PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940826

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940826

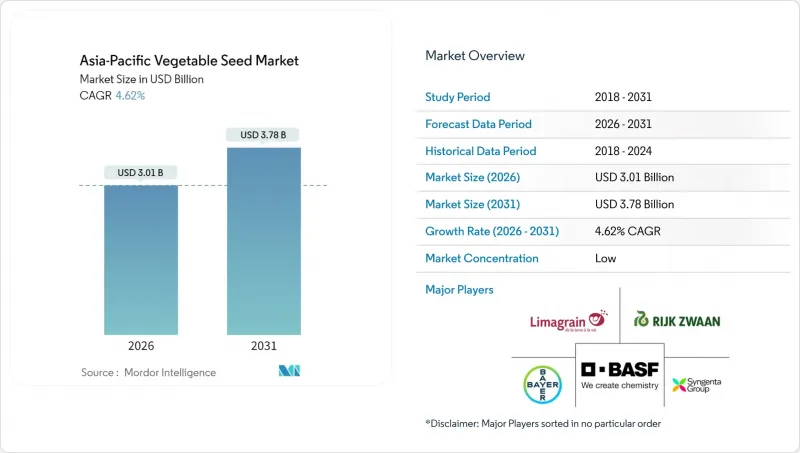

Asia-Pacific Vegetable Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Asia-Pacific vegetable seed market is expected to grow from USD 2.88 billion in 2025 to USD 3.01 billion in 2026 and is forecast to reach USD 3.78 billion by 2031 at 4.62% CAGR over 2026-2031.

Robust urban demand, expanding greenhouse infrastructure, and government support for hybrid technologies collectively underpin this steady expansion of the Asia-Pacific vegetable seed market. Multinational breeders focus on marker-assisted selection and genomic prediction to accelerate new-variety launch cycles, while regional firms emphasize cost-effective distribution to smallholders. Climate resilience traits dominate research pipelines as weather variability intensifies, and cross-border trade harmonization discussions inside ASEAN are creating fresh opportunities for streamlined seed movement. These dynamics position the Asia-Pacific vegetable seed market for sustained hybrid-driven transformation through 2030.

Asia-Pacific Vegetable Seed Market Trends and Insights

Rising Adoption of Hybrid Seeds for Yield and Quality Improvement

Hybrid penetration in commercial vegetable fields surpassed 80% in 2024, delivering 25-40% higher yields than open-pollinated lines and cutting post-harvest losses through improved shelf life.Demonstration plots funded by extension agencies in India and Thailand showcase tangible productivity gains, encouraging neighbor-to-neighbor diffusion. Precision breeding shortens development cycles to five years, allowing firms to release pest-resilient hybrids before resistance breaks down. Credit programs that bundle seed and inputs further lower adoption barriers, strengthening the Asia-Pacific vegetable seed market.

Expansion of Protected and Greenhouse Cultivation Area

Protected cropping acreage grew 15% in 2024 as growers seek yield stability amid erratic monsoons. Declining film and automation costs improve investment payback for mid-scale farmers, while China alone now manages more than 4 million hectares under plastic-house or glasshouse structures. Seed companies respond with compact, disease-tolerant varieties that optimize plant density and photoperiod management. Year-round output from greenhouses lifts revenue streams and enlarges the Asia-Pacific vegetable seed market.

Fragmented and Stringent Seed/GMO Regulations

Approval timelines for new vegetable varieties range from six months in Thailand to three years in India, complicating regional launch strategies. Only Australia and the Philippines allow commercial GM vegetable cultivation, constraining monetization of advanced gene-editing breakthroughs. Compliance duplication inflates R&D costs by up to 25%, dragging on the Asia-Pacific vegetable seed market.

Other drivers and restraints analyzed in the detailed report include:

- Government Horticulture Programs and Seed Subsidies

- Health-Driven Demand for Nutrient-Dense Vegetables

- Counterfeit and Sub-Standard Seed Circulation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid lines accounted for 75.10% of the Asia-Pacific vegetable seed market size in 2025 and are set to retain leadership with a 4.85% CAGR toward 2031. Yield premiums between 25% and 40% remain compelling for commercial growers facing land scarcity, even though initial seed costs run three to five times higher than open-pollinated alternatives. Intellectual property enforcement underpins sustainable royalty streams, giving multinational firms a clear incentive to invest in proprietary parent lines that cannot be farm-saved. Rapid genomic prediction and double-haploid techniques shorten product cycles to five or six years, enabling companies to react quickly to emerging pest pressures and maintain market relevance within the Asia-Pacific vegetable seed market.

Open-pollinated varieties continue to serve subsistence growers and organic producers who value seed-saving autonomy and lower cash outlays. Public-sector institutions frequently distribute these varieties through development programs, ensuring baseline seed access where commercial channels remain underdeveloped. Nevertheless, hybrid penetration advances wherever cold-chain expansion and supermarket procurement demand uniformity and shelf life advantages. As credit availability broadens and planting material financing products scale, the Asia-Pacific vegetable seed industry is likely to convert remaining open-pollinated acreage to high-performance hybrids over the next decade.

The Asia-Pacific Vegetable Seed Market Report is Segmented by Breeding Technology (Hybrids, Open Pollinated Varieties, and Hybrid Derivatives), Cultivation Mechanism (Open Field, Protected Cultivation), Crop Family (Solanaceae, Brassicas, Cucurbits, and More), and Country (Australia, Bangladesh, China, India, Indonesia, Japan, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- Bayer AG

- Syngenta Group

- BASF SE

- Advanta Seeds (UPL Limited)

- East-West Seed

- Sakata Seed Corporation

- Rijk Zwaan Zaadteelt en Zaadhandel BV

- Groupe Limagrain

- Corteva Agriscience

- Enza Zaden Holding BV

- Bejo Zaden BV

- Takii and Co., Ltd.

- Namdhari Seeds Pvt. Ltd.

- Maharashtra Hybrid Seeds Company Private Limited (Mahyco Private Limited)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Vegetables

- 4.2 Most Popular Traits

- 4.2.1 Cabbage and Lettuce

- 4.2.2 Tomato and Chilli

- 4.3 Breeding Techniques

- 4.3.1 Vegetables

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Rising adoption of hybrid seeds for yield and quality improvement

- 4.6.2 Expansion of protected and greenhouse cultivation area

- 4.6.3 Government horticulture programs and seed subsidies

- 4.6.4 Health-driven demand for nutrient-dense vegetables

- 4.6.5 Urban vertical farming driving micro-dwarf seed demand

- 4.6.6 Blockchain-enabled seed traceability premiums

- 4.7 Market Restraints

- 4.7.1 Fragmented and stringent seed/GMO regulations

- 4.7.2 Counterfeit and sub-standard seed circulation

- 4.7.3 Climate-driven pollinator variability affecting seed yields

- 4.7.4 Narrow genetic base raising disease-susceptibility costs

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.2 Open Pollinated Varieties and Hybrid Derivatives

- 5.2 Cultivation Mechanism

- 5.2.1 Open Field

- 5.2.2 Protected Cultivation

- 5.3 Crop Family

- 5.3.1 Brassicas

- 5.3.1.1 Cabbage

- 5.3.1.2 Carrot

- 5.3.1.3 Cauliflower and Broccoli

- 5.3.1.4 Other Brassicas

- 5.3.2 Cucurbits

- 5.3.2.1 Cucumber and Gherkin

- 5.3.2.2 Pumpkin and Squash

- 5.3.2.3 Other Cucurbits

- 5.3.3 Roots and Bulbs

- 5.3.3.1 Garlic

- 5.3.3.2 Onion

- 5.3.3.3 Potato

- 5.3.3.4 Other Roots and Bulbs

- 5.3.4 Solanaceae

- 5.3.4.1 Chilli

- 5.3.4.2 Eggplant

- 5.3.4.3 Tomato

- 5.3.4.4 Other Solanaceae

- 5.3.5 Unclassified Vegetables

- 5.3.5.1 Asparagus

- 5.3.5.2 Lettuce

- 5.3.5.3 Okra

- 5.3.5.4 Peas

- 5.3.5.5 Spinach

- 5.3.5.6 Other Unclassified Vegetables

- 5.3.1 Brassicas

- 5.4 Country

- 5.4.1 Australia

- 5.4.2 Bangladesh

- 5.4.3 China

- 5.4.4 India

- 5.4.5 Indonesia

- 5.4.6 Japan

- 5.4.7 Myanmar

- 5.4.8 Pakistan

- 5.4.9 Philippines

- 5.4.10 Thailand

- 5.4.11 Vietnam

- 5.4.12 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bayer AG

- 6.4.2 Syngenta Group

- 6.4.3 BASF SE

- 6.4.4 Advanta Seeds (UPL Limited)

- 6.4.5 East-West Seed

- 6.4.6 Sakata Seed Corporation

- 6.4.7 Rijk Zwaan Zaadteelt en Zaadhandel BV

- 6.4.8 Groupe Limagrain

- 6.4.9 Corteva Agriscience

- 6.4.10 Enza Zaden Holding BV

- 6.4.11 Bejo Zaden BV

- 6.4.12 Takii and Co., Ltd.

- 6.4.13 Namdhari Seeds Pvt. Ltd.

- 6.4.14 Maharashtra Hybrid Seeds Company Private Limited (Mahyco Private Limited)

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS