PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937345

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937345

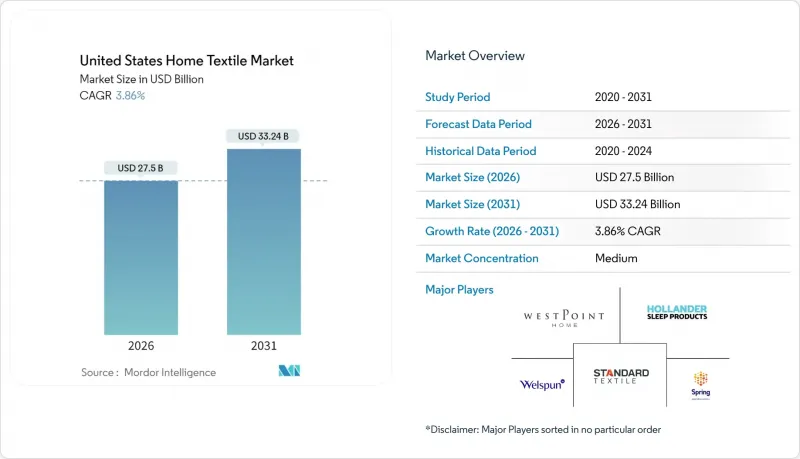

United States Home Textile - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States home textile market size in 2026 is estimated at USD 27.5 billion, growing from 2025 value of USD 26.48 billion with 2031 projections showing USD 33.24 billion, growing at 3.86% CAGR over 2026-2031.

Demand is shifting from pure volume to higher-value products that satisfy sustainability credentials, omnichannel convenience, and technology-enabled comfort. Home-renovation spending of USD 567.0 billion in 2022 serves as a durable engine for premium bed and bath replacements. A 52% jump in MADE IN GREEN labels, the first U.S. textile recycling mandate under California's SB 707, and mounting consumer interest in PFAS-free finishes elevate the role of traceability across the value chain. Regionally, the Southeast maintains cost-advantaged production clusters, while the West records the fastest growth due to tech-sector wealth and eco-oriented shoppers. Competitive intensity is moderate because scale incumbents still dominate mass channels even as direct-to-consumer innovators siphon premium share.

United States Home Textile Market Trends and Insights

Rising Home-Renovation Spend

Home renovation expenditure creates a multiplier effect for textile demand that extends beyond simple replacement cycles. Harvard's Joint Center for Housing Studies documented USD 567.0 billion in improvement spending for 2022, with energy-related envelope projects accounting for USD 111.0 billion. This spending pattern favors premium textile categories as homeowners increasingly view bedding and window treatments as integral design elements rather than commodity purchases. Houzz's 2025 survey revealed 54% of homeowners undertook renovation projects in 2024, with median spending on small bathroom remodels rising 13% to USD 17,000.0, indicating sustained discretionary spending power that benefits higher-margin textile segments. The trend toward luxury renovation spending, with high-end kitchen projects starting at USD 150,000.0, creates downstream demand for coordinated textile collections that can command premium pricing.

E-commerce Penetration Surge

Digital channel expansion reshapes both consumer behavior and supply chain dynamics in ways that favor agile, direct-to-consumer brands over traditional wholesale models. The National Retail Federation projects non-store sales growing 7-9% to USD 1.57-1.60 trillion in 2025, with home goods categories experiencing above-average digital adoption. This shift enables smaller textile brands to bypass traditional retail gatekeepers while providing established players with direct customer relationships and higher margins. Target's strategic expansion of its third-party marketplace from USD 1.0 billion in 2024 to over USD 5.0 billion by 2030 exemplifies how major retailers are adapting to accommodate both established brands and emerging direct-to-consumer players. The acceleration of same-day delivery services and store-as-fulfillment-hub strategies reduces the traditional advantage of local inventory positioning, creating opportunities for specialized textile brands to compete nationally without extensive distribution infrastructure.

Inflation-Driven Consumer Down-Trading to Budget SKUs

Persistent inflation pressures force consumer segmentation strategies that prioritize value positioning over premium features, creating margin compression across mid-tier product categories. The National Retail Federation's 2025 forecast anticipates PCE price index inflation at 2.5%, with tariff policies contributing additional cost pressures that retailers struggle to absorb. Newell Brands reported an estimated USD 155.0 million incremental tariff cost impact for 2025, with USD 105.0 million affecting gross profit margins, demonstrating how trade policy translates directly into consumer pricing pressures. This environment favors retailers with strong private-label capabilities and efficient supply chains, while pressuring specialty brands that lack scale economies. Sleep Number's 11% revenue decline in 2024, despite improved gross margins, illustrates how premium positioning becomes vulnerable when consumers prioritize affordability over advanced features.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability & Organic Demand

- Hospitality Sector Rebound

- Rising Logistics & Container Costs Squeezing Importer Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bed linen's commanding 42.15% market share in 2025 reflects consumer prioritization of sleep quality and bedroom aesthetics, yet upholstery's 5.31% CAGR through 2031 signals shifting demand toward living space enhancement and commercial applications. The hospitality sector's recovery drives significant upholstery demand as hotels and restaurants reinvest in interior upgrades, while residential consumers increasingly view furniture textiles as design statements rather than functional necessities. Bath linen maintains steady demand through replacement cycles and premium positioning, with antimicrobial treatments gaining adoption in healthcare and hospitality applications. Kitchen linen experiences modest growth as open-plan living designs integrate kitchen textiles into broader home aesthetics, while carpets and area rugs benefit from renewed interest in comfort and acoustic management in home offices.

Culp Inc.'s 2024 annual report revealed mattress fabrics generating USD 116.4 million (52% of sales) with 4.8% growth, while upholstery fabrics declined 12.1% to USD 108.9 million, illustrating the divergent performance within application categories. The company's emphasis on performance fabrics, which account for 40% of upholstery sales through its LiveSmart stain-resistant technology, demonstrates how innovation drives premium positioning within traditional categories. OEKO-TEX STANDARD 100 certification requirements increasingly influence purchasing decisions across all application segments, with over 43,000 labels issued globally in 2024, reflecting growing consumer awareness of chemical safety in textile products.

Cotton's 65.90% market share in 2025 demonstrates enduring consumer preference for natural fiber performance and versatility, while linen's accelerating 5.63% CAGR reflects premium positioning strategies and sustainability messaging that resonate with affluent demographics. Synthetic fibers maintain cost advantages in commercial applications and performance-specific uses, though they face increasing scrutiny over microplastic environmental impacts. The "Other Materials" category, encompassing wool, hemp, silk, jute, and bamboo, experiences growth through niche positioning and sustainability credentials, particularly in premium bedding and eco-conscious consumer segments.

Cotton Incorporated's 2025 supply chain analysis highlights ongoing challenges, including input cost volatility and sustainability requirements that affect pricing throughout the value chain. The organization's emphasis on traceability and reduced environmental impact aligns with retailer requirements for supply chain transparency, particularly following the implementation of the Uyghur Forced Labor Prevention Act enforcement. Eastman's Naia Renew fiber technology, incorporating 60% sustainably sourced wood pulp and 40% recycled waste through molecular recycling, exemplifies innovation in sustainable fiber development that challenges traditional cotton dominance. Microban International's H2O Shield PFAS-free water-resistant portfolio, launched in 2025, addresses growing regulatory restrictions on chemical treatments while maintaining performance standards across fiber types.

The United States Home Textile Market Report is Segmented by Application (Bed Linen, Bath Linen, Kitchen Linen, Upholstery, Carpets & Area Rugs), Material (Cotton, Linen, Synthetic Fibres, Other Materials), End-User (Residential, Commercial), Distribution Channel (B2C/Retail Channels, B2B/Direct), and Geography (Northeast, Midwest, Southeast, Southwest, West). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- WestPoint Home

- Springs Global (Springmaid)

- Hollander Sleep Products

- Standard Textile

- Welspun

- Berkshire Hathaway's Burlington

- Sunham Home Fashions

- Trident Group

- Brooklinen

- Parachute Home

- Boll & Branch

- Coyuchi

- Crane & Canopy

- Bed Bath & Beyond (Private Label)

- 1888 Mills

- Ralph Lauren

- Shaw Industries

- Ikea US

- Maples Industries

- Anthropologie (AnthroLiving)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Table of Contents - United States Home Textile Market

2 Introduction

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

3 Research Methodology

4 Executive Summary

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Rising home-renovation spend

- 5.2.2 E-commerce penetration surge

- 5.2.3 Sustainability & organic demand

- 5.2.4 Hospitality sector rebound

- 5.2.5 Antimicrobial fabric adoption

- 5.2.6 Smart-textile integration in bedding

- 5.3 Market Restraints

- 5.3.1 Inflation-driven consumer down-trading to budget SKUs

- 5.3.2 Rising logistics & container costs squeezing importer margins

- 5.3.3 Subscription-based linen rental models cutting replacement cycles

- 5.3.4 Retail traceability audits triggering delistings for non-compliant mills

- 5.4 Industry Value Chain Analysis

- 5.5 Porter's Five Forces Analysis

- 5.5.1 Threat of New Entrants

- 5.5.2 Bargaining Power of Suppliers

- 5.5.3 Bargaining Power of Buyers

- 5.5.4 Threat of Substitutes

- 5.5.5 Competitive Rivalry

- 5.6 Insights into the Latest Trends and Innovations in the Market

- 5.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

6 Market Size & Growth Forecasts (Value in USD)

- 6.1 By Application

- 6.1.1 Bed Linen

- 6.1.2 Bath Linen

- 6.1.3 Kitchen Linen

- 6.1.4 Upholstery

- 6.1.5 Carpets & Area Rugs

- 6.2 By Material

- 6.2.1 Cotton

- 6.2.2 Linen

- 6.2.3 Synthetic Fibres

- 6.2.4 Other Materials (Wool, Hemp, Silk, Jute, Bamboo)

- 6.3 By End-User

- 6.3.1 Residential

- 6.3.2 Commercial

- 6.4 By Distribution Channel

- 6.4.1 B2C/Retail Channels

- 6.4.1.1 Mass Merchandisers (Hypermarkets/Supermarkets)

- 6.4.1.2 Home Centers

- 6.4.1.3 Specialty Stores

- 6.4.1.4 Local Mom and Pop Stores

- 6.4.1.5 Online

- 6.4.1.6 Other Distribution Channels

- 6.4.2 B2B/Direct from the Manufacturers

- 6.4.1 B2C/Retail Channels

- 6.5 By Region

- 6.5.1 Northeast

- 6.5.2 Midwest

- 6.5.3 Southeast

- 6.5.4 Southwest

- 6.5.5 West

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 7.4.1 WestPoint Home

- 7.4.2 Springs Global (Springmaid)

- 7.4.3 Hollander Sleep Products

- 7.4.4 Standard Textile

- 7.4.5 Welspun

- 7.4.6 Berkshire Hathaway's Burlington

- 7.4.7 Sunham Home Fashions

- 7.4.8 Trident Group

- 7.4.9 Brooklinen

- 7.4.10 Parachute Home

- 7.4.11 Boll & Branch

- 7.4.12 Coyuchi

- 7.4.13 Crane & Canopy

- 7.4.14 Bed Bath & Beyond (Private Label)

- 7.4.15 1888 Mills

- 7.4.16 Ralph Lauren

- 7.4.17 Shaw Industries

- 7.4.18 Ikea US

- 7.4.19 Maples Industries

- 7.4.20 Anthropologie (AnthroLiving)

8 Market Opportunities & Future Outlook

- 8.1 Sustainable Materials Adoption in Premium Bedding

- 8.2 Tech-Integrated Smart Textiles for Home Comfort