PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934909

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934909

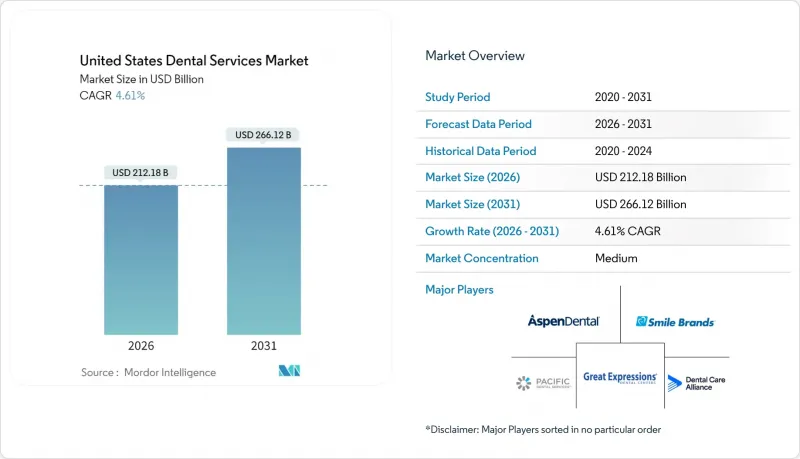

United States Dental Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States dental services market is expected to grow from USD 202.83 billion in 2025 to USD 212.18 billion in 2026 and is forecast to reach USD 266.12 billion by 2031 at 4.61% CAGR over 2026-2031.

Robust growth persists despite staffing shortages and input-cost inflation because of shifting demographics, expanded Medicare Advantage dental benefits for several seniors, and accelerated Dental Service Organization (DSO) consolidation all stimulate patient volumes. A rising prevalence of untreated oral diseases, rapid uptake of clear-aligner solutions, and broader employer-sponsored coverage maintain sustained procedure demand across age groups. DSOs leverage scale to centralize procurement and technology investments, thereby squeezing operating costs that challenge independent clinics. Meanwhile, technology-forward practices adopt intraoral scanners and AI diagnostics to shorten chair time and elevate patient satisfaction. This reinforces a digital transformation cycle that underpins the United States dental services market's next growth phase.

United States Dental Services Market Trends and Insights

Rising burden of untreated oral diseases

Periodontal disease affects 45% of U.S. adults and generates an annual economic burden of USD 154 billion through lost productivity and emergency interventions. These untreated cases cluster in rural counties where 65% of jurisdictions are dental health professional shortage areas, creating a backlog that mobile units and teledentistry platforms have begun to serve. Value-based reimbursement now rewards early detection, spurring clinics to adopt chairside diagnostics that flag incipient caries before they escalate into costly endodontic work. Integrating oral screenings into primary-care checkups further enlarges the United States dental services market by capturing patients who historically went untreated. Practices that embed medical-dental collaboration can tap previously unserved populations and elevate prevention revenues while lowering long-term restorative costs.

Rapid uptake of clear-aligner & digital workflows

Intraoral scanners reached 53% penetration among surveyed dentists in 2024, enabling same-day crowns and trimming visit counts for restorative work. Align Technology reported that adults constituted 70% of its 2024 clear-aligner start volume, spotlighting broader demand outside adolescent cohorts. Fully digital workflows raise productivity by 25% and boost patient satisfaction by 15%, strengthening the competitive position of early adopters. Artificial intelligence now forecasts tooth movement and points out margin errors before print jobs start, cutting rework rates. As direct-to-consumer clear-aligner brands market aggressively, professional offices pivot to hybrid offerings that combine DTC convenience with clinical oversight to safeguard outcomes.

High procedure cost & limited cosmetic coverage

Patient out-of-pocket expense for major restorative or cosmetic work can exceed USD 5,000, discouraging uptake among middle-income households. Insurance rarely reimburses elective veneers or whitening, segmenting demand toward affluent groups and restricting broader adoption of high-margin services. Dental financing platforms and membership subscriptions aim to bridge affordability gaps, yet uptake remains concentrated in urban markets. Rising tariffs on imported alloys and resin compounds compound cost pressure for practices, weighing on patient acceptance rates. Without broader third-party reimbursement, discretionary spending limits will temper upside for cosmetic volumes over the near term.

Other drivers and restraints analyzed in the detailed report include:

- Growing DSO penetration & private-equity funding

- Expansion of Medicare Advantage dental benefits

- Staffing shortages of hygienists & assistants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Endodontics accounted for 23.05% of the United States dental services market share in 2025, reflecting persistent caries prevalence and the clinical imperative to preserve natural dentition. Procedure fees ranging from USD 1,200 to USD 2,500 sustain attractive economics, and technological advances such as rotary instrumentation shorten operatory cycles, enhancing throughput. Endodontic demand also benefits from expanded insurance coverage of medically necessary root canal therapy, which tempers out-of-pocket exposure for patients. Meanwhile, the cosmetic segment is pacing growth at a 5.05% CAGR through 2031. Social media aesthetics, digital smile design, and growing disposable income collectively propel elective veneer, whitening, and aligner uptake. Chairside CAD-CAM adoption permits same-day veneers, trimming opportunity cost for busy professionals and supporting premium pricing.

Cosmetic procedures still face coverage gaps that confine adoption to higher-income brackets, yet financing programs and retail clinic channels broaden reach incrementally. Manufacturers release biocompatible, translucent zirconia that meets both cosmetic and functional mandates, narrowing trade-offs between beauty and longevity. Endodontic specialists confront encroachment from general dentists using cone-beam CT imaging; nonetheless, referral flows remain robust for molar treatments with complex canal morphology. Competitive advantage hinges on integrating AI-guided length determination and single-visit protocols to elevate patient experience.

The Above 17 - Up to 65 cohort contributed 53.72% of the United States dental services market size in 2025, underpinned by private insurance prevalence and stable employment income that funds restorative and elective care. This segment generates steady hygiene recall visits and rising interest in clear-aligner therapy as appearance expectations escalate in professional settings. Concurrently, the Up to 17 demographic is expanding fastest at a 5.35% CAGR, buoyed by Medicaid pediatric coverage and employer plans that now include fluoride varnish and sealant benefits. Preventive outreach in schools identifies caries early, and teledentistry follow-ups lower parental work disruption, reinforcing care adherence.

Seniors above 65 gain momentum as Medicare Advantage dental benefits widen eligibility, unlocking incremental procedure volumes and larger average case values due to multi-unit implants and periodontal maintenance. Generation Z introduces new consumer behavior, such as appointment booking via mobile apps and preference for eco-friendly materials. Practices configuring digital communication and flexible financing will secure loyalty across life stages, supporting lifetime patient value in the United States dental services market.

The United States Dental Services Market Report is Segmented by Service Type (Dental Implants, Endodontics, and More), Patient Age Group (Up To 17 and More), Provider Model (Independent and More), Service Provider (Hospitals, Dental Clinics, Others), and Payment Method (Private Insurance, Public Insurance, Out-Of-Pocket). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 32 Dental

- Affordable Care

- Aspen Dental Management, Inc.

- ClearChoice Dental Implant Centers

- Coast Dental

- Decision One Dental Partners

- Dental Care Alliance

- Dental Service Group

- Gentle Dental

- Great Expressions Dental Centers

- Heartland Dental

- InterDent

- MB2 Dental

- Midwest Dental

- Mondovi Dental

- Pacific Dental Services

- Smile 360

- Smile Brands Inc.

- Smile Doctors

- Sonrava Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Burden of Untreated Oral Diseases

- 4.2.2 Rapid Uptake of Clear-Aligner & Digital Workflows

- 4.2.3 Growing DSO Penetration & Private-Equity Funding

- 4.2.4 Expansion of Medicare Advantage Dental Benefits

- 4.2.5 AI-Driven Diagnostic Support Reducing Chair-Time

- 4.2.6 Retail-Clinic Models Inside Big-Box Stores

- 4.3 Market Restraints

- 4.3.1 High Procedure Cost & Limited Cosmetic Coverage

- 4.3.2 Staffing Shortages of Hygienists & Assistants

- 4.3.3 Inflation-Linked Rise in Consumables & Lab Fees

- 4.3.4 State-Level Scope-of-Practice Caps on Mid-Level Providers

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Dental Implants

- 5.1.2 Endodontics

- 5.1.3 Periodontics

- 5.1.4 Orthodontics

- 5.1.5 Dentures

- 5.1.6 Cosmetic Dentistry

- 5.1.7 Others

- 5.2 By Patient Age Group

- 5.2.1 Up to 17

- 5.2.2 Above 17 - Up to 65

- 5.2.3 Above 65

- 5.3 By Provider Model

- 5.3.1 Independent

- 5.3.2 Dental Service Organizations

- 5.3.3 Public

- 5.4 By Service Provider

- 5.4.1 Hospitals

- 5.4.2 Dental Clinics

- 5.4.3 Others

- 5.5 By Payment Method

- 5.5.1 Private Insurance

- 5.5.2 Public Insurance

- 5.5.3 Out-of-Pocket

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 32 Dental

- 6.4.2 Affordable Care

- 6.4.3 Aspen Dental Management, Inc.

- 6.4.4 ClearChoice Dental Implant Centers

- 6.4.5 Coast Dental

- 6.4.6 Decision One Dental Partners

- 6.4.7 Dental Care Alliance

- 6.4.8 Dental Service Group

- 6.4.9 Gentle Dental

- 6.4.10 Great Expressions Dental Centers

- 6.4.11 Heartland Dental

- 6.4.12 InterDent

- 6.4.13 MB2 Dental

- 6.4.14 Midwest Dental

- 6.4.15 Mondovi Dental

- 6.4.16 Pacific Dental Services

- 6.4.17 Smile 360

- 6.4.18 Smile Brands Inc.

- 6.4.19 Smile Doctors

- 6.4.20 Sonrava Health

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment