PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934784

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934784

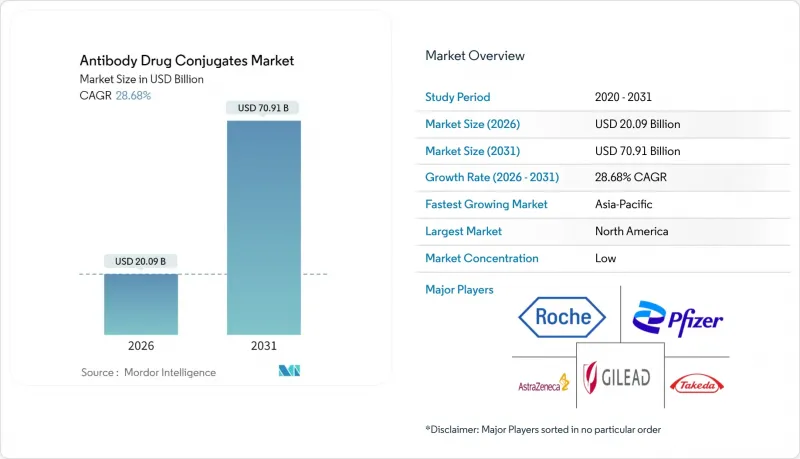

Antibody Drug Conjugates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Antibody Drug Conjugate market size in 2026 is estimated at USD 20.09 billion, growing from 2025 value of USD 15.61 billion with 2031 projections showing USD 70.91 billion, growing at 28.68% CAGR over 2026-2031.

This expansion mirrors a clear shift within the broader Antibody Drug Conjugate industry toward precision oncology, where the capacity to deliver potent cytotoxins directly to malignant cells limits systemic toxicity. Investors frequently cite the improved therapeutic index of ADCs as a catalyst for capital allocation, a trend that is visibly lowering the risk appetite required to fund early-stage development. A further implication is that hospitals continue to reengineer oncology pathways to accommodate day-care infusions rather than multi-day inpatient chemotherapy regimens. These workflow changes appear to shorten bed occupancy and indirectly improve hospital operating margins, reinforcing the attractiveness of ADC adoption.

Parallel to those clinical and financial advantages, competitive consolidation is gathering speed. Pfizer's USD 43 billion acquisition of Seagen provides an integrated platform covering linker chemistry, potent payloads, and commercial scale. Upstream, Daiichi Sankyo is building a USD 152 million high-potency plant in Shanghai to ensure uninterrupted Enhertu supply as Chinese reimbursement expands. Regulatory agencies are also sharpening expectations: the United States Food and Drug Administration released stand-alone clinical-pharmacology guidance for ADCs in March 2024, raising quality benchmarks on drug-to-antibody ratio (DAR) consistency.

Global Antibody Drug Conjugates Market Trends and Insights

Rising Incidences of Solid Tumors: Expanding ADC Applications Beyond Hematological Malignancies

Solid tumors increasingly account for the largest share of new ADC trials, propelled by response rates once limited to blood cancers. Early-phase data for a HER2-mutant non-small cell lung cancer candidate demonstrated an overall response rate north of 38%, underscoring class versatility . That efficacy is spurring clinicians to re-evaluate entrenched chemotherapy backbones, especially in tumors with long-standing drug resistance. An immediate outcome is that contract manufacturers report longer order books for cleavable linkers optimized for solid-tumor microenvironments, hinting at forthcoming production scale-ups.

Rapid Expansion of the >=65-Year Demographic: Driving Demand for Targeted Therapies with Improved Safety Profiles

Demographic aging is swelling the pool of oncology patients who cannot tolerate intensive cytotoxics, elevating demand for ADCs with outpatient-friendly safety profiles. Observational evidence shows body-fat distribution influences dose reductions for trastuzumab deruxtecan, prompting clinicians to personalize regimens for older adults. Imaging centers now integrate body-composition analytics into routine staging, subtly raising diagnostic revenues . Payers increasingly view ADCs as tools to offset downstream hospitalization costs, leading to more favorable reimbursement decisions.

Payload Supply Constraints Causing Production Bottlenecks: Manufacturing Challenges Limiting Market Growth

Auristatin and PBD payloads remain in constrained supply, largely due to the complex containment requirements of high-potency active ingredients. New multi-billion-dollar facilities in Singapore and Shanghai show that firms are internalizing production to safeguard launch timelines. Despite these projects, procurement teams still hedge risk by exploring alternative payload classes that require lower handling stringency. This effort indirectly boosts demand for next-generation linkers capable of accommodating varied chemical moieties, fostering incremental process innovations.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated R&D Funding and Clinical Trial Initiations: Expanding the ADC Pipeline

- Growing Pharmaceutical Investments: Strategic Acquisitions Reshaping the Competitive Landscape

- Increasing Demand for Low-Toxicity and Effective Drugs: ADCs Offering Superior Therapeutic Index

- Regulatory Uncertainties Around Novel Payloads

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Enhertu commands 22.80% Antibody Drug Conjugate market share in 2025, and its forecast CAGR of 30.17% indicates continued leadership through 2031. That momentum stems from approvals spanning breast, gastric, and lung cancers, creating a multi-indication revenue stream. Clinical evidence showing superiority over conventional first-line HER2 regimens suggests payers may soon face pressure to broaden front-line coverage.

Adcetris retains relevance in hematology, but an expansion effort into large B-cell lymphoma hints at renewed growth potential. Padcev's combination with pembrolizumab for urothelial cancer has cut mortality risk by nearly half, bolstering uptake in community settings. Emerging assets such as sacituzumab tirumotecan highlight a pipeline tilt toward dual-payload configurations, offering differentiation in refractory disease. Collectively, these products underscore that the Antibody Drug Conjugate market size benefits from both breadth of indications and depth of data in specific cancers.

Cleavable linkers accounted for roughly 69.20% of the Antibody Drug Conjugate market size in 2025, yet site-specific conjugation technologies are set to grow at over 30.08% CAGR through 2031. Exo-cleavable designs offer enhanced systemic stability while ensuring reliable intracellular release, a combination valued by regulators.

Site-specific platforms employing enzymatic or genetic-code expansion methods yield homogeneous drug-antibody ratios that can support lower clinical doses. The trajectory implies manufacturing analytics will shift toward high-throughput DAR confirmation assays, creating new business for specialty contract research organizations. Non-cleavable linkers, while shrinking in share, remain favored for payloads susceptible to premature cleavage, ensuring niche demand persists.

The Antibody Drug Conjugates Market Report Segments the Industry Into by Product Type (Adcetris, Kadcyla, and More), by Application (Blood Cancer, Breast Cancer, and More), by Technology (Clevable Linker, and More), by Target Type (CD30 Antibodies, and More), by End User, and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 41.20% of the global Antibody Drug Conjugate market size in 2025, buoyed by early FDA approvals and concentrated research infrastructure. Physician familiarity with biomarker testing ensures rapid patient identification, a factor that compresses adoption lag. The region's reimbursement frameworks now include ADC-specific payment codes, shortening revenue recognition cycles for new launches. As U.S. oncology networks integrate telehealth, follow-up visits for manageable toxicities shift to virtual platforms, freeing clinic capacity.

Asia-Pacific is the fastest-growing territory with a projected CAGR above 31.43% to 2031, driven by rising cancer incidence and supportive national insurance policies. China's inclusion of an ADC in its reimbursement list led to notable upticks in prescription volume, illustrating how policy steers uptake. Indigenous firms are entering global trials, hinting at future export ambitions. Japan's outpatient payment reform underpins hospital economics by incentivizing day-care infusions. A plausible knock-on effect is that regional contract manufacturers specializing in high-potency payloads will attract multinational partnerships, elevating Asia-Pacific's manufacturing clout.

Europe retains meaningful Antibody Drug Conjugate market share, backed by robust health-technology-assessment processes and specialized treatment centers. Germany's outpatient coding adjustments lower hospital overheads, subtly improving jurisdictional competitiveness. The United Kingdom's Cancer Drugs Fund often grants interim access while full evaluation proceeds, shortening patient wait times. Middle Eastern and South American markets, although smaller, exhibit early adoption trends in tertiary centers, signaling future growth pockets. These regions may deploy managed-entry agreements to mitigate budget impact, creating fertile ground for value-based-pricing pilots.

- Pfizer Inc. (Seagen Inc.)

- Roche

- AstraZeneca

- Abbvie

- Daiichi Sankyo Co. Ltd

- Gilead Sciences

- Takeda Pharmaceuticals

- ADC Therapeutics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising incidences of solid tumors

- 4.2.2 Rapid expansion of >=65-yr demographic

- 4.2.3 Accelerated R&D funding and clinical trial initiations

- 4.2.4 Growing pharmaceutical investments

- 4.2.5 Increasing demand for low-toxcity and effective drugs

- 4.2.6 Reimbursement expansion for outpatient ADC administration in Japan & Germany

- 4.3 Market Restraints

- 4.3.1 High treatment costs

- 4.3.2 Payload supply constraints (auristatin/PBD) causing production bottlenecks

- 4.3.3 Competition from emerging T-cell engagers & bispecific antibodies

- 4.3.4 High manufacturing complexity

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value - USD)

- 5.1 By Product

- 5.1.1 Adcetris (brentuximab vedotin)

- 5.1.2 Kadcyla (trastuzumab emtansine)

- 5.1.3 Padcev (enfortumab vedotin)

- 5.1.4 Polivy (polatuzumab vedotin)

- 5.1.5 Enhertu (trastuzumab deruxtecan)

- 5.1.6 Trodelvy (sacituzumab govitecan)

- 5.1.7 Elahere (mirvetuximab soravtansine)

- 5.1.8 Other Approved ADCs

- 5.2 By Linker Chemistry

- 5.2.1 Cleavable Linkers

- 5.2.2 Non-cleavable Linkers

- 5.2.3 Site-specific / Next-Gen Conjugation Technologies

- 5.3 By Target Antigen

- 5.3.1 HER2

- 5.3.2 CD30

- 5.3.3 TROP2

- 5.3.4 CD22

- 5.3.5 Others

- 5.4 By Application (Indication)

- 5.4.1 Breast Cancer

- 5.4.2 Blood Cancers (Lymphoma, Leukaemia)

- 5.4.3 Urothelial Cancer

- 5.4.4 Lung Cancer

- 5.4.5 Gynaecologic Cancers (Ovary, Endometrium)

- 5.4.6 Other Solid Tumours

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Specialty Cancer Centres

- 5.5.3 Biopharma & Contract Research Organisations

- 5.5.4 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Pfizer Inc. (Seagen Inc.)

- 6.4.2 F. Hoffmann-La Roche Ltd

- 6.4.3 AstraZeneca plc

- 6.4.4 AbbVie Inc.

- 6.4.5 Daiichi Sankyo Co. Ltd

- 6.4.6 Gilead Sciences Inc.

- 6.4.7 Takeda Pharmaceutical Co. Ltd

- 6.4.8 ADC Therapeutics SA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment