PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940741

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940741

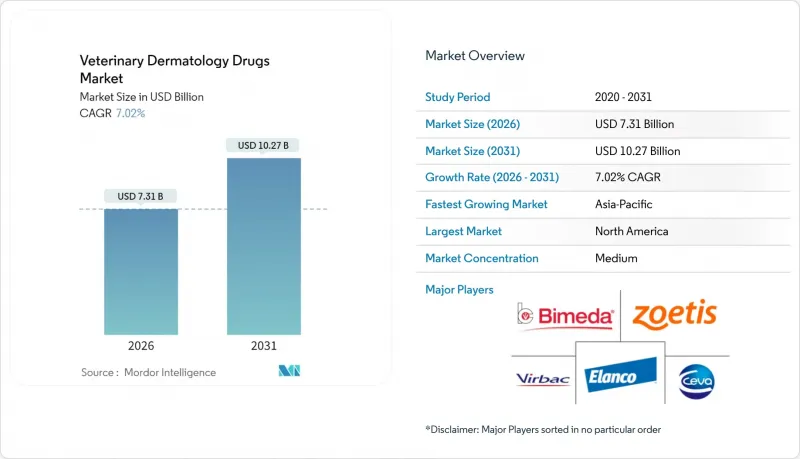

Veterinary Dermatology Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The veterinary dermatology drugs market was valued at USD 6.8 billion in 2025 and estimated to grow from USD 7.31 billion in 2026 to reach USD 10.27 billion by 2031, at a CAGR of 7.02% during the forecast period (2026-2031).

Robust pet-humanisation trends, rising allergic skin disorders, and rapid uptake of long-acting biologics are steering demand, while climate-driven parasite range expansion is reshaping disease seasonality and forcing year-round prevention strategies. Market leaders are shifting portfolios toward precision immunomodulators that command premium pricing and improve compliance, especially injectable monoclonal antibodies that provide up to eight weeks of relief per dose. Digital sales channels are accelerating fastest, eroding traditional clinic retail dominance and strengthening companies with direct-to-consumer fulfilment capability. Regionally, North America remains the largest buyer, yet Asia-Pacific supplies the steepest growth curve on the back of rising disposable incomes and expanding veterinary infrastructure.

Global Veterinary Dermatology Drugs Market Trends and Insights

Rising Incidence Of Allergic & Atopic Dermatitis In Companion Animals

Allergic skin diseases now affect close to 15% of the global dog population, and the share is still climbing as urban living exposes pets to new indoor allergens. The FDA clearance of Zenrelia in 2024 added a second JAK inhibitor option and underlined the shift toward cytokine-targeted modulation. Clinical data show 77% of treated dogs achieve low itch scores, outpacing legacy therapies and pushing clinics to rewrite protocols. Monoclonal antibodies such as Cytopoint sustain 90% initial efficacy and 77% maintenance, creating predictable repeat-dose revenue for veterinarians. Chronic management rather than episodic relief is, therefore, anchoring the veterinary dermatology drugs market, driving premium adoption across all major regions. Elevated clinical standards further reinforce growth as owners seek human-level outcomes for pets.

Surge In Global Pet Ownership & Pet Humanisation Expenditure

Asia-Pacific's rising middle-income households are treating pets as family members, shifting spend towards higher-value care. Insurance coverage in Europe and North America is widening treatment affordability thresholds, especially for long-term dermatology regimens. Owners are increasingly willing to fund preventive skin care and genetic-based therapies, a trend expected to support long-run CAGR uplift. The veterinary dermatology drugs market therefore benefits from an entrenched lifestyle shift rather than a cyclical consumption spike.

Limited Awareness & Access In Low-Income Regions

Veterinary dermatology remains a low priority where basic vaccinations still compete for limited household budgets. Sparse specialist availability intensifies the gap, with most board-certified dermatologists concentrated in high-income urban centres. Cultural norms in some emerging economies also place limited emphasis on chronic dermatological care, restricting uptake of premium options. Absent insurance coverage further curbs affordability, stalling veterinary dermatology drugs market penetration. Over time, NGO and tele-health initiatives may soften barriers, yet the near-term drag persists.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Uptake Of Novel Monoclonal Antibody & JAK-Inhibitor Therapies

- Climate-Driven Expansion Of Ectoparasite Range Elevating Skin Infections

- High Cost Of Biologics & Chronic Therapy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Companion animals commanded 72.12% of veterinary dermatology drugs market share in 2025, and the category is projected to post a 9.58% CAGR to 2031. The surge reflects a deep behavioural shift that sees pets treated as family members, fuelling spend on immunotherapies, bespoke shampoos, and preventive regimens. Increased insurance uptake in North America and Europe widens access to chronic care programmes, cementing revenue predictability for clinics. Meanwhile, livestock skin therapeutics remain driven by welfare regulation and production economics rather than owner sentiment, creating a smaller but stable revenue pool. Rising awareness of zoonotic risk in food animals may lift prophylactic demand, yet the growth delta versus companion ownership remains wide. Pharmaceutical firms therefore channel the bulk of R&D funds into canine and feline indications where biologics acceptance and pricing power are strongest. This skew underpins the companion segment's weight in the veterinary dermatology drugs market size and reinforces future pipeline direction.

Livestock dermatology mostly targets ectoparasite control to protect carcass quality, with purchases often bundled into broader herd-health schemes. Generic actives dominate and pricing remains competitive, limiting margin upside. However, regulatory pressure on antibiotic use is nudging producers toward integrated pest-management that may include novel topicals, opening a modest premium tier. Despite such developments, companion care will continue to dictate innovation cycles and marketing investment.

Injectable formats represented the fastest-growing delivery class with an 11.78% CAGR, driven by monoclonal antibodies that ensure four-to-twelve-week efficacy per shot. These long-acting drugs upend compliance barriers linked to daily oral tablets or messy topicals. Topical solutions, still accounting for 47.02% of veterinary dermatology drugs market size in 2025, hold value for acute parasite knock-down and cosmetic skin repair, yet they face share erosion as owners opt for convenience. Oral JAK inhibitors such as Zenrelia maintain relevance by offering once-daily dosing and comparable itch control, giving clinicians flexibility in multi-modal regimens.

Veterinarians weigh factors such as owner skill, animal temperament, and disease chronicity when selecting routes. The high revenue per visit attached to injectables also aligns with clinic economics, encouraging adoption. Research pipelines now explore micro-implant and depot formulations that could extend dosing intervals beyond twelve months, potentially redefining veterinary dermatology drugs market share allocations across delivery modes.

The Veterinary Dermatology Drugs Market Report is Segmented by Animal (Companion Animal and Livestock Animal), Route of Administration (Topical, Injectable, and Oral), Indication (Parasitic Infections, Allergic Infections, and Other Indications), Distribution Channel (Retail, Hospital Pharmacies and E-Commerce), and Geography (North America, Europe, Asia-Pacific and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 38.42% of 2025 revenue thanks to high pet-insurance penetration, broad specialist availability, and rapid willingness to trial premium biologics. Tick-borne skin diseases are also rising, forcing year-round preventive regimens and lifting prescription volumes. Regulatory pathways under the FDA's Center for Veterinary Medicine remain efficient, facilitating swift market entry for JAK inhibitors and extended-release formulations.

Europe shows a mature yet innovating picture. Stringent EMA oversight and antibiotic-stewardship guidelines guide product choice, supporting non-antibiotic launches such as DuOtic. Rising veterinary service costs in Nordic and UK markets are driving owner demand for therapies that cut repeat visits, thereby favouring long-acting injectables. National variations in insurance coverage shape access, producing heterogeneous adoption curves across the bloc.

Asia-Pacific represents the fastest-growing territory at 11.26% CAGR, propelled by surging pet ownership in China and India and expanding clinic networks. Urbanisation drives allergy prevalence, mirroring Western epidemiology and underpinning early acceptance of biologics among affluent households. Hot-humid climates intensify parasitic burdens, enlarging the preventive segment of the veterinary dermatology drugs market. Regulatory regimes are still maturing, but recent approvals in Japan and Australia signal momentum toward streamlined pathways, which should accelerate product launches.

South America, the Middle East, and Africa remain nascent but attractive over the long term as veterinary infrastructure builds out. Limited specialist density and lower insurance penetration temper current uptake, though e-commerce channels could bypass brick-and-mortar bottlenecks over the next decade. Climate variability is expected to widen parasite habitats across these regions, offering a natural demand catalyst once purchasing power improves.

- Zoetis

- Elanco

- Merck Animal Health (MSD)

- Virbac

- Ceva

- Boehringer Ingelheim

- Bimeda

- Vetoquinol

- Dechra Pharmaceuticals

- Norbrook Laboratories

- Kindred Biosciences

- Nextmune (Stockholm-based)

- Leti Pharma

- Vivaldis

- Bioiberica

- Indian Immunologicals

- Pharmgate Animal Health

- Kyoritsu Seiyaku

- Toray Animal Health

- Hester Biosciences

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence Of Allergic & Atopic Dermatitis In Companion Animals

- 4.2.2 Surge In Global Pet Ownership & Pet Humanisation Expenditure

- 4.2.3 Rapid Uptake Of Novel Monoclonal Antibody & JAK-Inhibitor Therapies

- 4.2.4 Climate-Driven Expansion Of Ectoparasite Range Elevating Skin Infections

- 4.2.5 Emergence Of Tele-Dermatology Platforms Improving Diagnosis Reach

- 4.2.6 Regulatory Antibiotic-Stewardship Pushing Vets Toward Dermatological Preventives

- 4.3 Market Restraints

- 4.3.1 Limited Awareness & Access In Low-Income Regions

- 4.3.2 High Cost Of Biologics & Chronic Therapy

- 4.3.3 Stringent Antimicrobial-Resistance Guidelines Restricting Some Topical Actives

- 4.3.4 Shortage Of Board-Certified Veterinary Dermatologists

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Animal

- 5.1.1 Companion Animal

- 5.1.2 Livestock Animal

- 5.2 By Route of Administration

- 5.2.1 Topical

- 5.2.2 Injectable

- 5.2.3 Oral

- 5.3 By Indication

- 5.3.1 Parasitic Infections

- 5.3.2 Allergic Infections

- 5.3.3 Other Indications

- 5.4 By Distribution Channel

- 5.4.1 Retail

- 5.4.2 Hospital Pharmacies

- 5.4.3 E-commerce

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Zoetis Inc.

- 6.3.2 Elanco Animal Health

- 6.3.3 Merck Animal Health (MSD)

- 6.3.4 Virbac SA

- 6.3.5 Ceva Sante Animale

- 6.3.6 Boehringer Ingelheim Animal Health

- 6.3.7 Bimeda Inc.

- 6.3.8 Vetoquinol SA

- 6.3.9 Dechra Pharmaceuticals

- 6.3.10 Norbrook Laboratories

- 6.3.11 Kindred Biosciences

- 6.3.12 Nextmune (Stockholm-based)

- 6.3.13 Leti Pharma

- 6.3.14 Vivaldis

- 6.3.15 Bioiberica S.A.U.

- 6.3.16 Indian Immunologicals Ltd.

- 6.3.17 Pharmgate Animal Health

- 6.3.18 Kyoritsu Seiyaku

- 6.3.19 Toray Animal Health

- 6.3.20 Hester Biosciences

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment