PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939625

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939625

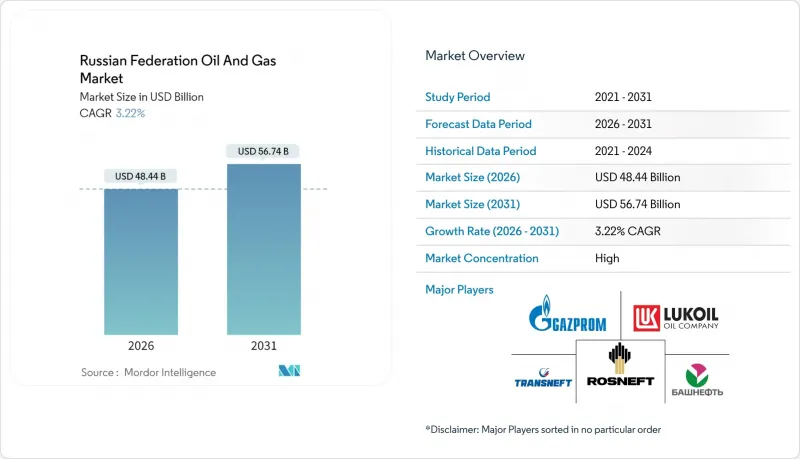

Russian Federation Oil And Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Russian Federation Oil And Gas Market was valued at USD 46.93 billion in 2025 and estimated to grow from USD 48.44 billion in 2026 to reach USD 56.74 billion by 2031, at a CAGR of 3.22% during the forecast period (2026-2031).

Robust upstream volumes, expanding pipeline corridors to Asia, and multibillion-dollar Arctic LNG installations anchor this steady trajectory, while state incentives for enhanced oil recovery (EOR) soften natural decline rates in Western Siberia. The Russian Federation oil and gas market additionally benefits from import-substitution policies that stimulate domestic petrochemicals demand, creating a stable offtake base for associated gas and liquids. Simultaneously, the midstream build-out around the Power of Siberia 2 trunkline and the ESPO crude system adds fresh revenue streams for service contractors and pipe manufacturers. Heightened investment in indigenous digital tools further cushions operators from technology embargoes by lifting brownfield recovery and reducing unplanned downtime.

Russian Federation Oil And Gas Market Trends and Insights

Pivot to Asian Export Pipelines Drive Market Reorientation

Russia's pledge to deliver 50 billion m3 annually via Power of Siberia 2 and to raise ESPO crude throughput to 80 million tonnes places the Russian Federation's oil and gas market at the heart of Asia's energy security agenda.Engineering packages for the 2,600 km conduit have already spurred a wave of steel-plate, compressor-station, and SCADA procurements that reverberate through domestic supply chains. China and India absorbed more than 70% of 2024 Russian crude exports, cushioning operators against European embargoes. The trunkline's high load factor promises stable midstream tolling revenue, which, in turn, de-risks upstream FIDs in stranded Tomsk and Krasnoyarsk licenses. Over the long term, integration with Mongolia's gas grid may unlock additional demand from landlocked Chinese provinces and broaden tariff options for Gazprom.

Arctic LNG and Vostok Oil Megaprojects Reshape Production Geography

Arctic LNG 2 and Vostok Oil rank among the largest global capital projects, pooling nearly USD 120 billion to tap more than 10 billion barrels of oil equivalent (boe) of recoverable reserves.Modular yard fabrication expedites schedule adherence while minimizing on-ice erection risk, an approach now viewed as a blueprint for future Barents and Kara Sea ventures. Gravity-based structures anchored at Utrenneye withstand ice loads of 10 kN/m2, showcasing Russian engineering resilience. Digital twins guide drilling and logistics in temperatures that reach as low as -50 °C, reducing NPT by 17% compared to first-generation Yamal trains. Although sanctions add friction to equipment procurement, Asian yards are filling turbine and cryogenic module gaps through barter-style supply deals. Job creation is expected to exceed 70,000 through 2027, yet labor churn remains elevated due to remote logistics and harsh rotation cycles.

Western Sanctions Constrain Technological Advancement and Capital Access

Embargoes restrict access to subsea Christmas trees, fifth-generation drillships, and cryogenic compressors, prolonging project timelines by up to 24 months and increasing borrowing costs by 200-300 basis points. Domestic yards substitute some packages, but deepwater BOPs and 15-kpsi manifolds remain scarce, curbing offshore frontier drilling. The financing drag pushes state banks to syndicate 15-year debt on concessionary terms, yet balance-sheet constraints cap aggregate exposure, forcing phased FIDs. Operators pivot to yuan-denominated credit and barter crude-for-equipment swaps, but currency mismatch exposes them to FX risk. Even so, USD 8 billion per year now flows into local R&D, spurring partial catch-up in telemetry, fracturing fluids, and reservoir modeling software, albeit with performance still trailing that of Western peers.

Other drivers and restraints analyzed in the detailed report include:

- Government Tax Incentives Accelerate EOR and LNG Development

- Petrochemical Import Substitution Creates Downstream Demand

- Oil Price Volatility Threatens Project Economics and Budget Revenues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Upstream activities represented 73.10% of the 2025 Russian Federation oil and gas market share, underpinned by 10.8 million bpd liquids output and 669 billion m3 gas production. Mature giants such as Samotlor still yield 1.1 million bpd after EOR, while green-field Arctic LNG 2 feed gas elevates supply resilience. The midstream build-out is on track for a 4.34% CAGR through 2031, propelled by Power of Siberia 2, ESPO debottlenecking, and a 50-tanker Arctic shuttle fleet. Downstream plants navigate sanctions by retooling catalytic crackers for higher domestic Euro VI-grade output, yet they suffer from catalyst shortages that curb throughput efficiency. Russian Federation oil and gas market participants thus shift capital toward pipe mills, pump manufacturers, and SCADA vendors that unlock transportation margins.

Structural evolution favors vertical integration, as upstream firms purchase pipe yards, compressor shops, and even rail fleets to insulate their operations from logistical chokepoints. Indigenous software now covers 70% of drilling automation tasks, reducing Western license fees by USD 250 million annually. State support programs, such as Zazemleniye, guarantee offtake for domestically produced pigging robots, further embedding local supply chains. These adjustments pave the way for a more balanced revenue mix, wherein transmission tolls and processing spreads help mitigate commodity swings.

The Russian Federation Oil and Gas Market Report is Segmented by Sector (Upstream, Midstream, and Downstream), Location (Onshore and Offshore), and Service (Construction, Maintenance and Turn-Around, and Decommissioning). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Rosneft Oil Company PJSC

- PJSC Gazprom

- PJSC Lukoil Oil Company

- Novatek PAO

- Transneft Group

- PJSC ANK Bashneft

- Gazprom Neft PJSC

- Tatneft PJSC

- Surgutneftegas PJSC

- Sakhalin Energy LLC

- Yamal LNG LLC

- Slavneft PJSC

- RussNeft PJSC

- Irkutsk Oil Company

- Zarubezhneft JSC

- Gazprom Transgaz LLC

- NNK (Independent Oil & Gas Company)

- RusGazDobycha LLC

- Yakutsk Fuel-Energy Company (YATEC)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pivot to Asian export pipelines (Power of Siberia 2, ESPO expansion)

- 4.2.2 Arctic LNG & Vostok Oil megaproject investments

- 4.2.3 Government tax incentives for EOR & LNG

- 4.2.4 Petrochemical demand from import substitution

- 4.2.5 Indigenous digital upstream technologies

- 4.2.6 Far-East energy corridor build-out

- 4.3 Market Restraints

- 4.3.1 Western sanctions on technology & finance

- 4.3.2 Oil-price volatility

- 4.3.3 Demographic decline in remote basins

- 4.3.4 Permafrost-thaw pipeline damage risk

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Crude-Oil Production & Consumption Outlook

- 4.8 Natural-Gas Production & Consumption Outlook

- 4.9 Installed Pipeline Capacity Analysis

- 4.10 Unconventional Resources CAPEX Outlook (tight oil, oil sands, deep-water)

- 4.11 Porters Five Forces

- 4.11.1 Threat of New Entrants

- 4.11.2 Bargaining Power of Suppliers

- 4.11.3 Bargaining Power of Buyers

- 4.11.4 Threat of Substitutes

- 4.11.5 Competitive Rivalry

- 4.12 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Sector

- 5.1.1 Upstream

- 5.1.2 Midstream

- 5.1.3 Downstream

- 5.2 By Location

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 By Service

- 5.3.1 Construction

- 5.3.2 Maintenance and Turn-around

- 5.3.3 Decommissioning

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Rosneft Oil Company PJSC

- 6.4.2 PJSC Gazprom

- 6.4.3 PJSC Lukoil Oil Company

- 6.4.4 Novatek PAO

- 6.4.5 Transneft Group

- 6.4.6 PJSC ANK Bashneft

- 6.4.7 Gazprom Neft PJSC

- 6.4.8 Tatneft PJSC

- 6.4.9 Surgutneftegas PJSC

- 6.4.10 Sakhalin Energy LLC

- 6.4.11 Yamal LNG LLC

- 6.4.12 Slavneft PJSC

- 6.4.13 RussNeft PJSC

- 6.4.14 Irkutsk Oil Company

- 6.4.15 Zarubezhneft JSC

- 6.4.16 Gazprom Transgaz LLC

- 6.4.17 NNK (Independent Oil & Gas Company)

- 6.4.18 RusGazDobycha LLC

- 6.4.19 Yakutsk Fuel-Energy Company (YATEC)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment