PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934866

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934866

Bread Crumbs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

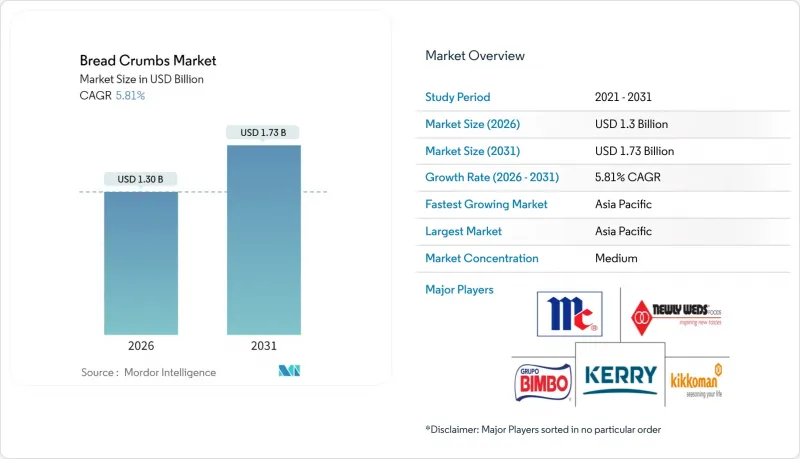

Bread crumbs market size in 2026 is estimated at USD 1.3 billion, growing from 2025 value of USD 1.23 billion with 2031 projections showing USD 1.73 billion, growing at 5.81% CAGR over 2026-2031.

The market is experiencing robust growth due to several factors, including the increasing consumer preference for convenience foods and the continuous expansion of quick-service restaurants worldwide. Food manufacturers are making substantial investments in texture-enhancing ingredients to develop premium product offerings that meet evolving consumer preferences. The industry is witnessing significant technological advancements, particularly in panko production automation and smart packaging solutions, which help extend product shelf life while enhancing product differentiation and profit margins. In response to growing consumer health concerns, regulatory bodies have intensified their focus on allergen disclosure requirements, compelling larger manufacturers to implement sophisticated manufacturing systems. This trend particularly benefits companies with scale operations that can consistently maintain and guarantee specific gluten thresholds. Furthermore, the European market is experiencing a transformation driven by sustainability legislation, which is encouraging manufacturers to transition toward recyclable packaging solutions. This shift has established packaging innovation as a crucial competitive advantage in the bread crumbs market.

Global Bread Crumbs Market Trends and Insights

Growing Consumer Preference for Convenience Foods

The convenience food revolution is reshaping breadcrumb demand patterns. This growth correlates with increased breadcrumb consumption as manufacturers use these ingredients for texture enhancement and binding in ready-to-eat meals. The expansion of frozen ready meals, particularly in North America and Western Europe, creates consistent demand for breadcrumbs as coating agents that maintain crispness during microwave preparation. Premium convenience foods require specialized breadcrumb formulations, extending beyond basic coating applications to texture engineering. The foodservice industry's e-commerce adoption, with distributors investing in technology and value-added services, increases demand through broader distribution of breadcrumb-enhanced convenience products. The combination of convenience culture and technological distribution capabilities establishes breadcrumbs as essential components in the food ecosystem.

Advancements In Packaging Technologies for Improved Shelf Life and Product Safety

Packaging innovation has emerged as a key competitive advantage in the breadcrumb market, highlighted by OSY Group securing EURO 750,000 funding in May 2024 to develop antimicrobial coatings. These coatings help protect fresh produce by removing harmful microbes from packaging surfaces. The industry has benefited from smart packaging advances, such as quality monitoring sensors and specialized atmosphere packaging that stops bacteria from growing, ensuring breadcrumbs stay fresh during transport and storage. Companies are now using plant-based packaging solutions that work on two levels - they keep products fresh and help the environment through biodegradable materials that naturally fight bacteria. Natural coatings applied directly to breadcrumbs offer a practical solution by keeping moisture in and harmful organisms out while maintaining product freshness. These advances help manufacturers stand out through better product quality rather than just price, creating opportunities for premium products with better profit margins while meeting environmental goals.

Stringent Food Safety and Labeling Regulations

Global regulatory requirements for breadcrumb products are undergoing significant changes that affect manufacturers of all sizes. The FDA's FSIS Directive 7,230.1 has introduced comprehensive measures requiring companies to verify "Big 9" allergen labeling for wheat-based breadcrumb products . This includes detailed ingredient declarations and implementation of robust cross-contamination prevention protocols. In the Canadian market, the Food Inspection Agency has established detailed labeling distinctions between "enriched bread crumbs" and "toasted wheat crumbs," which manufacturers must follow based on the characteristics of source materials . European manufacturers face additional challenges with EU Regulation 2025/40, which mandates the transition to recyclable packaging by 2030 and implements extended producer responsibility frameworks for all packaging producers . These regulatory developments have created substantial compliance requirements that particularly impact small manufacturers' operational costs, while potentially shifting market advantage toward larger companies that have well-established quality management systems. The FDA's approach to allergen thresholds, while essential for consumer safety, requires manufacturers to implement comprehensive monitoring systems and maintain detailed documentation throughout their supply chain operations.

Other drivers and restraints analyzed in the detailed report include:

- Ongoing Innovation in Bread Crumb Production Methods

- Rising Demand for Breadcrumbs in Bakery and Snack Products

- Allergen Concerns Limiting Consumer Base

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Panko breadcrumbs hold a 45.88% market share in 2025 and are projected to grow at a 6.83% CAGR through 2031. Their superior oil absorption and distinctive texture provide lighter, crispier coatings compared to traditional breadcrumbs. The growth in this segment is driven by foodservice industry expansion and increased consumer interest in Japanese cuisine. The unique manufacturing process of panko involves producing crustless bread followed by specialized shredding and drying, which creates its characteristic airy texture that enhances various culinary applications across restaurants, food manufacturers, and home cooking.

Fresh breadcrumbs maintain consistent demand in artisanal and premium food segments, especially in European markets where traditional cooking methods remain prevalent. These breadcrumbs are particularly valued in high-end restaurants and specialty food production for their ability to provide authentic textures and flavors. Dry breadcrumbs continue to dominate mass-market applications, including ready-to-eat meals and processed foods, serving as a versatile ingredient in industrial food production and commercial kitchens where consistency and longer shelf life are essential requirements.

Multi-grain breadcrumbs are projected to grow at a CAGR of 6.89% through 2031, while wheat-based products hold a 61.85% market share in 2025. This trend reflects increasing consumer demand for nutritious alternatives in their daily diet. The shift toward healthier options has prompted manufacturers to diversify their product portfolios, with companies like Bimbo Bakeries USA incorporating diverse ingredients such as chickpea flour and pea protein into their product lines.

The Whole Grains Council's promotion of heritage grains, including amaranth, quinoa, and spelt, has encouraged consumers to explore non-wheat alternatives in their food choices . This growing interest in ancient grains has created significant opportunities for manufacturers to develop innovative products that combine traditional and alternative flours, meeting the evolving preferences of health-conscious consumers while maintaining the familiar taste and texture profiles they expect.

The Bread Crumbs Market Report is Segmented by Crumb Type (Dry, Fresh, Panko, and Others), Ingredient (Wheat-Based, Corn-Based, Rice-Based, and More), Flavor (Unflavored, and Flavored), Distribution Channel (Foodservice, and Retail), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific has established itself as the dominant force in the global breadcrumb market, commanding a substantial 51.02% market share in 2025. The region's strong market position is underpinned by China's thriving restaurant industry, which has witnessed remarkable revenue growth and increased adoption of breadcrumbs in both traditional and fusion cuisine. India's food processing sector continues to expand, making it a key market for breadcrumb applications in ready-to-eat meals and processed foods. Japan's market is shaped by unique dietary trends, particularly the government-driven emphasis on fiber fortification in bakery products, which has created opportunities for specialized breadcrumb formulations.

