PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940663

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940663

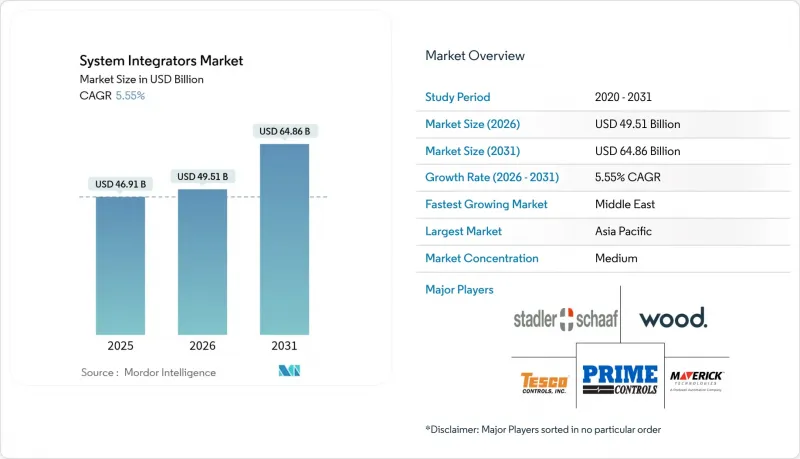

System Integrators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The system integrators market was valued at USD 46.91 billion in 2025 and estimated to grow from USD 49.51 billion in 2026 to reach USD 64.86 billion by 2031, at a CAGR of 5.55% during the forecast period (2026-2031).

Expansion is underpinned by manufacturers shifting from isolated upgrades to turnkey OT-IT convergence projects that shorten payback periods while minimizing production downtime. Brownfield plants account for a rising share of new awards, and multi-vendor edge deployments anchored in private-5G are unlocking fresh demand for advanced orchestration skills. At the same time, utilities in Europe and Asia are digitizing renewable assets to comply with aggressive clean-energy targets, a change that favors integrators fluent in SCADA upgrades and DER management. Regulatory cybersecurity mandates for critical infrastructure, most visibly in the Middle East, are widening the addressable pool of high-margin SCADA retrofit projects. Talent shortages on the plant floor further tilt the build-versus-buy calculus toward outsourcing, enabling mid-tier firms to capture share from large automation vendors.

Global System Integrators Market Trends and Insights

Demand for Turn-Key OT-IT Convergence Projects in Brownfield Manufacturing Plants

Turn-key OT-IT programs are replacing incremental upgrades because manufacturers now target ROI cycles below 18 months. The challenge of mapping decades-old PLCs to modern cloud architectures creates enduring demand for integrators able to manage coexistence, cybersecurity and analytics in one scope. Process industries feel this pressure most acutely, since one hour of unplanned downtime can exceed USD 50,000 in lost output.

Acceleration of Renewable-Energy Asset Digitalization Across Europe and Asia

European utilities must orchestrate nearly 900 GW of solar capacity by 2030, a milestone that compels tighter coupling of forecasting, storage and grid-balancing applications. The BaxEnergy platform, now owned by Yokogawa, already monitors 120 GW of renewables across 40 countries, illustrating the scale and complexity of next-gen projects.

High Project Scope-Creep Risk Elevating Total Cost of Ownership for End-Users

More than 40% of integration programs overshoot original budgets as engineers confront undocumented interfaces and obsolete firmware mid-project. The U.S. Government Accountability Office found that Category 1 technology projects still account for 81% of federal overruns, underscoring how scope drift persists even under strict governance.

Other drivers and restraints analyzed in the detailed report include:

- 5G-Enabled Edge Computing Use-Cases Requiring Complex Multi-Vendor Integration in North America

- Regulatory Push for Cyber-Secure SCADA Retrofits in Critical Infrastructure (Middle East)

- Procurement Delays Caused by Semiconductor Supply Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software and Digital Integration controlled 47.35% of system integrators market size in 2025 on the strength of analytics, MES and cloud-edge orchestration suites. IIoT and Edge-Focused Integration posts a 8.75% CAGR to 2031 as firms deploy containerized workloads at the machine level. Hardware retrofits remain vital for brownfield sites, but their share is gradually receding as manufacturers monetize data rather than pure throughput. Consulting and Training demand is reviving because talent gaps force companies to upskill in-house staff, while After-Sales Support secures recurring revenue that cushions cyclical project flow. The Litmus Edge-Azure IoT tie-up typifies the pivot toward standardized connectors like OPC UA and MQTT that cut roll-out times.

A second structural change is the rise of proprietary integration platforms that bundle middleware, pre-built APIs and digital-twin libraries. These services allow integrators to monetize intellectual property beyond hourly engineering fees, increasing switching costs. As more manufacturers favor outcome-based contracts, software-heavy scopes will likely surpass 55% share of the system integrators market by decade-end.

Integrated Process Control solutions-PLC, DCS and SCADA-accounted for 34.02% of system integrators market share in 2025, evidence that foundational control layers still anchor digital transformation roadmaps. Even so, Industrial Cyber-Security Solutions outpace every other cluster at a 10.05% CAGR as ransomware moves from IT to OT domains. Manufacturing Execution Systems keep growing steadily because executives need unified production and business data to run profit-center accounting. Robotics and Machine Vision projects gain traction where labor costs outstrip capex depreciation curves.

Cybersecurity's acceleration is visible in Rockwell's acquisition of Verve Industrial Protection, which unified asset inventory, risk scoring and breach response in a vendor-neutral stack. Siemens echoed this trend with its SIBERprotect solution that triggers automated responses within milliseconds, balancing uptime and safety. As regulations tighten, integrators that embed zero-trust architectures into process-control migrations are set to capture premium fees.

System Integrators Market Report is Segmented by Service Type (Hardware Integration, Software and Digital Integration, and More), Technology (Integrated Process Control, Manufacturing Execution Systems, and More), End-User Industry (Oil and Gas, Automotive and EV Manufacturing, and More), Enterprise Scale (SMEs, Large Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the system integrators market with 31.20% revenue in 2025, spurred by China's price-intensive automation landscape and India's expanding ethanol and co-gen base. Local competitors such as Ditap-V Automatio win bids by balancing quality and aggressive pricing, raising pressure on multinational incumbents. Government-sponsored smart-manufacturing schemes amplify demand, yet geopolitical frictions and shipping bottlenecks threaten delivery schedules.

The Middle East is the fastest-growing territory, forecast at 8.46% CAGR through 2031. Vision 2030 megaprojects and an expanding regulatory net for OT cybersecurity elevate average project values. Emerson's 140,000 ft2 manufacturing hub at King Salman Energy Park shows how global vendors localize supply chains to satisfy in-country value quotas. Meanwhile, the India-Middle East-Europe Economic Corridor could slash freight costs by 30% once operational, creating further pull for integrators versed in cross-border standards.

North America and Europe remain lucrative but mature. The U.S. sees outsized growth from private-5G and edge-AI pilots, yet chronic labor shortages inflate wage bills. Europe's renewable push forces utilities to blend grid-scale batteries, PV inverters and demand-response software in coherent stacks, an integration puzzle that sustains robust project pipelines. Both regions confront stringent safety codes that lengthen approval cycles, underscoring the value of domain-rich integrators.

- ABB Ltd.

- Siemens AG

- Rockwell Automation, Inc.

- Schneider Electric SE

- Honeywell International Inc.

- Emerson Electric Co.

- Yokogawa Electric Corporation

- John Wood Group PLC

- TESCO CONTROLS, Inc.

- STADLER + SCHAAF Mess- und Regeltechnik GmbH

- Prime Controls, LP

- MAVERICK Technologies, LLC

- Adsyst Automation Ltd.

- George T. Hall Company

- Avanceon Ltd.

- Wunderlich-Malec Engineering, Inc.

- Burrow Global, LLC

- ATS Corporation

- HCLTech (Industrial and Digital SI Practice)

- Accenture plc (Industry X)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for Turn-Key OT-IT Convergence Projects

- 4.2.2 Acceleration of Renewable-Energy Asset Digitalization

- 4.2.3 5G-Enabled Edge Computing Use-Cases

- 4.2.4 Regulatory Push for Cyber-Secure SCADA Retrofits

- 4.2.5 Rising Adoption of Modular Automation

- 4.2.6 Shortage of Plant-Floor Automation Talent

- 4.3 Market Restraints

- 4.3.1 High Project Scope-Creep Risk

- 4.3.2 Procurement Delays

- 4.3.3 Fragmented Vendor Ecosystem

- 4.3.4 Critical Liability Exposure

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hardware Integration

- 5.1.2 Software and Digital Integration

- 5.1.3 Consulting and Training

- 5.1.4 After-Sales Support and Maintenance

- 5.2 By Technology

- 5.2.1 Integrated Process Control (PLC, DCS, SCADA)

- 5.2.2 Manufacturing Execution Systems (MES)

- 5.2.3 Robotics and Machine Vision

- 5.2.4 IIoT and Edge Platforms

- 5.2.5 Cyber-Security Solutions

- 5.3 By End-User Industry

- 5.3.1 Oil and Gas

- 5.3.2 Automotive and EV Manufacturing

- 5.3.3 Aerospace and Defense

- 5.3.4 Healthcare and Life Sciences

- 5.3.5 Energy and Power

- 5.3.6 Chemicals and Petrochemicals

- 5.3.7 Food and Beverage

- 5.3.8 Metals and Mining

- 5.3.9 Others (Water / Waste-Water, Pulp and Paper)

- 5.4 By Enterprise Scale

- 5.4.1 SMEs

- 5.4.2 Large Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Latin America

- 5.5.2.1 Mexico

- 5.5.2.2 Brazil

- 5.5.2.3 Argentina

- 5.5.2.4 Rest of Latin America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Middle East and Africa

- 5.5.5 Asia-Pacific

- 5.5.5.1 China

- 5.5.5.2 Japan

- 5.5.5.3 South Korea

- 5.5.5.4 India

- 5.5.5.5 Australia

- 5.5.5.6 Rest of Asia Pacific

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global?level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Siemens AG

- 6.4.3 Rockwell Automation, Inc.

- 6.4.4 Schneider Electric SE

- 6.4.5 Honeywell International Inc.

- 6.4.6 Emerson Electric Co.

- 6.4.7 Yokogawa Electric Corporation

- 6.4.8 John Wood Group PLC

- 6.4.9 TESCO CONTROLS, Inc.

- 6.4.10 STADLER + SCHAAF Mess- und Regeltechnik GmbH

- 6.4.11 Prime Controls, LP

- 6.4.12 MAVERICK Technologies, LLC

- 6.4.13 Adsyst Automation Ltd.

- 6.4.14 George T. Hall Company

- 6.4.15 Avanceon Ltd.

- 6.4.16 Wunderlich-Malec Engineering, Inc.

- 6.4.17 Burrow Global, LLC

- 6.4.18 ATS Corporation

- 6.4.19 HCLTech (Industrial and Digital SI Practice)

- 6.4.20 Accenture plc (Industry X)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment