PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937335

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937335

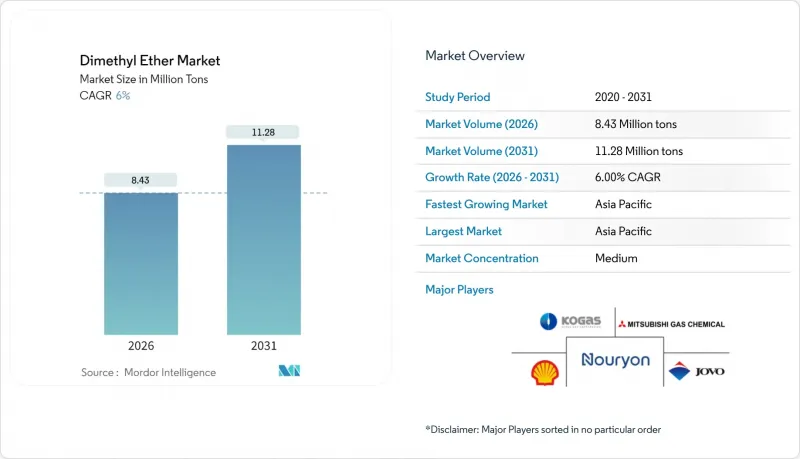

Dimethyl Ether - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Dimethyl Ether market is expected to grow from 7.95 million tons in 2025 to 8.43 million tons in 2026 and is forecast to reach 11.28 million tons by 2031 at 6.00% CAGR over 2026-2031.

Regulatory moves toward ultra-low-sulfur requirements, the pivot to carbon-neutral targets, and dimethyl ether's (DME) seamless fit in existing LPG logistics create a strong demand runway. Asia-Pacific anchors momentum, leveraging China's coal gasification network and cost advantage, while Japan and Korea deploy DME for energy-security diversification. Natural-gas-based output dominates volumes today, yet rapid technology gains in bio-DME routes point to a structural feedstock shift that could recalibrate long-term supply curves. Competitive intensity stays moderate; producers with both conventional methanol-dehydration and emerging CO2 hydrogenation know-how secure optionality as green-hydrogen availability scales.

Global Dimethyl Ether Market Trends and Insights

Growing Demand from LPG Blending Applications

Household energy programs across Indonesia, Malaysia, and Thailand push LPG substitution targets that directly lift volumes in the dimethyl ether market. Indonesia's 15% LPG replacement plan alone could save USD 388 million in import costs and make DME politically attractive due to drop-in compatibility with existing stoves and cylinders. The substitution pathway reduces fiscal exposure to volatile propane prices while letting utilities defer expensive appliance retrofits. Producers benefit from a ready customer base that values fuel cost stability more than marginal efficiency gains. Parallel biomass-to-DME pilots using palm-oil waste and rice husks align with local circular-economy mandates and strengthen rural incomes. These converging factors underpin resilient regional demand even if oil price swings occur.

Increasing Fuel Demand from Transportation and Industrial Boilers

Emission standards for heavy-duty vehicles tighten globally, prompting fleet managers to explore fuels that match diesel performance without diesel's particulate profile. DME offers a 55-60 cetane score and produces virtually no soot, allowing compliance upgrades through fuel switching rather than after-treatment retrofits. Mines, ports and agricultural cooperatives in China already blend DME into on-site diesel pools to meet provincial PM limits. Industrial boilers follow a similar arc; manufacturers installing low-NOx burners find that DME delivers incremental CO2 reductions at acceptable cost because it leverages installed LPG storage tanks. The dimethyl ether market therefore enjoys an expanding total addressable volume across transport and process-heat end-uses while policy-makers enforce stricter air-quality benchmarks.

High Capex/OPEX for Large-Scale Synthesis and Dehydration

Building methanol-to-DME complexes demands specialized reactors and tall distillation columns that lift capital intensity beyond USD 18,000 per ton per year of capacity, squeezing returns in low-margin fuel markets. Operating expenditure remains sensitive to utility prices; steam-demand optimization via dividing-wall columns can trim costs by 44.5%, but commercial references stay limited. Financing hurdles are more acute for greenfield projects in emerging economies where borrowing costs exceed 10%. Investors therefore favor brownfield retrofits or modular skids, tempering mega-plant announcements and potentially slowing the dimethyl ether market expansion rate.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Ultra-Low-Sulfur Household Fuels

- Modular Bio-DME Plants Leveraging Green H2 and Captured CO2

- Competition from LNG, LPG and Green Methanol

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Natural-gas feedstock generated 64.10% of 2025 output, and retained cost superiority through established steam-reforming assets in North America, the Middle East, and Russia. Because these assets piggyback on legacy methanol units, incremental dehydration lines reach cash-cost breakeven below USD 350 per ton, sustaining natural-gas leadership in the dimethyl ether market. Coal-gasification pathways underpin China's production clusters, but environmental penalties and carbon-market exposure gradually compress margins.

The renewable pivot is unmistakable: bio-DME grows at 8.42% CAGR. Scale-ups include Oberon Fuels' plan to lift U.S. capacity beyond 200 million gallons per year and EU consortia targeting woody-biomass gasification. Credits under California's Low Carbon Fuel Standard and the EU's Renewable Energy Directive II deliver monetizable carbon premiums of USD 85-190 per ton, tipping project economics in favor of bio-routes. As electrolyzer costs fall, direct CO2 hydrogenation could further challenge fossil feedstock incumbency, reshaping supply-side dynamics in the dimethyl ether market.

The Dimethyl Ether Report is Segmented by Source (Natural Gas, Coal, and Bio-Based Products), Application (Propellants, LPG Blending, Fuel, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific commanded 86.20% of global volume in 2025, sustaining the highest regional CAGR at 6.10%. China retains a cost advantage through coal-to-DME complexes in Shaanxi and Inner Mongolia, each exceeding 1 million tons per year. Provincial subsidies tied to air-quality attainment credits shield margins even as national carbon pricing tightens. Japan and Korea deepen fuel diversification efforts; Tokyo's hydrogen roadmap cites liquid carriers like DME for maritime bunkering, while Korean refiners deploy blend pumps at LPG import terminals-key developments shaping the dimethyl ether market.

North America trails distantly but leads the technology curve in renewable DME. California's renewable-fuel credit stack, layering federal RINs with state LCFS advantages, yields netbacks over USD 1,400 per ton for low-CI product, drawing capital toward dairy-waste-to-DME clusters in the Central Valley. Canada evaluates policy parity via its Clean Fuel Regulations, signaling cross-border harmonization potential that could enlarge addressable truck-fleet volumes. Mexico explores DME-diesel blends for agriculture, but infrastructure finance hurdles slow uptake.

Europe aligns DME adoption with Green Deal imperatives. Sweden's BioDME demonstration confirmed lignocellulosic pathways, and Denmark's Power-to-X roadmap lists DME for CO2-negative shipping routes. German agencies sponsor Fraunhofer research on polymer-electrolyte-membrane reformers that reconvert DME to hydrogen on board fuel-cell trucks, illustrating deep value-chain innovation. Middle East gas-rich producers weigh DME export options as a monetization lever that avoids LNG liquefaction capital, while African markets focus on household LPG affordability, implying gradual, subsidy-dependent entry pathways-factors guiding regional trajectories in the dimethyl ether market.

- Biofriends Inc.

- DME-Aerosol LLC

- Dongguan Jovo Warehousing Services Co., Ltd.

- GRILLO-Werke AG

- Gruppo SIAD

- Korea Gas Corporation

- Mitsubishi Gas Chemical Company, Inc.

- Nouryon

- Oberon Fuels, Inc.

- Shell PLC

- Sichuan Lutianhua Co., Ltd.

- The Chemours Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand from LPG Blending Applications

- 4.2.2 Increasing Fuel Demand from Transportation and Industrial Boilers

- 4.2.3 Government Incentives for Ultra-Low-Sulfur Household Fuels

- 4.2.4 Modular Bio-DME Plants Leveraging Green H2 and Captured CO2

- 4.2.5 DME as a Hydrogen Carrier for Long-Haul Fuel-Cell Logistics

- 4.3 Market Restraints

- 4.3.1 High Capex/OPEX For Large-Scale Synthesis and Dehydration

- 4.3.2 Competition from LNG, LPG, and Green Methanol

- 4.3.3 Methanol Feedstock Price Volatility Amid E-Methanol Boom

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Rivalry Among Existing Competitors

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Source

- 5.1.1 Natural Gas

- 5.1.2 Coal

- 5.1.3 Bio-based Products

- 5.2 By Application

- 5.2.1 Propellants

- 5.2.2 LPG Blending

- 5.2.3 Fuel

- 5.2.4 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 Indonesia

- 5.3.1.6 Thailand

- 5.3.1.7 Vietnam

- 5.3.1.8 Malaysia

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Nordic Countries

- 5.3.3.8 Turkey

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Biofriends Inc.

- 6.4.2 DME-Aerosol LLC

- 6.4.3 Dongguan Jovo Warehousing Services Co., Ltd.

- 6.4.4 GRILLO-Werke AG

- 6.4.5 Gruppo SIAD

- 6.4.6 Korea Gas Corporation

- 6.4.7 Mitsubishi Gas Chemical Company, Inc.

- 6.4.8 Nouryon

- 6.4.9 Oberon Fuels, Inc.

- 6.4.10 Shell PLC

- 6.4.11 Sichuan Lutianhua Co., Ltd.

- 6.4.12 The Chemours Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment