PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937365

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937365

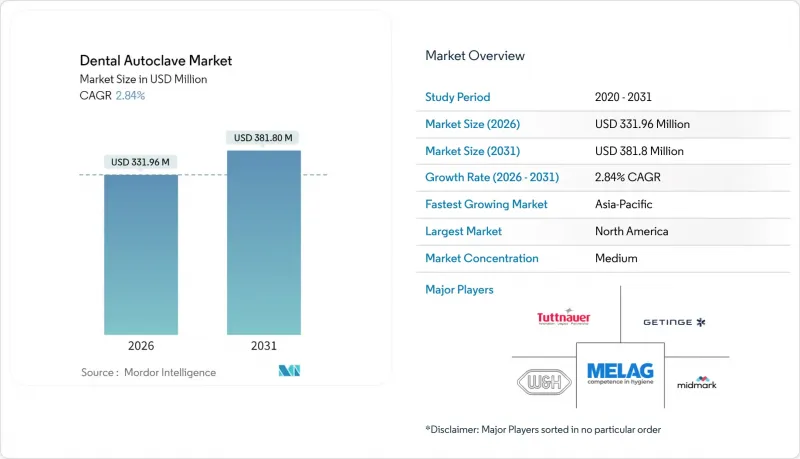

Dental Autoclave - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The dental autoclave market is expected to grow from USD 322.79 million in 2025 to USD 331.96 million in 2026 and is forecast to reach USD 381.8 million by 2031 at 2.84% CAGR over 2026-2031.

Measured expansion reflects enduring demand created by infection-control mandates, a widening installed base, and the steady replacement of legacy sterilizers with connected Class B systems. Equipment standardization by dental service organizations (DSOs) amplifies purchasing power, allowing vendors that bundle after-sales service and consumables to protect margins despite price pressure. Digital traceability, energy-efficient cycles, and instrument-specific presets are emerging as differentiators that influence capital procurement cycles. Competitive intensity remains moderate because proprietary firmware and validation documentation create switching costs that smaller regional rivals struggle to match. Portable models now attract sustained interest from mobile clinics, humanitarian missions, and disaster-response units, opening niche revenue streams for manufacturers that can ruggedize Class B performance in compact footprints.

Global Dental Autoclave Market Trends and Insights

Rising Incidences of Dental Disorders and Cosmetic Dentistry

Rapid population aging and widespread aesthetic awareness continue to lift procedure volumes across implants, clear aligners, and full-arch restorations. Each of these interventions requires validated sterilization of handpieces, torque wrenches, and implant drivers at multiple stages, resulting in higher daily cycle counts for practices. A single aligner practice that manages 20 new cases a week may run up to 40 additional sterilization cycles to comply with instrument turnover protocols. The demand surge aligns with heightened patient expectations for documented sterilization, prompting clinics to upgrade to Class B autoclaves that can handle hollow instruments and complex geometries reliably. Device makers bundle biological indicator starter kits and sterility assurance services, allowing operators to meet audit requirements without internal microbiology facilities. The convergence of procedural complexity and case volume sustains long-term growth for the dental autoclave market.

Stricter Global Infection-Control Regulations

The U.S. Centers for Disease Control and Prevention updated its sterilization monitoring guide in 2024 to emphasize weekly biological indicators, chemical integrators, and digital record retention, pushing clinics toward units with integrated printers or cloud connectivity. The European Committee for Standardization reaffirmed EN 13060 compliance for dental benchtop sterilizers, reinforcing Class B performance requirements across the region. Simultaneously, the FDA classified vapor hydrogen peroxide (VHP) as a Category A method but underscored steam autoclave superiority for reusable handpieces, indirectly validating steam sterilization's central role. These rules heighten liability risk, making automatic cycle documentation a key buying criterion for DSOs. Manufacturers now preload predefined protocol packages in firmware, speeding installation and standardizing reporting across multi-site networks.

High Upfront and Maintenance Cost for Small Practices

A mid-range Class B autoclave typically lists between USD 4,000 and USD 10,000, a figure that can equal two months of chairside gross production for many single-chair offices. Annual preventive-maintenance contracts add USD 440-699 in recurring expense, exclusive of consumables such as biological indicators. Energy costs have risen by 12% since 2023 in several regions, further increasing ownership cost. Although manufacturers promote lease-to-own schemes with residual buyouts, the total lifetime cost still biases small operators toward delaying upgrades until existing units fail a spore test. The resulting elongation of replacement cycles tempers near-term revenue upside for vendors even as DSOs continue bulk purchases.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption Of Class B Vacuum Autoclaves

- Digital And IoT-Enabled Autoclaves For Traceability

- Competition From Low-Temperature Or Chemical Sterilizers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automatic units accounted for 42.85% of 2025 revenue, underpinned by touch-panel controls, auto-locking doors, and cycle presets that reduce human error. DSOs with standardized clinical pathways adopt automatic autoclaves to harmonize workflows across hundreds of sites, minimizing variance in sterility assurance. Manual and semi-automatic models maintain footholds in developing economies where purchase price dominates decision criteria, yet rising infection-control awareness in these regions nudges upgrades. Manufacturers layer value by bundling electronic record systems and on-site training, ensuring rapid staff onboarding. As practices move toward single-visit restorative workflows, the need for fast cycle turnaround further strengthens automatic adoption. Service analytics show 15% fewer post-warranty failures in automatic lines, enhancing total cost-of-ownership appeal. Consequently, the dental autoclave market registers a gradual but persistent shift toward full automation in its installed base.

Automatic systems are projected to grow at 5.08% CAGR through 2031, outpacing overall market expansion. Standardization of user interfaces reduces staff retraining costs during acquisitions, a factor DSOs cite when negotiating master purchase agreements. Manufacturers differentiate through cycle speed, water-quality monitoring, and self-diagnostics that issue maintenance alerts, safeguarding uptime for high-volume clinics. Semi-automatic models now integrate limited connectivity, yet absence of automatic door actuators and load-detection sensors caps their premium positioning. Manual units remain relegated to backup roles or budget-limited rural practices, where vendor refurbished stock offers a low-entry pathway. Across all price tiers, warranty length and local service presence influence buying decisions more than feature sets, underscoring post-sale support as a competitive lever in the dental autoclave market.

Class B autoclaves captured 42.18% dental autoclave market share in 2025, reflecting widespread acknowledgement of their superiority for lumened and porous loads. Validated performance against prion contamination secures adoption in oral-surgery centers that handle bone graft kits. European standards compel new installations to meet Class B criteria, creating natural replacement demand. Class N gravity units dominate basic check-up clinics, especially in countries where insurance reimbursement remains low, fostering an entry-level tier. Class S machines split the difference by offering single vacuum pulses, serving orthodontic labs that process mostly plastic aligner molds.

The dental autoclave market size for Class B models is forecast to rise steadily as North American states update dental-board rules to recommend pre-vacuum sterilization for handpieces. Vendors respond with compact Class B chambers that fit into cabinetry built for legacy gravity units, easing upgrade barriers. Meanwhile, Class N units benefit from retrofitted energy-saving heaters and improved water separation, narrowing utility-cost gaps. Nonetheless, rising complexity of implant instrumentation tips emerging-market clinicians toward vacuum technology despite cost sensitivity. Overall, technology segmentation will continue to hinge on regulatory alignment and instrument mix rather than raw price alone.

The Dental Autoclave Market Report is Segmented by Product Type (Semi-Automatic, Automatic, and Manual), Technology/Class (Class B Vacuum, Class N Non-Vacuum, and Class S Single-Cycle), Modality (Table-top/Bench-top, and Portable/Mobile), Capacity (< 10 L, and More), End User (Hospitals & Multispecialty Clinics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 41.88% of 2025 revenue, buoyed by stringent CDC mandates that compel routine biological monitoring and documentation. DSOs now account for more than one quarter of U.S. practices, creating consolidated procurement structures that favor vendors offering national service fleets. Canadian provincial regulators mirror U.S. guidance, sustaining demand for Class B upgrades even among single-chair clinics. Despite mature penetration, replacement demand remains healthy as offices retire gravity units purchased pre-2016.

Asia-Pacific is projected to record a 4.47% CAGR through 2031, the fastest among all regions, propelled by dental tourism, expanding insurance coverage, and rising infection-control awareness. Thailand and India invest heavily in private hospital infrastructure to attract foreign patients, leading to procurement of internationally certified Class B units. China's medical device watchdog approved 133 dental devices in early 2024, reflecting a maturing regulatory environment that values validated sterilization. Manufacturers that localize after-sales support in Southeast Asia gain an advantage as language and logistics barriers recede.

Europe maintains steady demand due to EN 13060 mandates that require Class B performance for new installations. Sustainability targets drive interest in energy-efficient cycles, with some clinics integrating heat-recovery systems. Latin America experiences moderate expansion as Brazil's private insurance sector grows, though currency volatility influences purchasing timing. The Middle East and Africa represent emerging opportunities tied to public-sector investments in oral-health programs. Overall, regional dynamics underscore the global reach of the dental autoclave market while highlighting nuanced regulatory and economic drivers that vendors must navigate.

List of Companies Covered in this Report:

- 3M

- Astell Scientific

- Belimed

- Coltene Holding

- Dentsply Sirona

- Euronda

- Flight Dental Systems

- Getinge

- Matachana Group

- MELAG Medizintechnik

- Midmark

- Mocom

- NSK Ltd.

- Runyes Medical

- SciCan Ltd.

- Shinva Medical Instrument

- STERIS

- TECNO-GAZ

- Tuttnauer

- W&H Dentalwerk

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidences of Dental Disorders & Cosmetic Dentistry

- 4.2.2 Stricter Global Infection-Control Regulations

- 4.2.3 Growing Adoption of Class B Vacuum Autoclaves

- 4.2.4 Digital & Iot-Enabled Autoclaves for Traceability

- 4.2.5 Emerging Dental Tourism Hubs Driving Equipment Demand

- 4.2.6 ESG Focus on Energy-Efficient Sterilization Solutions

- 4.3 Market Restraints

- 4.3.1 High Upfront & Maintenance Cost for Small Practices

- 4.3.2 Low Hygiene Awareness in Parts of Africa & South Asia

- 4.3.3 Fragmented Regulatory Standards Across Countries

- 4.3.4 Competition From Low-Temperature/Chemical Sterilizers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Buyer Bargaining Power

- 4.7.2 Supplier Bargaining Power

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Semi-Automatic

- 5.1.2 Automatic

- 5.1.3 Manual

- 5.2 By Technology / Class

- 5.2.1 Class B (Vacuum)

- 5.2.2 Class N (Non-Vacuum)

- 5.2.3 Class S (Single-Cycle)

- 5.3 By Modality

- 5.3.1 Table-top / Bench-top

- 5.3.2 Portable / Mobile

- 5.4 By Capacity (Chamber Volume)

- 5.4.1 <10 L

- 5.4.2 10-20 L

- 5.4.3 20-40 L

- 5.4.4 >40 L

- 5.5 By End User

- 5.5.1 Hospitals & Multispecialty Clinics

- 5.5.2 Dental Laboratories

- 5.5.3 Academic & Research Institutes

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 3M Company

- 6.3.2 Astell Scientific

- 6.3.3 Belimed AG

- 6.3.4 Coltene Holding

- 6.3.5 Dentsply Sirona

- 6.3.6 Euronda

- 6.3.7 Flight Dental Systems

- 6.3.8 Getinge AB

- 6.3.9 Matachana Group

- 6.3.10 MELAG Medizintechnik GmbH & Co. KG

- 6.3.11 Midmark Corp.

- 6.3.12 Mocom

- 6.3.13 NSK Ltd.

- 6.3.14 Runyes Medical

- 6.3.15 SciCan Ltd.

- 6.3.16 Shinva Medical Instrument Co. Ltd

- 6.3.17 STERIS plc

- 6.3.18 TECNO-GAZ

- 6.3.19 Tuttnauer

- 6.3.20 W&H Dentalwerk

7 Market Opportunities & Future Outlook