PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940801

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940801

Social Media Listening - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

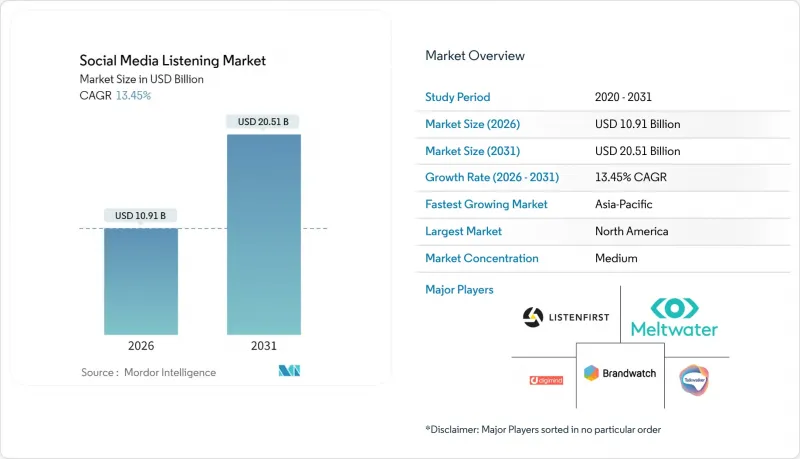

The social media listening market was valued at USD 9.62 billion in 2025 and estimated to grow from USD 10.91 billion in 2026 to reach USD 20.51 billion by 2031, at a CAGR of 13.45% during the forecast period (2026-2031).

The uptrend stems from enterprises shifting toward proactive engagement that relies on early sentiment signals captured on social platforms. North America retains leadership, aided by heightened brand-safety concerns following several high-profile crises, while Asia-Pacific records the steepest growth as localized platforms expand and smartphone adoption accelerates. Software remains the core investment category, although demand for expert services is climbing because firms need tailored workflows and AI model training. Text analytics still dominates, but video analytics is scaling quickly as short-form video overtakes text on many networks.

Global Social Media Listening Market Trends and Insights

Brand-risk Mitigation Amid Influencer-led Crises

Escalating financial fallout from influencer controversies is making real-time social intelligence indispensable for corporate risk teams. Brands with mature listening setups now detect brewing issues and respond 4.3 times faster than peers relying only on traditional monitoring, sharply limiting damage. Always-on alerts are being plugged into enterprise risk dashboards so PR, legal, and customer-care units can coordinate rapid remediation. Consumer-facing sectors feel the greatest urgency because a single viral post can erase months of equity building. The strategic shift elevates budget allocation for crisis-specific modules inside leading platforms. Vendors that embed predictive scoring and automated workflows gain preference among risk-averse buyers.

Generative-AI Sentiment Classification Boosting APAC Retail ROI

Large language models are rewriting sentiment analysis accuracy in markets where code-switching and slang frustrated legacy NLP. GPT-4 attains 93% precision on binary sentiment tasks, unlocking high-fidelity insights for multilingual regions. Retailers in Asia-Pacific quickly exploit the advance to fine-tune promotions and product tweaks. Cross-border sellers gain particular leverage because LLMs handle multiple Asian languages without separate analyst teams. Australian supplement maker Blackmores used WeChat-centric monitoring to spot rising consumer concerns and recast messaging, contributing to share gains in China. The ROI narrative accelerates adoption among e-commerce brands mindful of razor-thin margins.

Fragmented Data-Privacy Regimes

Divergent privacy statutes force vendors to juggle opt-outs, deletion rights, and data-residency mandates that vary by region. The California Consumer Privacy Act exemplifies the operational burden, requiring granular consumer controls and unique workflows for sensitive information. Smaller suppliers struggle to fund continuous rule updates, accelerating consolidation as compliance costs escalate. Enterprise buyers often deploy separate regional instances, diluting the value of unified global dashboards and dampening ROI expectations.

Other drivers and restraints analyzed in the detailed report include:

- Shift of TV Ad Spend to Social Video in Europe Raises SOV Analytics Demand

- Regulatory Response-Time Mandates for BFSI Complaints

- Multilingual AI Accuracy Gaps for Low-Resource Languages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for a 67.20% share of the social media listening market in 2025, cementing its role as the backbone of enterprise social intelligence stacks. Buyers prefer integrated suites that merge listening, engagement, and analytics so that insights flow directly into campaign orchestration tools. Platform vendors respond by embedding API layers that connect to customer data platforms and BI warehouses, supporting broader digital-experience strategies. The bundling trend protects license revenue even as basic monitoring commoditizes.

Services revenue, though smaller, is advancing at 16.02% CAGR because firms increasingly view social intelligence as an outcome-driven function rather than a plug-and-play toolset. Providers now offer crisis simulations, competitive war-rooms, and bespoke LLM fine-tuning that map to sector-specific jargon. Managed services resonate with mid-market brands lacking 24/7 coverage, while AI-tuning engagements carve a niche among regulated sectors that need domain-safe models. The dual-track growth keeps both pure-play and hybrid vendors relevant in the social media listening market.

Large enterprises commanded 64.10% of 2025 spending because they integrate listening outputs into data-lake architectures that span CRM, product, and compliance systems. Multi-brand conglomerates rely on dashboards that surface sentiment spikes per region, enabling coordinated rebuttal or campaign amplification. Enterprise buying cycles also drive consolidation as CIOs favor vendors offering contractual simplicity and ISO-certified security frameworks.

SMEs, however, represent the fastest-growing cohort with a projected 15.35% CAGR. Cloud pricing tiers, template-based onboarding, and conversational UI lower entry barriers. OECD research shows that 39% of SMEs used AI tools in 2025, up from 26% in 2024, mirroring broader digital acceleration. Small exporters pairing listening with social "talking" tactics report sharper customer gains, validating investment. Vendors target this segment with bundled freemium offerings that graduate to paid tiers once analytic depth and multiseat access become essential.

The Social Media Listening Market Report is Segmented by Component (Software, and Services), Organization Size (Large Enterprises, Small and Medium-Sized Enterprises), Analytics Type (Text Analytics, Image Analytics, and More), Application (Brand Health Tracking, Crisis Management, and More), Industry Vertical (Retail and E-Commerce, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained a 41.20% revenue lead in 2025, supported by technology maturity and stringent brand-protection postures following recent crises. Financial-services and healthcare firms integrate social data into regulated complaint systems to comply with statutes like the California Consumer Privacy Act, which grants consumers sweeping data rights. Ongoing investment focuses on high-precision risk detection modules that shield brand equity before posts trend.

Asia-Pacific is forecast to grow at 16.02% CAGR to 2031, propelled by soaring platform penetration and the dominance of mobile commerce. China's walled-garden networks oblige vendors to fine-tune language models and API connectors; brands that master this complexity, such as Blackmores on WeChat, unlock rapid share gains. India's rise combines smartphone affordability with regional-language social networks that demand multilingual coverage. Southeast Asian markets present high engagement but require dialect-adaptive NLP, keeping service partners busy.

Europe balances opportunity with heavy GDPR compliance overhead, spurring innovation in privacy-preserving analytics. The pivot of media budgets toward social video intensifies demand for multimodal share-of-voice dashboards. Latin America, the Middle East, and Africa are smaller yet dynamic, with growth centered in urban hubs and among multinationals that need regional sentiment gauges. Gulf governments increasingly adopt listening to track public opinion on service quality, expanding public-sector demand in the social media listening market.

- Meltwater

- Sprinklr

- Brandwatch (Cision LLC)

- NetBase Quid

- Talkwalker

- Digimind

- Khoros

- Clarabridge (Qualtrics)

- Mention

- Hootsuite Inc.

- Agorapulse

- Awario

- Zignal Labs

- ListenFirst

- Synthesio (Ipsos)

- Reputology

- Linkfluence

- Socialbakers (Astute)

- Keyhole Inc.

- Brand24

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Brand-risk mitigation amid influencer-led crises (North America)

- 4.2.2 Generative-AI sentiment classification boosting APAC retail ROI

- 4.2.3 Shift of TV ad spend to social video in Europe raises SOV analytics demand

- 4.2.4 Regulatory response-time mandates for BFSI complaints

- 4.2.5 Gaming and livestreaming surge generating rich video/audio data sets

- 4.2.6 Open-API martech ecosystems driving platform consolidation

- 4.3 Market Restraints

- 4.3.1 Fragmented data-privacy regimes (GDPR, CCPA, PDPA)

- 4.3.2 Multilingual AI accuracy gaps for low-resource languages

- 4.3.3 API access fee hikes from X (Twitter) and Meta

- 4.3.4 Overlap with in-house BI/CDP causing procurement fatigue

- 4.4 Technological Outlook

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Assessment of Macroeconomic Factors

5 Market Size and Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium-sized Enterprises (SMEs)

- 5.3 By Analytics Type

- 5.3.1 Text Analytics

- 5.3.2 Image Analytics

- 5.3.3 Video Analytics

- 5.3.4 Voice/Audio Analytics

- 5.4 By Application

- 5.4.1 Brand Health Tracking

- 5.4.2 Customer Experience Management

- 5.4.3 Competitive Benchmarking

- 5.4.4 Lead Generation and Sales Monitoring

- 5.4.5 Campaign Management

- 5.4.6 Crisis Management

- 5.5 By Industry Vertical

- 5.5.1 Retail and E-commerce

- 5.5.2 BFSI

- 5.5.3 IT and Telecom

- 5.5.4 Media and Entertainment

- 5.5.5 Healthcare and Life Sciences

- 5.5.6 Travel and Hospitality

- 5.5.7 Education

- 5.5.8 Others (Government, NGOs)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Nordics

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Southeast Asia

- 5.6.3.6 Australia and New Zealand

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 GCC Countries

- 5.6.5.2 Turkey

- 5.6.5.3 Israel

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Kenya

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Meltwater

- 6.4.2 Sprinklr

- 6.4.3 Brandwatch (Cision LLC)

- 6.4.4 NetBase Quid

- 6.4.5 Talkwalker

- 6.4.6 Digimind

- 6.4.7 Khoros

- 6.4.8 Clarabridge (Qualtrics)

- 6.4.9 Mention

- 6.4.10 Hootsuite Inc.

- 6.4.11 Agorapulse

- 6.4.12 Awario

- 6.4.13 Zignal Labs

- 6.4.14 ListenFirst

- 6.4.15 Synthesio (Ipsos)

- 6.4.16 Reputology

- 6.4.17 Linkfluence

- 6.4.18 Socialbakers (Astute)

- 6.4.19 Keyhole Inc.

- 6.4.20 Brand24

- 6.5 Vendor Positioning Matrix

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment