PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934851

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934851

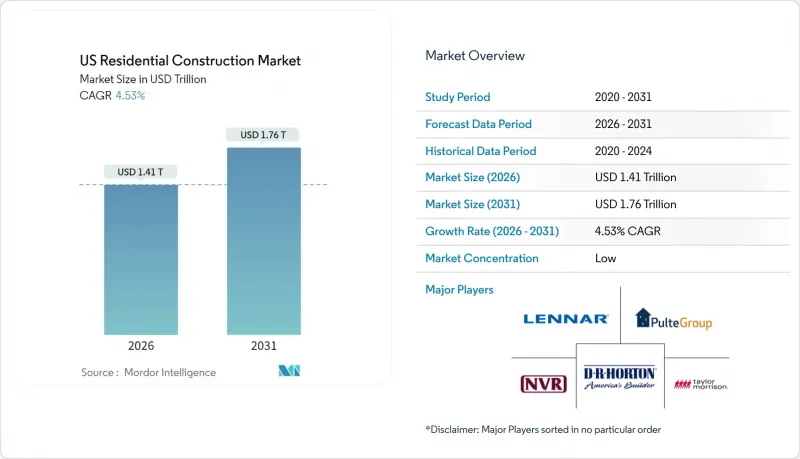

US Residential Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The US residential construction market size in 2026 is estimated at USD 1.41 trillion, growing from 2025 value of USD 1.35 trillion with 2031 projections showing USD 1.76 trillion, growing at 4.53% CAGR over 2026-2031.

Robust demographic momentum, larger institutional capital allocations, and accelerated technology adoption anchor this expansion, even as developers navigate cyclical mortgage-rate shifts. Migration toward Sun Belt metros, supportive zoning reforms, and federal energy-efficiency incentives widen the demand base. Builders increasingly differentiate through prefabrication, 3-D printing, and data-driven project management platforms, while shifting insurance and water-supply risks compel geographic diversification. Collectively, these forces recast the US residential construction market as a strategic infrastructure opportunity rather than a short-cycle, rate-sensitive play.

US Residential Construction Market Trends and Insights

Falling Mortgage Rates Improve Affordability

Mortgage rates trending down from 7% to near-6% by late 2025 restores roughly 15% additional buying power, stimulating new-home demand across price points. The easing rate backdrop loosens the "rate-lock" that kept existing owners sidelined, pushing more buyers toward new construction. First-time purchasers now form the majority of funded loans and favor energy-efficient, tech-ready dwellings. Builders respond with smaller footprints and smart-home packages, especially in job-rich secondary metros. The combined effect is a broader, more resilient demand curve, cushioning the US residential construction market against future rate volatility.

Millennial Household Formation Surge

Millennials aged 28-43 will contribute roughly 70% of new household creation through 2030, driving structural demand that transcends short-term economic swings. Their preference for walkable, amenity-rich communities accelerates higher-density projects near transit nodes. The cohort's digital expectations make touchless entry, solar integration, and app-based maintenance indispensable. Sun Belt metros such as Austin and Raleigh draw outsized interest due to lower living costs and robust job pipelines. This demographic wave underpins long-run volume visibility across both single-family and multifamily segments.

Skilled-Labor Shortages

Construction payrolls remain nearly 400,000 workers below their 2007 peak, inflating wages by 15-20% in fast-growing metros. Scarcity in specialized trades elongates schedules and forces builders to retain larger in-house teams or pay premium rates to subcontractors. Immigration policy uncertainty compounds regional gaps, particularly in Texas and Florida. These pressures accelerate investment in robotics, prefabrication, and 3-D printing, yet ramp-up periods limit near-term relief. Consequently, labor scarcity drags on projected output and margins across the US residential construction market.

Other drivers and restraints analyzed in the detailed report include:

- Institutional Build-to-Rent Capital Inflows

- Aging Housing Stock Fuels Remodeling

- Volatile Material Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Apartments and condominiums captured 39.15% of 2025 output, trailing single-family formats yet posting the segment's fastest 6.02% CAGR to 2031, powered by zoning liberalization and institutional capital demand. Investor appetite for scale-ready, rent-generating assets and millennial preferences for walkable communities converge to lift multifamily pipelines in transit-oriented corridors. Projects increasingly integrate co-working lounges, EV-ready parking, and centralized package lockers to serve digital lifestyles.

Single-family construction adapts through smaller lots, paired homes, and community amenities that mimic urban convenience. Builders such as D.R. Horton have rolled out detached rental lines in Texas and Florida, reflecting cross-pollination between segments. Land availability and appraisal norms still anchor villas and landed houses at 60.85% of 2025 volume, but higher-density formats steadily chip away as municipalities pursue housing-supply mandates. Overall, product-mix evolution widens the addressable US residential construction market.

New-build activity retained a 69.05% share in 2025, yet renovation projects expanded faster at a 5.61% CAGR on the back of aging stock and tax-credit support. Energy-retrofit packages, kitchen expansions, and accessory-dwelling-unit conversions push typical budgets above USD 75,000, rivaling entry-level new builds. Contractors specializing in occupied-home workflows gain pricing power and repeat business.

Project pipelines swell in legacy Northeast and Midwest neighborhoods where land scarcity curtails ground-up development. Builders such as Lennar have launched dedicated remodeling divisions to hedge cycle risk and meet customer demand. The robust retrofit niche, therefore, deepens the resilience of the US residential construction market size.

The US Residential Construction Market Report is Segmented by Type (Apartment & Condominiums, Villas and Landed Houses), by Construction Type (New Construction and Renovation), by Construction Method (Conventional On-Site, and More), by Investment Source (Public and Private), and by Region (Northeast, Midwest, Southeast, West, and Southwest). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- D.R. Horton

- Lennar Corporation

- PulteGroup

- NVR

- Taylor Morrison

- KB Home

- Meritage Homes

- Clayton Properties Group

- Century Communities

- LGI Homes

- Toll Brothers

- Tri Pointe Homes

- Beazer Homes

- Greystar

- Alliance Residential

- Mill Creek Residential

- Wood Partners

- Trammell Crow Residential

- Related Group

- The NRP Group

- Bridge Investment Group

- Continental Properties Co.

- Boxabl

- Mighty Buildings

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Falling mortgage rates improve affordability

- 4.2.2 Millennial household formation surge

- 4.2.3 Aging housing stock fuels remodeling

- 4.2.4 Institutional build-to-rent capital inflows

- 4.2.5 State-level zoning reforms for higher density

- 4.2.6 IRA heat-pump tax credits accelerate retrofits

- 4.3 Market Restraints

- 4.3.1 Skilled-labor shortages

- 4.3.2 Volatile material costs

- 4.3.3 Insurance-premium spikes in climate-risk zones

- 4.3.4 Water-scarcity building moratoriums

- 4.4 Government Initiatives & Vision

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Force Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing (Construction Materials) and Construction Cost (Materials, Labour, Equipment) Analysis

- 4.9 Comparison of Key Industry Metrics of the United States with Other Countries

- 4.10 Key Upcoming/Ongoing Projects (with a focus on Mega Residential Projects)

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Type

- 5.1.1 Apartment & Condominiums

- 5.1.2 Villas and Landed Houses

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Renovation

- 5.3 By Construction Method

- 5.3.1 Conventional On-Site

- 5.3.2 Modern Methods of Construction (Prefabricated, Modular, etc)

- 5.4 By Investment Source

- 5.4.1 Public

- 5.4.2 Private

- 5.5 By Region

- 5.5.1 Northeast (New York, Massachusetts, Pennsylvania, etc.)

- 5.5.2 Midwest (Illinois, Ohio, Michigan, etc.)

- 5.5.3 Southeast (Florida, Georgia, North Carolina, etc.)

- 5.5.4 West (California, Washington, Colorado, etc.)

- 5.5.5 Southwest (Texas, Arizona, New Mexico, etc.)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 D.R. Horton

- 6.4.2 Lennar Corporation

- 6.4.3 PulteGroup

- 6.4.4 NVR

- 6.4.5 Taylor Morrison

- 6.4.6 KB Home

- 6.4.7 Meritage Homes

- 6.4.8 Clayton Properties Group

- 6.4.9 Century Communities

- 6.4.10 LGI Homes

- 6.4.11 Toll Brothers

- 6.4.12 Tri Pointe Homes

- 6.4.13 Beazer Homes

- 6.4.14 Greystar

- 6.4.15 Alliance Residential

- 6.4.16 Mill Creek Residential

- 6.4.17 Wood Partners

- 6.4.18 Trammell Crow Residential

- 6.4.19 Related Group

- 6.4.20 The NRP Group

- 6.4.21 Bridge Investment Group

- 6.4.22 Continental Properties Co.

- 6.4.23 Boxabl

- 6.4.24 Mighty Buildings

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment