PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940782

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940782

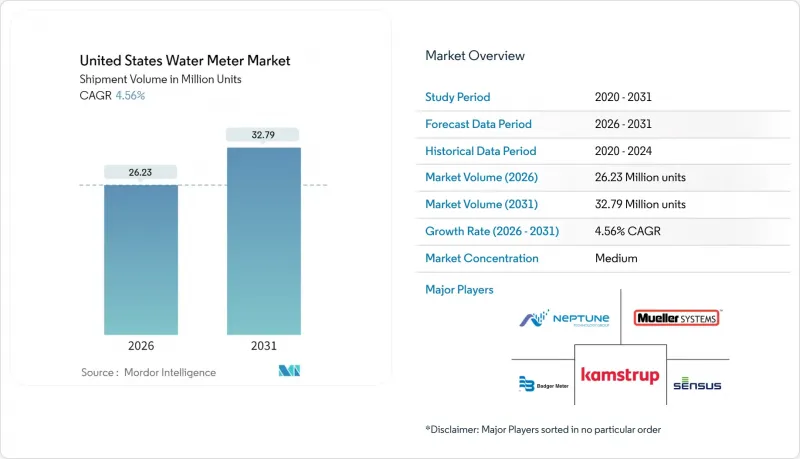

United States Water Meter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The US water meter market was valued at 25.09 million units in 2025 and estimated to grow from 26.23 million units in 2026 to reach 32.79 million units by 2031, at a CAGR of 4.56% during the forecast period (2026-2031).

Continued federal funding, drought-driven conservation requirements, and the shift from reactive maintenance to predictive asset management are sustaining this upward trajectory. Utilities are prioritizing advanced metering to curb non-revenue water, satisfy regulatory reporting mandates, and build data platforms that support broader smart-city objectives. Vendor strategies now emphasize integrated hardware-plus-analytics offerings that demonstrate measurable operational gains, creating differentiated value beyond initial meter cost. Communication technology innovation, especially cellular NB-IoT and LTE-M, has lowered deployment barriers in rural territories, widening the addressable base for next-generation meters.

United States Water Meter Market Trends and Insights

Aging Water Infrastructure Replacement Cycle

Chronic pipe failures, 250,000 breaks each year, have pushed utilities toward full-scale asset renewal, including meter fleets that date to the 1990s. End-of-life mechanical meters provide an opportune touch-point to install ultrasonic devices that stay in calibration for 20 years, lowering total lifecycle cost. Concurrent retirements of veteran operators intensify the need for automated data capture that substitutes analytics for shrinking field expertise. As replacement programs synchronize with federal grants, utilities are skipping like-for-like swaps and deploying smart infrastructure that future-proofs networks for decades.

Federal IIJA Funds Tied to Meter Upgrades

The Infrastructure Investment and Jobs Act earmarks USD 55 billion for water projects, and its eligibility criteria explicitly reward utilities that deploy metering technologies capable of documenting efficiency improvements. This is a paradigm shift from earlier federal programs centered on treatment plants. Two-way metering now serves as the compliance dashboard for equitable-investment goals, forcing grant applicants to prove quantifiable gains in distribution-system performance and customer service benchmarks that mechanical meters cannot supply.

Up-Front CAPEX Burden on Small Utilities

Utilities serving fewer than 3,300 connections confront per-meter costs exceeding USD 500, double the figure for large utilities, because they lack purchasing scale and internal project teams. Traditional bond financing is often off-limits owing to limited debt capacity. Metering-as-a-Service contracts, where vendors retain ownership and bill a monthly fee, have emerged as viable alternatives that shift capital outlays into operating budgets and transfer performance risk to suppliers.

Other drivers and restraints analyzed in the detailed report include:

- Utility Push to Cut Non-Revenue Water

- Smart-City and IoT Adoption Wave

- Cybersecurity and Data-Privacy Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Smart water meters are expanding at a 5.53% CAGR, even though mechanical devices still held 64.15% of the US water meter market share in 2025. Utilities value ultrasonic accuracy, integrated leak detection, and remote firmware updates that cut truck rolls. Kamstrup's flowIQ 2200 captures roughly 6 gallons per home per day previously unregistered by mechanical meters. The Las Vegas Valley Water District's evaluation of 400,000 residential replacements illustrates how operational savings offset higher unit prices within five years. Meanwhile, mechanical meters persist in capital-constrained districts that prioritize low first cost over data intelligence, but replacement cycles will eventually expose these utilities to the same performance gap.

The US water meter market size for smart meters is expected to reach 14.47 million units by 2031, supported by federal grant structures that tie funding to demonstrable efficiency metrics. Ultrasonic platforms retain calibration over life, trimming maintenance budgets in contrast to mechanical components that drift and demand periodic bench testing. This reliability advantage resonates with utilities facing workforce attrition; fewer meter repairs translate into lower staffing needs. As smart-city platforms incorporate water data, the strategic relevance of real-time consumption insight will keep eroding the mechanical installed base.

Automated Meter Reading held 57.12% of the US water meter market size in 2025, yet Advanced Metering Infrastructure is posting the fastest growth at 6.05% as utilities migrate to two-way architectures. AMI supports interval data granularity, remote disconnects, and network-wide firmware updates, creating a holistic asset-management environment. Tacoma Public Utilities leveraged AMI to roll out time-of-day pricing and achieved measurable consumption shifts within six months.

Utility executives also cite regulatory compliance: many state commissions now require hourly or daily reads to validate drought-response plans. AMR will remain relevant in low-density territories, but chipset cost reductions and cellular coverage expansion are narrowing the cost gap. Over the forecast horizon, AMI's market proposition of real-time situational awareness aligns with the industry push to manage non-revenue water proactively, ensuring continued share gains.

The United States Water Meter Market is Segmented by Meter Type (Smart Water Meter and Mechanical/Basic Meter), Communication Technology (Advanced Metering Infrastructure, Automated Meter Reading, and Manual/Walk-by), Network Connectivity (Cellular, RF-Mesh/900 MHz, and PLC/Wired), End-User Sector (Residential, and More), Utility Size Tier (Tier-1, Tier-2, and Tier-3). The Market Forecasts are Provided in Terms of Volume (Units).

List of Companies Covered in this Report:

- Badger Meter, Inc.

- Sensus USA Inc.

- Neptune Technology Group Inc.

- Mueller Systems, LLC

- Kamstrup Water Metering LLC

- Diehl Metering LLC USA

- Itron, Inc.

- Aclara Technologies LLC

- Landis+Gyr Technology Inc.

- Master Meter, Inc.

- Zenner USA, Inc.

- Metron-Farnier, LLC

- Carlon Meter, Inc.

- Elster AMCO Water, LLC

- Datamatic, Inc.

- Spire Metering Technology, LLC

- Arad Technologies USA, Inc.

- Honeywell International Inc.

- Xylem Inc.

- B Meters USA, Inc.

- Trimble Water, Inc.

- SmartCover Systems, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Supportive state regulations and conservation mandates

- 4.2.2 Aging water infrastructure replacement cycle

- 4.2.3 Utility push to cut non-revenue water

- 4.2.4 Smart-city and IoT adoption wave

- 4.2.5 NB-IoT coverage enabling rural roll-outs

- 4.2.6 Federal IIJA funds tied to meter upgrades

- 4.3 Market Restraints

- 4.3.1 Up-front CAPEX burden on small utilities

- 4.3.2 Cyber-security and data-privacy risks

- 4.3.3 Chip-supply volatility for ultrasonic meters

- 4.3.4 Utility workforce analytics skill-gap

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

- 4.8 Impact of Macroeconomic Trends

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Meter Type

- 5.1.1 Smart Water Meter

- 5.1.2 Mechanical/Basic Meter

- 5.2 By Communication Technology

- 5.2.1 Advanced Metering Infrastructure (AMI)

- 5.2.2 Automated Meter Reading (AMR)

- 5.2.3 Manual/Walk-by

- 5.3 By Network Connectivity

- 5.3.1 Cellular (LTE-M / NB-IoT)

- 5.3.2 RF-Mesh / 900 MHz

- 5.3.3 PLC/Wired

- 5.4 By End-User Sector

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.4.4 Municipal Utilities

- 5.5 By Utility Size Tier

- 5.5.1 Tier-1 (>400 k connections)

- 5.5.2 Tier-2 (45 k - 400 k)

- 5.5.3 Tier-3 (<45 k)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Analysis

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Badger Meter, Inc.

- 6.4.2 Sensus USA Inc.

- 6.4.3 Neptune Technology Group Inc.

- 6.4.4 Mueller Systems, LLC

- 6.4.5 Kamstrup Water Metering LLC

- 6.4.6 Diehl Metering LLC USA

- 6.4.7 Itron, Inc.

- 6.4.8 Aclara Technologies LLC

- 6.4.9 Landis+Gyr Technology Inc.

- 6.4.10 Master Meter, Inc.

- 6.4.11 Zenner USA, Inc.

- 6.4.12 Metron-Farnier, LLC

- 6.4.13 Carlon Meter, Inc.

- 6.4.14 Elster AMCO Water, LLC

- 6.4.15 Datamatic, Inc.

- 6.4.16 Spire Metering Technology, LLC

- 6.4.17 Arad Technologies USA, Inc.

- 6.4.18 Honeywell International Inc.

- 6.4.19 Xylem Inc.

- 6.4.20 B Meters USA, Inc.

- 6.4.21 Trimble Water, Inc.

- 6.4.22 SmartCover Systems, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment