PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939122

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939122

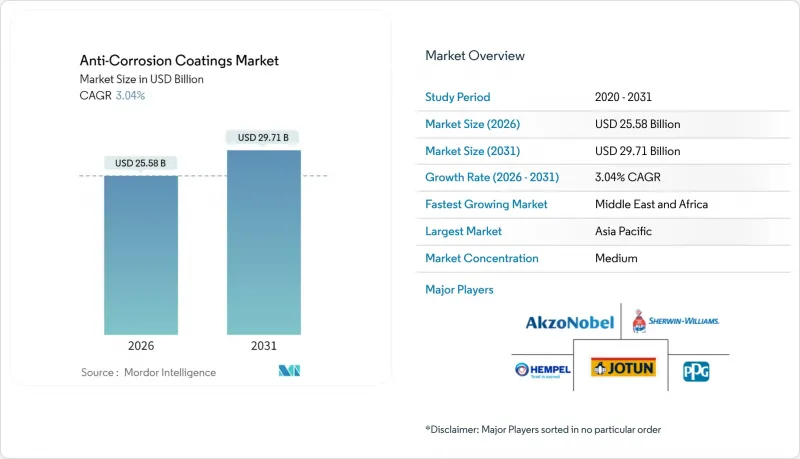

Anti-Corrosion Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Anti-Corrosion Coatings Market is expected to grow from USD 24.82 billion in 2025 to USD 25.58 billion in 2026 and is forecast to reach USD 29.71 billion by 2031 at 3.04% CAGR over 2026-2031.

Strong public-sector infrastructure spending, more demanding offshore wind specifications, and the expanding refurbishment cycle for floating production storage offloading (FPSO) vessels are shifting the anti-corrosion coatings market from a volume-led arena to a performance-driven ecosystem. Water-borne chemistries are advancing in regulatory-sensitive regions, yet solvent-borne systems still dominate where failure risk outweighs environmental trade-offs. Resin innovation is also accelerating, with bio-based epoxies and hybrid polyurethane systems gaining traction in bids that score sustainability alongside lifetime durability. Greater demand for corrosion-under-insulation solutions at LNG terminals highlights the market's transition from generalized maintenance paints toward application-specific engineered coatings.

Global Anti-Corrosion Coatings Market Trends and Insights

Infrastructure Renewal Super-cycle in U.S., EU and Japan

Massive government programs are steering demand toward high-performance coatings that extend service life well beyond conventional maintenance cycles. The Infrastructure Investment and Jobs Act in the United States earmarked USD 550 billion for upgrades that prioritize long-life bridge, rail, and port assets. European Green Deal allocations link funding to low-VOC, high-durability products, nudging specifiers toward bio-based epoxy and hybrid polyurethane systems. Japan's national resilience plan requires flexible, seismic-resistant finishes for tunnels and coastal defenses, propelling research into tougher polyurethane elastomer chemistries. The combined effect is a steady replacement of basic alkyd films with engineered systems offering 25-30-year protection intervals. Suppliers capable of lifecycle assurance and rapid on-site technical support are capturing premium margins as owners view coatings as strategic risk mitigators rather than consumables.

Offshore Wind Farm Coating Demand Surge

Global offshore wind capacity is targeted to exceed 380 GW by 2030, driving specialized needs for monopile, transition-piece, and nacelle protection. Turbine components demand coatings that withstand cyclical salt spray, impact from floating debris, and cathodic disbondment. Nano-ceramic-reinforced epoxy primers topped with aliphatic polyurethane finishes are emerging as a standard stack because they retain gloss and barrier integrity for 25-year service windows. U.S. East Coast projects, galvanized by a federal roadmap for 30 GW of installations, are specifying water-borne or high-solids variants to honor strict VOC caps without compromising performance. Asian yards fabricating turbine jackets are fast-tracking qualification of similar systems to stay compliant with European developer tenders, tightening global raw-material supply chains for specialty anticorrosive pigments.

Tightening Global VOC Caps and Isocyanate Exposure Limits

Revised limits of 50 g/L VOC in several U.S. and EU districts are squeezing solvent-borne polyurethane sales. Manufacturers must invest in water-borne or high-solids upgrades, often accepting slower cure times and stricter humidity controls on job sites. The added training, equipment adaptation, and third-party certification expenses erode margins while the performance gap relative to legacy solvent technologies still worries marine and heavy-industrial users. In parallel, new REACH rules on di-isocyanate labeling raise logistical hurdles for shipping two-pack polyurethanes across borders, extending lead times in critical maintenance windows.

Other drivers and restraints analyzed in the detailed report include:

- Growing FPSO Refurbishments in Latin America and West Africa

- Corrosion-under-insulation Failures in LNG Terminals

- High Capex for Nano-ceramic Dispersion Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy systems accounted for 38.92% of the anti-corrosion coatings market size in 2025, thanks to unmatched adhesion and chemical resistance, especially in marine ballast tanks and bridge girders. Recent bio-based epoxy variants satisfy green-procurement scoring without sacrificing salt-spray hours, pulling share from conventional bis-A formulations. The segment remains resilient despite raw-material cost swings, as formulators lean on diluent optimization to keep delivered prices stable.

Polyurethane volumes are expanding fastest, supported by a 3.79% CAGR as developers choose flexible films that absorb vibration and resist mechanical chipping on offshore wind towers. Growing polyurethane acceptance in seismic-prone Asian transport tunnels further narrows the gap to epoxy. Alkyd, polyester, and vinyl ester niches maintain relevance where cost sensitivity or extreme chemical resistance dictates, but hybrid technology blending epoxy primers with polyurethane topcoats now dominates specification sheets for long-life steel infrastructure.

The Anti-Corrosion Coatings Report is Segmented by Resin Type (Epoxy, Alkyds, Polyester, Polyurethane, and More), Technology (Water-Borne, Solvent-Borne, Powder, and UV-Cured), End-User Industry (Oil and Gas, Marine, Power, Infrastructure, Industrial, Aerospace and Defense, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 46.60% of 2025 revenue, driven by China's Belt and Road port expansions, India's offshore wind farm orders, and Japan's seismic infrastructure initiatives. Domestic manufacturers benefit from integrated resin production hubs that compress lead times and reduce currency risk, yet rising local environmental rules are pushing waterborne adoption in coastal provinces. Southeast Asian shipyards, eager to win EU-flag vessel contracts, are aligning with IMO PSPC-approved coating systems, adding further pull for global premium brands.

North America's share remains sizeable owing to the Infrastructure Investment and Jobs Act pipeline of bridge and tunnel rehabilitation, combined with elevated maintenance spending on U.S. Gulf Coast petrochemical plants. Specifiers are pivoting toward high-solids epoxies with rapid return-to-service properties to minimize lane-closure durations on busy interstates.

Europe hosts a sophisticated market where Green Deal subsidies tie funding to low-VOC, bio-based, or recycled-content coatings. Ship repair yards in the North Sea embrace advanced zinc-silicate primers compatible with fast-flush solvent-free topcoats to rebalance stricter health regulations.

The Middle East and Africa is projected to rise at a3.36% CAGR through 2031 due to mega-projects such as Saudi Arabia's NEOM and Nigeria's offshore hubs. High UV levels, sand abrasion, and salinity demand premium fluoropolymer topcoats paired with glass-flake epoxies, positioning technical superiority over price as the chief contract award criterion. Rising refinery capacity in Oman and Qatar fuels steady demand for CUI-resistant linings across kilometers of insulated piping.

- Akzo Nobel N.V.

- Axalta Coating Systems, LLC

- BASF

- Beckers Group

- Berger Paints India

- Carboline

- Chugoku Marine Paints, Ltd.

- H.B. Fuller Company

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- Teknos Group

- The Sherwin-Williams Company

- Tikkurila

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure renewal super-cycle in U.S., EU and Japan

- 4.2.2 Offshore wind farm coating demand surge

- 4.2.3 Growing FPSO refurbishments in Latin America and West Africa

- 4.2.4 Corrosion-under-insulation (CUI) failures in LNG terminals

- 4.2.5 Bio-based resin innovations securing "green procurement" bids

- 4.3 Market Restraints

- 4.3.1 Tightening global VOC caps and isocyanate exposure limits

- 4.3.2 High capex for nano-ceramic dispersion lines

- 4.3.3 Volatility in epoxy raw material prices (bis-A, ECH)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Alkyds

- 5.1.3 Polyester

- 5.1.4 Polyurethane

- 5.1.5 Vinyl Ester

- 5.1.6 Other Resin Types

- 5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Powder

- 5.2.4 UV-cured

- 5.3 By End-user Industry

- 5.3.1 Oil and Gas

- 5.3.2 Marine

- 5.3.3 Power

- 5.3.4 Infrastructure

- 5.3.5 Industrial

- 5.3.6 Aerospace and Defense

- 5.3.7 Transportation

- 5.3.8 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Axalta Coating Systems, LLC

- 6.4.3 BASF

- 6.4.4 Beckers Group

- 6.4.5 Berger Paints India

- 6.4.6 Carboline

- 6.4.7 Chugoku Marine Paints, Ltd.

- 6.4.8 H.B. Fuller Company

- 6.4.9 Hempel A/S

- 6.4.10 Jotun

- 6.4.11 Kansai Paint Co., Ltd.

- 6.4.12 Nippon Paint Holdings Co., Ltd.

- 6.4.13 PPG Industries, Inc.

- 6.4.14 RPM International Inc.

- 6.4.15 Sika AG

- 6.4.16 Teknos Group

- 6.4.17 The Sherwin-Williams Company

- 6.4.18 Tikkurila

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment