PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940634

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940634

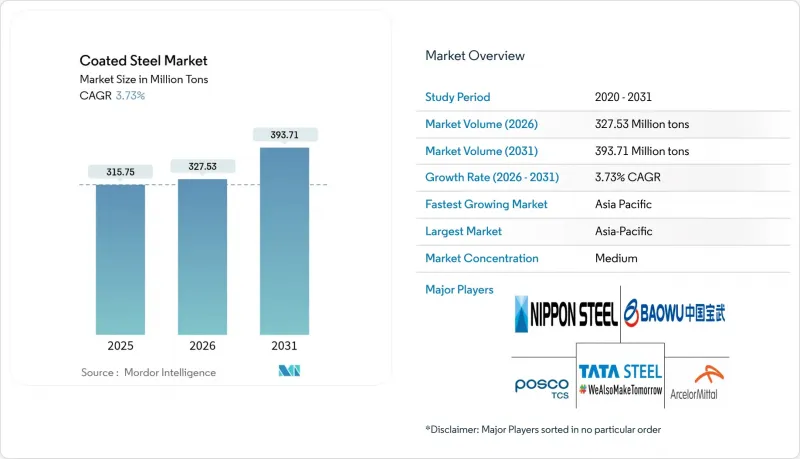

Coated Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Coated Steel Market was valued at 315.75 Million tons in 2025 and estimated to grow from 327.53 Million tons in 2026 to reach 393.71 Million tons by 2031, at a CAGR of 3.73% during the forecast period (2026-2031).

This growth reflects resilient demand from automotive lightweighting programs, expanding energy-efficient building envelopes, and sustained capacity additions in key production hubs. Momentum is reinforced by quicker commercialization of Zn-Al-Mg alloy coatings that extend service life versus conventional galvanized products. Producers are also pursuing vertical integration and renewable-powered operations to hedge raw-material volatility and meet tightening carbon rules. Trade remedies-most notably the United States' anti-dumping duties on corrosion-resistant imports-reshape regional supply flows while favoring domestic investments. At the same time, EU carbon-border pricing accelerates disclosure of embedded emissions, allowing certified low-carbon coated steel to command premiums.

Global Coated Steel Market Trends and Insights

Surging Demand for AHSS-Based Coated Steels in EV Lightweighting

Electric-vehicle producers now specify advanced high-strength steel grades paired with coatings that survive complex forming while protecting battery enclosures and crash structures. ArcelorMittal's USD 1.2 billion Alabama electrical-steel project illustrates strategic capital alignment with this trend. Zn-Al-Mg chemistries offer edge-corrosion resistance crucial for laser-welded battery packs, positioning coated AHSS as a bridge between legacy auto steel and next-generation mobility.

Energy-Efficient Building Envelope Adoption of Pre-Painted Coil

Cooling-load regulations spur use of pre-painted coil achieving solar reflectance above 0.7 and thermal emittance beyond 0.8. Asian Development Bank field work shows cool roofs can cut cooling energy 15-20% in tropical settings. PVDF-based coatings such as Kynar 500 provide 30-year warranties that improve lifecycle economics while helping builders meet LEED and EU Ecodesign thresholds.

Zinc and Aluminum Price Volatility

Spot zinc closed 2024 at RMB 25,900 per ton, up 19.8% year-on-year, before easing to RMB 23,370 in Q1 2025 amid mine disruptions and demand swings. Aluminum shows similar gyrations, complicating procurement for Zn-Al-Mg and aluminized lines. Margin compression is most severe where passing costs downstream meets contract lags.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Rollout of Zn-Al-Mg Alloy Coating Lines in Asia

- Tax-Driven Appliance Replacement Programs (EU and US)

- Aluminum-Composite Facade Substitution

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hot-dipped material held 63.10% of coated steel market share in 2025, equating to roughly 199 million tons. Its 3.89% CAGR through 2031 anchors the coated steel market size for traditional construction, appliance, and storage uses. Electro-galvanized and aluminized alternatives grow faster in high-precision or high-temperature niches, but capacity build-outs center on hot-dip lines due to capital efficiency.

The coated steel industry is pivoting toward Zn-Al-Mg alloys classified in the "Others" bucket, where AM/NS India's Magnelis offers 3-5 times galvanized corrosion life. Producers integrate laser-welding-friendly chemistries for auto body-in-white, suggesting hot-dipped volume will gradually cede mix share to next-generation coatings rather than suffer absolute decline.

The Coated Steel Market Report is Segmented by Product Type (Hot-Dipped, Galvannealed, Electro-Galvanized, Aluminized, and Others), Application (Construction and Building Components, Automotive Components, Appliances, Pipe and Tubular, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific commanded 61.10% of coated steel market share in 2025-just over 193 million tons-and is projected at a 4.47% CAGR to 2031. China leads with integrated mills upgrading downstream lines, while India, South Korea, and Japan export specialty products. ASEAN nations expand capacity for solar, logistics, and housing projects, enhancing regional coated steel market resilience.

North America ranks second. U.S. anti-dumping tariffs covering corrosion-resistant sheet from 10 countries have narrowed import options, encouraging investments such as Nucor's USD 425 million South Carolina galvanizing line and Hyundai Steel's USD 5.8 billion Louisiana integrated plant. Mexico's 8 million-ton capacity additions over 2025-2026 reinforce near-shoring, keeping the coated steel market in the hemisphere balanced.

Europe confronts energy-cost spikes and CBAM compliance. Producers showcase Environmental Product Declarations to secure architectural premiums and mitigate carbon levies. Germany, France, Italy, and the United Kingdom remain anchor consumers, while Nordic mills focus on renewables and marine segments. Regulatory certainty on circularity and scrap use will shape Europe's coated steel market competitiveness.

- AM/NS INDIA

- ArcelorMittal

- China Baowu Steel Group Corp., Ltd

- CUMIC STEEL LIMITED

- JFE Steel Corporation

- Jindal Steel

- JSW

- KOBE STEEL, LTD.

- MMK (PJSC)

- Nippon Steel Coated Sheet Corporation

- NLMK

- NS BlueScope

- Nucor Corporation

- POSCO Coated Steel(Thailand) Co.,Ltd.

- Salzgitter Flachstahl GmbH

- SSAB AB

- Tata Steel

- thyssenkrupp Steel

- United States Steel Corporation

- voestalpine Stahl GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for AHSS-Based Coated Steels in EV Lightweighting

- 4.2.2 Energy-Efficient Building Envelope Adoption of Pre-Painted Coil

- 4.2.3 Rapid Rollout of Zn-Al-Mg Alloy Coating Lines In Asia

- 4.2.4 Tax-Driven Appliance Replacement Programs (EU And US)

- 4.2.5 Certified Low-Carbon (EPD/CBAM-Ready) Coated Steels

- 4.3 Market Restraints

- 4.3.1 Zinc And Aluminium Price Volatility

- 4.3.2 Aluminium-Composite Facade Substitution

- 4.3.3 AD/CVD Trade Actions on Coated Sheet

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Hot-dipped

- 5.1.2 Galvannealed

- 5.1.3 Electro-galvanized

- 5.1.4 Aluminized

- 5.1.5 Others Product Types

- 5.2 By Application

- 5.2.1 Construction and Building Components

- 5.2.2 Automotive Components

- 5.2.3 Appliances

- 5.2.4 Pipe and Tubular

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AM/NS INDIA

- 6.4.2 ArcelorMittal

- 6.4.3 China Baowu Steel Group Corp., Ltd

- 6.4.4 CUMIC STEEL LIMITED

- 6.4.5 JFE Steel Corporation

- 6.4.6 Jindal Steel

- 6.4.7 JSW

- 6.4.8 KOBE STEEL, LTD.

- 6.4.9 MMK (PJSC)

- 6.4.10 Nippon Steel Coated Sheet Corporation

- 6.4.11 NLMK

- 6.4.12 NS BlueScope

- 6.4.13 Nucor Corporation

- 6.4.14 POSCO Coated Steel(Thailand) Co.,Ltd.

- 6.4.15 Salzgitter Flachstahl GmbH

- 6.4.16 SSAB AB

- 6.4.17 Tata Steel

- 6.4.18 thyssenkrupp Steel

- 6.4.19 United States Steel Corporation

- 6.4.20 voestalpine Stahl GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment