PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940727

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940727

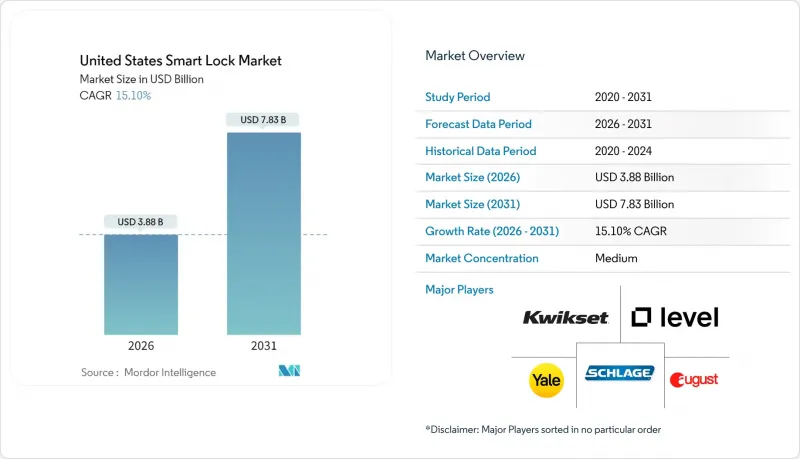

United States Smart Lock - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States Smart Lock Market is expected to grow from USD 3.37 billion in 2025 to USD 3.88 billion in 2026 and is forecast to reach USD 7.83 billion by 2031 at 15.1% CAGR over 2026-2031.

In terms of shipment volume, the market is expected to grow from 17.46 million units in 2025 to 39.03 million units by 2030, at a CAGR of 17.45% during the forecast period (2025-2030). Momentum stems from persistent package-theft incidents, broader smart-home ecosystem maturity, and ultra-wideband (UWB) integration in mainstream smartphones. Deadbolt compatibility with existing door hardware underpins widespread residential adoption, while specialty locks gain traction in commercial retrofits. Build-to-rent developers and insurance incentives accelerate demand, and strategic consolidation among leading brands reinforces competitive intensity across both online and offline channels.

United States Smart Lock Market Trends and Insights

Increasing Integration with Smart-Home Hubs and Voice Assistants

Smart lock demand accelerates as manufacturers achieve native compatibility with Amazon Alexa, Google Home, and Apple HomeKit. The arrival of the Matter over Thread protocol standardizes device communication and allows smart locks to function as energy-efficient mesh nodes. Yale Assure Lock 2 operates across multiple ecosystems without proprietary hubs, illustrating this shift. Voice-activated unlocking now layers authentication through voice patterns and contextual cues, improving security and convenience. Each additional smart device increases overall network utility, prompting replacement cycles as users transition from point solutions to unified access management.

Rising Package-Theft Incidents Boosting Entryway Security Demand

More than 260 million deliveries faced theft in 2024, representing USD 20 billion in lost goods. Smart locks solve last-meter security by issuing temporary codes for delivery personnel, enabling in-home or vestibule drops. Amazon's Key program demonstrated mainstream acceptance when monitored access and liability coverage are present . The same capability extends to service providers such as cleaners and healthcare aides, offering audit logs that satisfy insurers and property managers.

Persistent Cyber-Security Vulnerabilities and Public Hacks

Academic testing in 2024 revealed 14 zero-day flaws in mainstream smart locks. Issues include static Bluetooth GATT values, 433 MHz replay vectors, and RFID cloning. Some older hardware lacks over-the-air update capability, leaving users exposed. High-profile demonstrations erode trust, even as new models add encrypted storage and stronger cryptography. Regulators lag behind the threat curve, so consumers rely on third-party audits that frequently uncover gaps.

Other drivers and restraints analyzed in the detailed report include:

- Insurance Premium Discounts for Smart-Security Installations

- UWB Passive-Entry in Smartphones

- Multi-Family Building Code Restrictions on Retrofit Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Deadbolt locks accounted for 61.12% of the US Smart Lock Market share in 2025 because most US doors are pre-bored for this format. Retrofit convenience encourages DIY adoption, and platform support from dominant brands reinforces deadbolt strength. The segment benefits from frequent insurance discounts and a rich accessory ecosystem that includes video doorbells and sensors. Specialty categories such as mortise and lever locks grow at a 17.43% CAGR as commercial renovations demand architecture-specific hardware. These products integrate advanced credentials such as biometric pads, which lift the average selling price and margin.

Specialty growth stems from commercial building upgrades, hospitality retrofits, and high-end residential applications that favor design continuity. The US Smart Lock Market size for mortise solutions is forecast to expand steadily as system integrators bundle access control with building automation platforms. Rugged padlocks address outdoor storage and construction needs where weather sealing is critical. Although niche, the padlock segment proves smart access utility beyond the front door, broadening vendor addressable revenue.

Residential buyers represented 88.90% of revenue in 2025 due to the enormous installed base of single-family homes and growing DIY culture. Voice-assistant interoperability and discounted insurance premiums sustain household demand. Battery life improvements lengthen replacement cycles, but upgrade intent remains high because UWB and Matter features motivate second-generation purchases. Commercial deployments, however, record an 18.28% CAGR. Property managers value centralized credential management that trims labor costs tied to mechanical key turnover.

Cloud dashboards let facilities revoke or grant access across hundreds of doors within seconds. The US Smart Lock Market size for commercial applications is forecast to rise sharply in multi-family and healthcare properties, where audit compliance drives technology adoption. Rising corporate ESG goals also favor smart locks that integrate with energy management systems and occupancy analytics.

The United States Smart Lock Market Report is Segmented by Product Type (Deadbolt, Padlock, Other Product Types), End-User (Residential, Commercial), Installation Type (Retrofit, New-Construction Integrated), and Distribution Channel (Online, Offline). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Shipments).

List of Companies Covered in this Report:

- August Home Inc. (ASSA ABLOY AB)

- Yale Home (ASSA ABLOY AB)

- Kwikset (ASSA ABLOY AB)

- Schlage (Allegion Company)

- Level Home Inc.

- U-Tec Group Inc.

- Wyze Labs, Inc.

- Lockly Inc.

- Eufy Security (Anker Innovations)

- SimpliSafe, Inc.

- Sentrilock, LLC

- Gate Labs Inc.

- RemoteLock

- SwitchBot Inc.

- Onity Inc. (Carrier Global)

- Digilock Inc.

- Igloohome Pte Ltd

- Nuki Home Solutions Inc.

- PDQ Locks

- Baldwin (Part of ASSA ABLOY)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing integration with smart-home hubs and voice assistants

- 4.2.2 Rising package-theft incidents boosting entryway security demand

- 4.2.3 Insurance premium discounts for smart-security installations

- 4.2.4 Build-to-rent single-family developments adopting smart locks at scale

- 4.2.5 ESG/LEED incentives for connected access solutions

- 4.2.6 UWB passive-entry in smartphones

- 4.3 Market Restraints

- 4.3.1 Persistent cyber-security vulnerabilities and public hacks

- 4.3.2 Multi-family building code restrictions on retrofit devices

- 4.3.3 Chip-set supply constraints for secure SoCs

- 4.3.4 Consumer privacy concerns over data sharing

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of Substitute Products

- 4.8 Pricing and Historical Price Trends

- 4.9 An Assessment of Macroeconomic Impact on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Deadbolt

- 5.1.2 Padlock

- 5.1.3 Other Product Types (Mortise, etc.)

- 5.2 By End-user

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.3 By Installation Type

- 5.3.1 Retrofit

- 5.3.2 New-Construction Integrated

- 5.4 By Distribution Channel

- 5.4.1 Online (Direct and Marketplaces)

- 5.4.2 Offline (Retail, Installers)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 August Home Inc. (ASSA ABLOY AB)

- 6.4.2 Yale Home (ASSA ABLOY AB)

- 6.4.3 Kwikset (ASSA ABLOY AB)

- 6.4.4 Schlage (Allegion Company)

- 6.4.5 Level Home Inc.

- 6.4.6 U-Tec Group Inc.

- 6.4.7 Wyze Labs, Inc.

- 6.4.8 Lockly Inc.

- 6.4.9 Eufy Security (Anker Innovations)

- 6.4.10 SimpliSafe, Inc.

- 6.4.11 Sentrilock, LLC

- 6.4.12 Gate Labs Inc.

- 6.4.13 RemoteLock

- 6.4.14 SwitchBot Inc.

- 6.4.15 Onity Inc. (Carrier Global)

- 6.4.16 Digilock Inc.

- 6.4.17 Igloohome Pte Ltd

- 6.4.18 Nuki Home Solutions Inc.

- 6.4.19 PDQ Locks

- 6.4.20 Baldwin (Part of ASSA ABLOY)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment