is on track for a 9.05% CAGR, the fastest worldwide. China remains the production engine and a sizable domestic market, yet rising labor costs drive incremental capacity to Vietnam and Malaysia. Smartphone ownership above 80% lets Indian and Southeast Asian shoppers visualize products in small apartments before committing. Government quality standards, such as India's mandatory BIS certification, elevate branded imports over informal local offerings .

Europe posts moderate growth as manufacturers combat energy price inflation and stricter sustainability rules. Despite Germany's 2024 sales dip, the region benefits from automation advances and consumer emphasis on circular economy principles. Southern Europe's tourism revival fuels hospitality furniture refurbishments. Outside the three largest regions, South America, the Middle East, and Africa grow from a smaller base, driven by urban migration and expanding middle-class cohorts that appreciate affordable modern designs.

- Inter IKEA Systems B.V.

- Sauder Woodworking Co.

- Dorel Industries Inc.

- Tvilum A/S

- Steinhoff International

- Ashley Furniture Industries

- Godrej Interio

- Alphason Designs

- Bush Industries Inc.

- Fabritec (EuroStyle)

- Simplicity Sofas

- Nitori Holdings Co.

- Wayfair Inc.

- Home Reserve LLC

- West Fraser (panel supply)

- Kronospan

- Egger Group

- Arauco

- Greenpanel Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing e-commerce penetration for furniture

- 4.2.2 Urbanisation & shrinking living spaces

- 4.2.3 Cost advantage of flat-pack logistics

- 4.2.4 Expansion of DIY & big-box retail formats

- 4.2.5 Subscription-based furniture rental platforms boosting RTA turnover

- 4.2.6 Smartphone AR assembly guides enhancing DIY adoption

- 4.3 Market Restraints

- 4.3.1 Perceived low durability of particleboard items

- 4.3.2 Raw-material price volatility

- 4.3.3 Shortage of skilled assemblers in emerging markets

- 4.3.4 Embedded digital-traceability mandates increasing component costs

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

- 4.8 Insights on Regulatory Framework and Industry Standards for the Furniture Industry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Home Furniture

- 5.1.1.1 Chairs

- 5.1.1.2 Tables (side, coffee, dressing, etc.)

- 5.1.1.3 Beds

- 5.1.1.4 Wardrobes

- 5.1.1.5 Sofas

- 5.1.1.6 Dining Tables / Dining Sets

- 5.1.1.7 Kitchen Cabinets

- 5.1.1.8 Other Home Furniture (bathroom, outdoor, etc.)

- 5.1.2 Office Furniture

- 5.1.2.1 Chairs

- 5.1.2.2 Tables

- 5.1.2.3 Storage Cabinets

- 5.1.2.4 Desks

- 5.1.2.5 Sofas & Other Soft Seating

- 5.1.2.6 Other Office Furniture

- 5.1.3 Hospitality Furniture

- 5.1.4 Educational Furniture

- 5.1.5 Healthcare Furniture

- 5.1.6 Other Applications (public places, retail malls, government offices, etc.)

- 5.1.1 Home Furniture

- 5.2 By Material

- 5.2.1 Wood

- 5.2.2 Metal

- 5.2.3 Plastic & Polymer

- 5.2.4 Other Materials

- 5.3 By Price Range

- 5.3.1 Economy

- 5.3.2 Mid-Range

- 5.3.3 Premium

- 5.4 By Distribution Channel

- 5.4.1 B2C / Retail

- 5.4.1.1 Home Centers

- 5.4.1.2 Specialty Furniture Stores

- 5.4.1.3 Online

- 5.4.1.4 Other Distribution Channels

- 5.4.2 B2B / Project

- 5.4.1 B2C / Retail

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 United States

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX

- 5.5.3.7 NORDICS

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South-East Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East & Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East & Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Inter IKEA Systems B.V.

- 6.4.2 Sauder Woodworking Co.

- 6.4.3 Dorel Industries Inc.

- 6.4.4 Tvilum A/S

- 6.4.5 Steinhoff International

- 6.4.6 Ashley Furniture Industries

- 6.4.7 Godrej Interio

- 6.4.8 Alphason Designs

- 6.4.9 Bush Industries Inc.

- 6.4.10 Fabritec (EuroStyle)

- 6.4.11 Simplicity Sofas

- 6.4.12 Nitori Holdings Co.

- 6.4.13 Wayfair Inc.

- 6.4.14 Home Reserve LLC

- 6.4.15 West Fraser (panel supply)

- 6.4.16 Kronospan

- 6.4.17 Egger Group

- 6.4.18 Arauco

- 6.4.19 Greenpanel Industries

7 Market Opportunities & Future Outlook

- 7.1 AI-Guided Assembly Systems with QR & IoT Integration

- 7.2 Smart Modular RTA Furniture with Built-In Connectivity