The region's impressive growth trajectory, marked by a 6.78% CAGR through 2031, reflects the transformative impact of rapid urbanization and rising disposable incomes across Asia-Pacific. This growth is further accelerated by the increasing adoption of Western food preparation methods, where breadcrumbs play a crucial role in enhancing texture and flavor profiles. The combination of economic development and evolving food consumption patterns positions Asia-Pacific as the most dynamic market for breadcrumb manufacturers and suppliers. North America and Europe maintain mature market positions with well-established consumption patterns and stringent regulatory frameworks for food safety and allergen management. The U.S. market structure favors large-scale suppliers due to the concentrated food retail sector, while European manufacturers adapt to new sustainability requirements in packaging. In emerging regions, South America, led by Brazil's growing food processing sector, shows promising development. The Middle East benefits from its young population and expanding restaurant industry, while Africa's market potential is gradually unlocking through improved infrastructure and urbanization, particularly in Nigeria and South Africa.

- Kerry Group plc

- Newly Weds Foods Inc.

- McCormick & Company Inc.

- Kikkoman Corporation

- Grupo Bimbo SAB de CV

- Goya Foods Inc.

- Premier Foods Group Limited (Paxo)

- George Weston Foods Ltd.

- Orkla ASA

- Dr. Schar

- WK Kellogg Co

- Ajinomoto Co., Inc.

- Brata GmbH

- Quality Foods

- American Bread Crumb Co.

- ABS FOODS LTD.

- Sungrano Gmbh

- Vigo Foods

- Our Family Foods

- Walmart Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Consumer Preference for Convenience Foods

- 4.2.2 Advancements In Packaging Technologies for Improved Shelf Life and Product Safety

- 4.2.3 Ongoing Innovation in Bread Crumb Production Methods

- 4.2.4 Rising Demand for Breadcrumbs in Bakery and Snack Products

- 4.2.5 Increased Use of Global/Ethnic Cuisine Fusion

- 4.2.6 Product Utility for Texture, Binding, And Flavor Enhancement

- 4.3 Market Restraints

- 4.3.1 Stringent Food Safety and Labeling Regulations

- 4.3.2 Allergen Concerns Limiting Consumer Base

- 4.3.3 Rising Demand for Low-Carb or Keto Diets Reducing Usage

- 4.3.4 Environmental Concerns Regarding Single-Use or Non-Sustainable Packaging

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.6.5.1 ewe

5 MARKET SIZE and GROWTH FORECASTS (VALUE)

- 5.1 By Crumb Type

- 5.1.1 Dry

- 5.1.2 Fresh

- 5.1.3 Panko

- 5.1.4 Others

- 5.2 By Ingredient

- 5.2.1 Wheat-Based

- 5.2.2 Corn-Based

- 5.2.3 Rice-Based

- 5.2.4 Multi-Grain

- 5.2.5 Others

- 5.3 By Flavor

- 5.3.1 Unflavored

- 5.3.2 Flavored

- 5.4 By Distribution Channel

- 5.4.1 Foodservice

- 5.4.2 Retail

- 5.4.2.1 Supermarkets and Hypermarkets

- 5.4.2.2 Convenience Stores

- 5.4.2.3 Online Retail

- 5.4.2.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Kerry Group plc

- 6.4.2 Newly Weds Foods Inc.

- 6.4.3 McCormick & Company Inc.

- 6.4.4 Kikkoman Corporation

- 6.4.5 Grupo Bimbo SAB de CV

- 6.4.6 Goya Foods Inc.

- 6.4.7 Premier Foods Group Limited (Paxo)

- 6.4.8 George Weston Foods Ltd.

- 6.4.9 Orkla ASA

- 6.4.10 Dr. Schar

- 6.4.11 WK Kellogg Co

- 6.4.12 Ajinomoto Co., Inc.

- 6.4.13 Brata GmbH

- 6.4.14 Quality Foods

- 6.4.15 American Bread Crumb Co.

- 6.4.16 ABS FOODS LTD.

- 6.4.17 Sungrano Gmbh

- 6.4.18 Vigo Foods

- 6.4.19 Our Family Foods

- 6.4.20 Walmart Inc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK