PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940836

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940836

Specialty Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

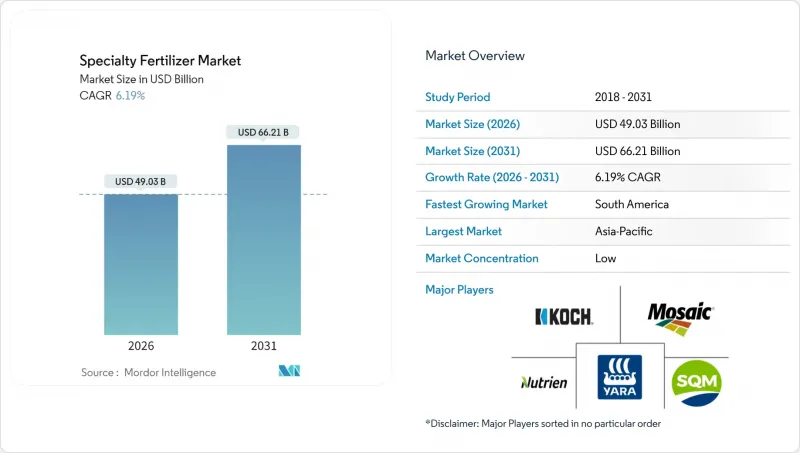

The specialty fertilizers market was valued at USD 46.17 billion in 2025 and estimated to grow from USD 49.03 billion in 2026 to reach USD 66.21 billion by 2031, at a CAGR of 6.19% during the forecast period (2026-2031).

The adoption of precision farming tools propels market growth, driven by the rapid shift toward enhanced-efficiency formulations and policy support that links nutrient management with environmental metrics. Liquid products dominate because their full solubility matches fertigation needs, while technology improvements in controlled-release coatings keep nutrient availability synchronized with crop demand. Digital agriculture platforms provide real-time field data that enhances nutrient use efficiency, promotes regulatory compliance, and facilitates carbon-credit monetization. Expanding protected cultivation, increasing drip irrigation coverage, and offering incentives for nitrogen use efficiency enhance demand resiliency across crop categories. Competitive intensity hinges on integrated service models that bundle analytics, hardware, and tailored nutrient solutions to raise farm profitability in the specialty fertilizers market.

Global Specialty Fertilizer Market Trends and Insights

Precision-Agriculture Adoption

Satellite imagery, soil sensors, and GPS-guided spreaders are enhancing the accuracy of nutrient placement. In 2024, the majority of corn and soybean growers adopted variable-rate application, compared to 2023, and specialty fertilizer use per acre increased as the broadcast practice declined. Real-time nitrogen crediting triggers on-demand blended inputs that match crop stages, cutting losses and bolstering yields. Equipment firms now co-design multi-bin applicators with nutrient suppliers, letting farmers switch formulations without downtime. Supportive conservation programs cover part of the hardware cost, thereby accelerating the penetration of precision-ready, enhanced-efficiency products.

Water Scarcity and Irrigation Efficiency

Drip irrigation, paired with fertigation, reduces water use compared to flood systems, a critical benefit as agriculture's share of freshwater resources contracts. Global acreage under drip lines reached a higher level in 2024, and specialty fertilizer volumes through these networks doubled those of conventional field methods. Israel and Jordan mandate pressurized irrigation for new farms larger than 10 ha, creating locked-in demand for fully soluble nutrient blends. Online pH and conductivity probes require low-salt index products that remain clog-free. Subsidies linked to water use targets favor fertigation and support the growth of the specialty fertilizers market.

Raw-Material and Energy Price Volatility

Natural gas, potash, and phosphate rock prices fluctuated in 2024 amid geopolitical tensions, compressing producer margins. Polymer coatings, which account for up to 25% of CRF costs, track crude oil, so oil spikes translate quickly into higher finished product prices. Potash supply disruptions from Russia and Belarus led to spot costs increasing by 50% at times, prompting alternative sourcing. Single-supplier dependence for specialty additives magnifies risk, and currency shifts add further uncertainty for import-reliant manufacturers. Short procurement cycles leave little room for hedging, making price stability elusive.

Other drivers and restraints analyzed in the detailed report include:

- Greenhouse and Vertical-Farm Expansion

- Digital Traceability Premiums

- Emerging Micro-Plastic Coating Bans

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid fertilizers accounted for 53.38% of the specialty fertilizers market share in 2025, a position built on their unmatched compatibility with fertigation and uniform nutrient distribution. Their rapid dissolution and ease of blending suit variable-rate rigs that demand precise homogeneity. Adoption of large irrigated acreage across the Asia Pacific and South America keeps volumes high, while indoor farming values its low salt risk. The segment also benefits from an expanded distribution infrastructure that supports bulk shipments and on-farm blending.

The specialty fertilizers market size for controlled-release products is projected to expand at a 7.81% CAGR, the fastest among specialty types. Coating advances offer predictable nutrient release curves that align with crop uptake, thereby curbing leaching and reducing labor requirements. Polymer-sulfur variants gain traction in sulfur-deficient regions, and biodegradable films help satisfy looming microplastic laws. Precision agriculture tools amplify value, as one application now feeds a crop across multiple growth stages, improving return on investment.

The Specialty Fertilizer Market is Segmented by Specialty Type (CRF, Liquid Fertilizer, SRF, Water Soluble), by Application Mode (Fertigation, Foliar, Soil), by Crop Type (Field Crops, Horticultural Crops, Turf and Ornamental), and by Region (Asia-Pacific, Europe, Middle East and Africa, North America, and South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Geography Analysis

Asia Pacific commanded 65.20% of global revenue in 2025, supported by China's soil testing subsidies and India's specialty nutrient incentives for smallholders. Intensive land use in Japan and South Korea further propels per-hectare spending, while Australia's drought management rules promote the use of fertigation systems with liquid blends. Southeast Asian palm and rice producers adopt enhanced-efficiency inputs to comply with sustainability certifications, adding incremental volume.

South America represents the fastest-growing region with an 8.55% CAGR to 2031. Brazil has initiated investments in precision agriculture technologies that enhance nutrient efficiency, and large farms are aligning CRF usage with no-till practices to safeguard soil health. Argentina mirrors this trajectory, utilizing controlled-release solutions for soy and corn to maintain export competitiveness amid growing environmental scrutiny.

The South American specialty fertilizer market is characterized by large-scale agricultural operations and growing adoption of modern farming practices. The region, primarily represented by Brazil and Argentina, shows significant market potential driven by extensive agricultural lands and diverse crop portfolios. Brazil emerges as the largest market in the region, supported by its vast agricultural operations and strong focus on technological advancement in farming. Argentina stands as the fastest-growing market, driven by increasing adoption of precision farming techniques and a focus on export-oriented agriculture. The region's market is characterized by growing awareness about sustainable farming practices and increasing investments in agricultural technology.

- Coromandel International Limited

- EuroChem Group AG

- COMPO EXPERT GmbH

- Haifa Group

- Kingenta Ecological Engineering Group Co., Ltd.

- Koch Fertilizer LLC

- Nutrien Ltd.

- Sociedad Quimica y Minera de Chile S.A.

- The Mosaic Company

- Yara International ASA

- ICL Group Ltd.

- K+S Aktiengesellschaft

- Indian Farmers Fertiliser Cooperative Ltd.

- Omex Agriculture Ltd.

- Agro-Culture Liquid Fertilizers LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped for Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Precision-agriculture adoption

- 4.6.2 Water scarcity and irrigation efficiency

- 4.6.3 Greenhouse and vertical-farm expansion

- 4.6.4 Carbon-credit incentives for NUE inputs

- 4.6.5 CRISPR-enabled nutrient-dense crops

- 4.6.6 Digital traceability premiums

- 4.7 Market Restraints

- 4.7.1 Raw-material and energy price volatility

- 4.7.2 High capex of fertigation hardware

- 4.7.3 Emerging micro-plastic coating bans

- 4.7.4 Data-standard gaps for carbon accounting

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Specialty Type

- 5.1.1 Controlled-Release Fertilizer (CRF)

- 5.1.1.1 Polymer Coated

- 5.1.1.2 Polymer-Sulfur Coated

- 5.1.1.3 Others

- 5.1.2 Liquid Fertilizer

- 5.1.3 Slow-Release Fertilizer (SRF)

- 5.1.4 Water-Soluble

- 5.1.1 Controlled-Release Fertilizer (CRF)

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf and Ornamental

- 5.4 Region

- 5.4.1 Asia-Pacific

- 5.4.1.1 Australia

- 5.4.1.2 Bangladesh

- 5.4.1.3 China

- 5.4.1.4 India

- 5.4.1.5 Indonesia

- 5.4.1.6 Japan

- 5.4.1.7 Pakistan

- 5.4.1.8 Philippines

- 5.4.1.9 Thailand

- 5.4.1.10 Vietnam

- 5.4.1.11 Rest of Asia-Pacific

- 5.4.2 Europe

- 5.4.2.1 France

- 5.4.2.2 Germany

- 5.4.2.3 Italy

- 5.4.2.4 Netherlands

- 5.4.2.5 Russia

- 5.4.2.6 Spain

- 5.4.2.7 Ukraine

- 5.4.2.8 United Kingdom

- 5.4.2.9 Rest of Europe

- 5.4.3 Middle East and Africa

- 5.4.3.1 Nigeria

- 5.4.3.2 Saudi Arabia

- 5.4.3.3 South Africa

- 5.4.3.4 Turkey

- 5.4.3.5 Rest of Middle East and Africa

- 5.4.4 North America

- 5.4.4.1 Canada

- 5.4.4.2 Mexico

- 5.4.4.3 United States

- 5.4.4.4 Rest of North America

- 5.4.5 South America

- 5.4.5.1 Argentina

- 5.4.5.2 Brazil

- 5.4.5.3 Rest of South America

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Coromandel International Limited

- 6.4.2 EuroChem Group AG

- 6.4.3 COMPO EXPERT GmbH

- 6.4.4 Haifa Group

- 6.4.5 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.6 Koch Fertilizer LLC

- 6.4.7 Nutrien Ltd.

- 6.4.8 Sociedad Quimica y Minera de Chile S.A.

- 6.4.9 The Mosaic Company

- 6.4.10 Yara International ASA

- 6.4.11 ICL Group Ltd.

- 6.4.12 K+S Aktiengesellschaft

- 6.4.13 Indian Farmers Fertiliser Cooperative Ltd.

- 6.4.14 Omex Agriculture Ltd.

- 6.4.15 Agro-Culture Liquid Fertilizers LLC

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS