PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937366

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937366

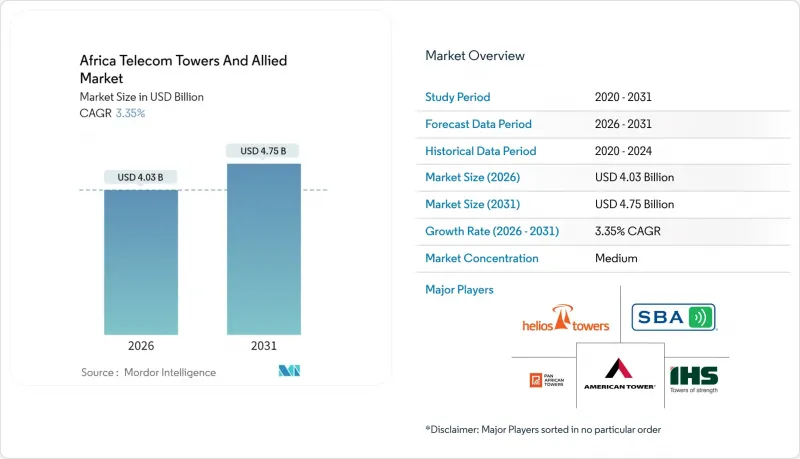

Africa Telecom Towers And Allied - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Africa Telecom Towers And Allied Market size in 2026 is estimated at USD 4.03 billion, growing from 2025 value of USD 3.9 billion with 2031 projections showing USD 4.75 billion, growing at 3.35% CAGR over 2026-2031.

Accelerated 4G and newly launched 5G rollouts, rising data consumption, and government-backed rural coverage mandates underpin this steady expansion. Independent TowerCos continue to win large multi-year outsourcing contracts from pan-African mobile network operators, a trend that lifts tenancy ratios and improves operating cash flows. Renewable-powered systems are gaining momentum as green financing incentives offset the volatility of diesel fuel costs. Meanwhile, country-specific programs, such as Algeria's fiber-to-the-home build-out and Kenya's digital-economy blueprint, add geographic depth to overall demand for ground-based and rooftop sites across the Africa telecom tower market.

Africa Telecom Towers And Allied Market Trends and Insights

Accelerated 4G/5G rollout by pan-African MNOs

Pan-African mobile network operators added hundreds of 5G sites in 2024 and early 2025, lifting total 5G subscriptions in Sub-Saharan Africa toward Ericsson's 420 million projection for 2030 . MTN Group alone expanded its 5G footprint to more than 3,000 sites, prompting a surge in colocation requests across the Africa telecom tower market . The densification imperative is especially acute in Lagos, Nairobi, and Johannesburg, where 5G mid-band spectrum requires closer site spacing. Independent TowerCos capitalize on this urgency by offering turnkey build-to-suit programs that shorten time-to-market for operators migrating from legacy 4G networks. The momentum is reinforced by the recent commercial 5G launch in Tunisia, underscoring the broad regional commitment to next-generation connectivity .

Rising data consumption and smartphone penetration

Video streaming, social media, and mobile payments are elevating per-subscriber data use into double-digit gigabyte ranges across North and West Africa. Young demographics and low-cost smartphone imports sustain this demand curve, compelling operators to add capacity faster than originally budgeted. Higher data volumes translate into larger leaseable antenna counts per site, pushing tenancy ratios across the Africa telecom tower market from 1.5x toward 2x in core metros. TowerCos are therefore incentivized to future-proof structures with stronger load capacities and fiber-ready backhaul, ensuring revenue upside as data-heavy services proliferate.

Volatile foreign-exchange and high sovereign risk

Revenue is largely denominated in local currencies, but debt and capex remain USD-linked, exposing TowerCos to material conversion losses during currency depreciations. IHS Towers reported notable FX headwinds in several African markets during 2024, underscoring sensitivity to macroeconomic cycles. Sovereign credit downgrades trigger higher interest rates that can render new builds unviable or slow refinancing efforts. Operators and TowerCos are increasingly exploring natural hedges such as USD-indexed lease escalators, but uptake remains limited by regulatory caps on foreign-currency billing.

Other drivers and restraints analyzed in the detailed report include:

- Government-led rural coverage mandates and universal service funds

- Asset-light network strategies by MNOs boosting tower outsourcing

- Lengthy permitting and land-acquisition bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Independent TowerCos commanded 45.18% of the Africa telecom tower market share in 2025 and are on track for a 6.53% CAGR through 2031. The superior returns stem from 92.4% utilization rates and diversified country portfolios that smooth FX and regulatory risk. Operator-owned assets persist in markets with infrastructure-sharing constraints, but monetization pressure is rising as balance-sheet light strategies take hold. The Africa telecom tower market size for Independent TowerCos could exceed USD 2.07 billion in annual lease revenue by 2031 if current divestiture pipelines close on schedule.

MNO captive sites remain critical in politically sensitive geographies where network control is paramount; however, cash-strapped operators increasingly favor sale-leasebacks to fund 5G spectrum fees. Joint-venture TowerCos offer a middle path, letting rivals co-invest in passive plant without sacrificing active-layer differentiation. American Tower's selective entry strategy validates the margin advantage enjoyed by global specialists in complex metros, a dynamic likely to accelerate consolidation across the Africa telecom tower industry.

Ground-based towers held 76.20% of the Africa telecom tower market size in 2025, proving cost-effective for suburban and rural macro coverage. Rooftop installations, though smaller in absolute footprint, are gaining a 7.34% CAGR as 5G mid-band frequencies demand tighter grid spacing in densely populated business districts. Municipal aesthetic guidelines and mounting land prices make rooftops the only viable option in central Nairobi, Casablanca, and Johannesburg.

Ground-based towers still deliver higher absolute revenue per site thanks to greater antenna load capacity and ease of renewable-power retrofits. Yet rooftops promise faster permitting and reduced civil works expenditure, allowing TowerCos to capture incremental revenue within established coverage zones. This nuanced mix of site types ensures the Africa telecom tower market remains flexible as data-traffic patterns evolve.

The Africa Telecom Towers and Allied Market Report is Segmented by Ownership (Operator-Owned, Independent TowerCo, and More), Installation (Rooftop, Ground-Based), Fuel Type (Renewable-Powered, Grid/Diesel Hybrid), Tower Type (Monopole, Lattice, Guyed, Stealth/Concealed), and Country. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Installed Base).

List of Companies Covered in this Report:

- TowerCos

- Mobile Network Operator

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Taxonomy

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

- 3.1 Telecom Tower Volume Estimates (Units, 2023-2030)

- 3.2 Telecom Tower Leasing Revenue Estimates (USD, 2023-2030)

- 3.3 Telecom Tower Construction Revenue Estimates (USD, 2023-2030)

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated 4G/5G rollout by pan-African MNOs

- 4.2.2 Rising data consumption and smartphone penetration

- 4.2.3 Government-led rural coverage mandates and universal service funds

- 4.2.4 Asset-light network strategies by MNOs boosting tower outsourcing

- 4.2.5 Green financing incentives for renewable power retrofits

- 4.2.6 Expansion of neutral-host indoor DAS and small-cell backhaul demand

- 4.3 Market Restraints

- 4.3.1 Volatile foreign-exchange and high sovereign risk

- 4.3.2 Lengthy permitting and land-acquisition bottlenecks

- 4.3.3 Diesel supply disruptions raising opex at off-grid sites

- 4.3.4 Fiber backhaul deficits limiting tenancy ratios in secondary cities

- 4.4 Ecosystem Analysis

- 4.5 Regulatory Landscape Related to Telecom Infrastructure

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Ownership

- 5.1.1 Operator-owned

- 5.1.2 Independent TowerCo

- 5.1.3 Joint-Venture TowerCo

- 5.1.4 MNO Captive

- 5.2 By Installation

- 5.2.1 Rooftop

- 5.2.2 Ground-based

- 5.3 By Fuel Type

- 5.3.1 Renewable-powered

- 5.3.2 Grid/Diesel Hybrid

- 5.4 By Tower Type

- 5.4.1 Monopole

- 5.4.2 Lattice

- 5.4.3 Guyed

- 5.4.4 Stealth / Concealed

- 5.5 By Country

- 5.5.1 Algeria

- 5.5.2 Kenya

- 5.5.3 Morocco

- 5.5.4 South Africa

- 5.5.5 Nigeria

- 5.5.6 Ghana

- 5.5.7 Egypt

- 5.5.8 Tanzania

- 5.5.9 Rest of Africa (Tunisia, Uganda, Zambia, Senegal, and Others)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Details of Major Mergers and Acquisitions

- 6.3 Market Share Analysis for top vendors

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 TowerCos

- 6.4.1.1 American Tower Corporation

- 6.4.1.2 IHS Towers (IHS Holding Limited)

- 6.4.1.3 Helios Towers Plc

- 6.4.1.4 SBA Communications Corporation

- 6.4.1.5 Pan African Towers

- 6.4.1.6 Atlas Tower Group Limited

- 6.4.1.7 Eastcastle Infrastructure

- 6.4.1.8 Paradigm Infrastructure Limited

- 6.4.1.9 Hotspot Network Ltd

- 6.4.2 Mobile Network Operator

- 6.4.2.1 MTN Group

- 6.4.2.2 Vodacom Group

- 6.4.2.3 Airtel Africa plc

- 6.4.2.4 Orange Middle East and Africa

- 6.4.2.5 e& misr company

- 6.4.2.6 Safaricom PLC

- 6.4.2.7 Telkom SA SOC Limited

- 6.4.2.8 Globacom Limited (Glo)

- 6.4.2.9 Maroc Telecom SA

- 6.4.2.10 WE (Telecom Egypt)

- 6.4.2.11 Unitel Angola (Unitel SA)

- 6.4.2.12 Econet Wireless Zimbabwe Ltd.

- 6.4.2.13 Ethio Telecom

- 6.4.2.14 Movitel Mozambique (Movitel S.A.)

- 6.4.2.15 Moov Africa

- 6.4.2.16 Sonatel Senegal (Sonatel SA)

- 6.4.2.17 Yas Madagascar

- 6.4.1 TowerCos

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

- 7.2 Investment Analysis

- 7.3 Analyst Suggestions and Recommendations