PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940769

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940769

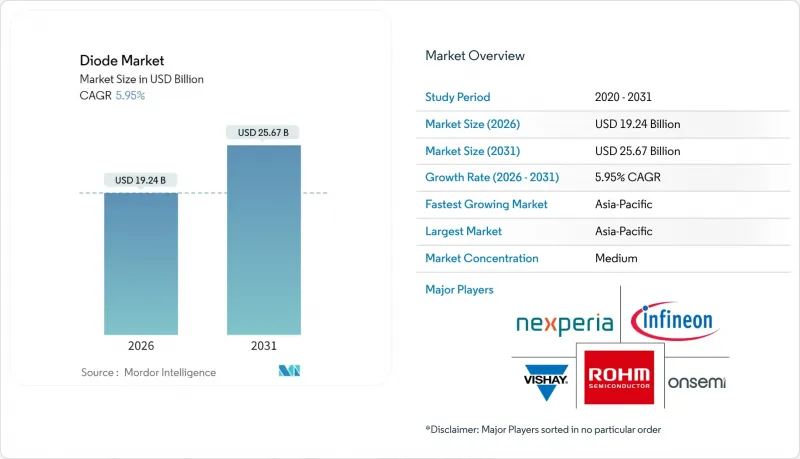

Diode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The diode market is expected to grow from USD 18.16 billion in 2025 to USD 19.24 billion in 2026 and is forecast to reach USD 25.67 billion by 2031 at 5.95% CAGR over 2026-2031.

Consumer electronics remains the largest end-user at 23.2% diode market share, while automotive applications show the strongest 6.8% CAGR as electric-vehicle programs accelerate worldwide. Asia-Pacific holds 58.86% of global revenue and grows at a 6.63% pace thanks to dense manufacturing clusters in China, Japan, and South Korea. Surface-mount packaging captures 61.2% of shipments, yet chip-scale packages rise at a 7.1% CAGR because handset and IoT producers need ever-smaller footprints.

Global Diode Market Trends and Insights

Digitization of Consumer Electronics Ecosystems

Smartphones, wearables, and connected-home devices embed higher semiconductor content per system, lifting discrete component volumes for signal conditioning, battery protection, and data-line safeguarding. Small-signal and electrostatic-discharge arrays such as the ESDS31x series from Texas Instruments deliver +-30 kV protection at up to 5 Gbps data rates, supporting USB, HDMI, and Ethernet interfaces.Asia-Pacific manufacturers assemble about 60% of global electronics hardware, feeding clustered demand for diode arrays that secure high-speed interconnects.

Acceleration of EV Production and On-Board Chargers

Automotive semiconductor demand is increasing as electric-powertrain penetration climbs. Silicon-carbide and gallium-nitride diodes deliver lower switching losses for traction inverters and 800 V chargers; onsemi's EliteSiC platform has been adopted by Volkswagen for next-generation EVs.Infineon's CoolSiC 1200 V MOSFETs allow DC-DC stages to operate beyond 900 V without extra insulation, raising power density while trimming system cost.

Raw-Material Price Volatility (Si, GaAs, GaN)

China provides most primary gallium feedstock, and any export curbs rapidly elevate wafer costs for GaAs and GaN devices. Only 20% of global e-waste is properly recycled, causing critical-metal losses that tighten supply and raise pricing swings. SiC wafer yields remain volatile, contingent on manufacturing maturity and substrate quality.

Other drivers and restraints analyzed in the detailed report include:

- 5G Rollout Boosting RF and Microwave Diodes

- Data-Center Efficiency Mandates Raising Power-Diode Demand

- Thermal Limitations in High-Current Packages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Laser diodes generated the largest diode market size at USD 6.48 billion in 2025 and are positioned for an 8.25% CAGR, propelled by automotive front-lighting, LiDAR sensing, and high-speed fiber communications. Rectifier and Schottky devices continue to secure power-conversion sockets, though their mid-single-digit growth trails laser adoption.

Industrial cutting, projectors, and 3D printing sustain multimode laser-diode volumes, while medical-grade lasers require tighter wavelength stability that lifts average selling prices. In server power supplies, Infineon's GaN transistors integrate a Schottky diode that curbs dead-time losses and elevates efficiency, showcasing cross-category partnerships.

The Diode Market Report is Segmented by Product Type (Schottky Diodes, Zener Diodes, and More), End-User Industry (Communications, Consumer Electronics, Automotive, Defense and Aerospace, Computer and Peripherals, and More), Mounting-Package (Through-Hole, Surface-Mount, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 58.30% of global revenue in 2025, and continues at a 6.45% CAGR through 2031 on the back of integrated supply chains in China, Japan, and South Korea. China absorbed a significant share of world chip sales in 2023, buoyed by government incentives and domestic smartphone exports. Indonesia courts foreign investors with 98 silica-sand mining licenses and tax holidays, aiming to localize substrate production.

North America's share is set to rise by 2030 as the CHIPS Act grants unlock USD 540 billion of private fab commitments, including onsemi's new 8-inch SiC line in Texas. Canada supports GaN epi-wafer startups through Clean-Tech credits, seeking to anchor value-add processes. Mexico's EMS clusters extend tariff-free access to the U.S. vehicle supply chain, stimulating rectifier and transient-voltage-suppressor assembly.

Europe targets more than 20% global production share by 2030, though audit findings warn of schedule risk given permitting delays and skilled-labor gaps. Nexperia's USD 200 million Hamburg investment broadens European SiC capacity, while Poland secures Intel's post-fab testing center that creates 2,000 roles. The Middle East and Africa remain nascent but see pilot solar-inverter fabs in the UAE that specify 1200 V SiC diodes.

- Central Semiconductor Corp.

- Diodes Incorporated

- MinebeaMitsumi Power Semiconductor Device Inc.

- Infineon Technologies AG

- Littelfuse Inc.

- MACOM Technology Solutions Holdings Inc.

- Nexperia BV

- onsemi

- Renesas Electronics Corp.

- ROHM Co. Ltd.

- Micross Components Inc.

- Vishay Intertechnology Inc.

- Toshiba Electronic Devices and Storage Corp.

- Mitsubishi Electric Corp.

- Microchip Technology Inc.

- Semikron Danfoss

- Shindengen Electric Manufacturing Co. Ltd.

- STMicroelectronics NV

- Panasonic Holdings Corp.

- Texas Instruments Inc.

- Kyocera AVX Components Corp.

- Skyworks Solutions Inc.

- Cree - Wolfspeed Inc.

- Alpha and Omega Semiconductor Ltd.

- GlobalFoundries Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digitization of consumer electronics ecosystems

- 4.2.2 Acceleration of EV production and on-board chargers

- 4.2.3 5G rollout driving demand for RF and microwave diodes

- 4.2.4 Data-center efficiency mandates boosting power diodes

- 4.2.5 Regulatory tailwinds for GaN-on-Si high-voltage diodes

- 4.2.6 E-waste recycling laws increasing replacement rates

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility (Si, GaAs, GaN)

- 4.3.2 Thermal limitations in high-current packages

- 4.3.3 Patent congestion in WBG semiconductor processes

- 4.3.4 Regional capacity imbalance from localization policies

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Schottky Diodes

- 5.1.2 Zener Diodes

- 5.1.3 Rectifier Diodes

- 5.1.4 Laser Diodes

- 5.1.5 Small-Signal Diodes

- 5.1.6 Electrostatic Discharge Protection Diodes

- 5.1.7 Transient Voltage Suppressor Diodes

- 5.1.8 RF and Microwave Diodes

- 5.2 By End-User Industry

- 5.2.1 Communications

- 5.2.2 Consumer Electronics

- 5.2.3 Automotive

- 5.2.4 Defense and Aerospace

- 5.2.5 Computer and Peripherals

- 5.2.6 Industrial

- 5.2.7 Lighting

- 5.2.8 Other End-User Industries

- 5.3 By Mounting - Package

- 5.3.1 Through-Hole

- 5.3.2 Surface-Mount (SMD)

- 5.3.3 Chip-Scale Package

- 5.3.4 Flip-Chip

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Russia

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 South-East Asia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Egypt

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank - Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Central Semiconductor Corp.

- 6.4.2 Diodes Incorporated

- 6.4.3 MinebeaMitsumi Power Semiconductor Device Inc.

- 6.4.4 Infineon Technologies AG

- 6.4.5 Littelfuse Inc.

- 6.4.6 MACOM Technology Solutions Holdings Inc.

- 6.4.7 Nexperia BV

- 6.4.8 onsemi

- 6.4.9 Renesas Electronics Corp.

- 6.4.10 ROHM Co. Ltd.

- 6.4.11 Micross Components Inc.

- 6.4.12 Vishay Intertechnology Inc.

- 6.4.13 Toshiba Electronic Devices and Storage Corp.

- 6.4.14 Mitsubishi Electric Corp.

- 6.4.15 Microchip Technology Inc.

- 6.4.16 Semikron Danfoss

- 6.4.17 Shindengen Electric Manufacturing Co. Ltd.

- 6.4.18 STMicroelectronics NV

- 6.4.19 Panasonic Holdings Corp.

- 6.4.20 Texas Instruments Inc.

- 6.4.21 Kyocera AVX Components Corp.

- 6.4.22 Skyworks Solutions Inc.

- 6.4.23 Cree - Wolfspeed Inc.

- 6.4.24 Alpha and Omega Semiconductor Ltd.

- 6.4.25 GlobalFoundries Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment