PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940874

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940874

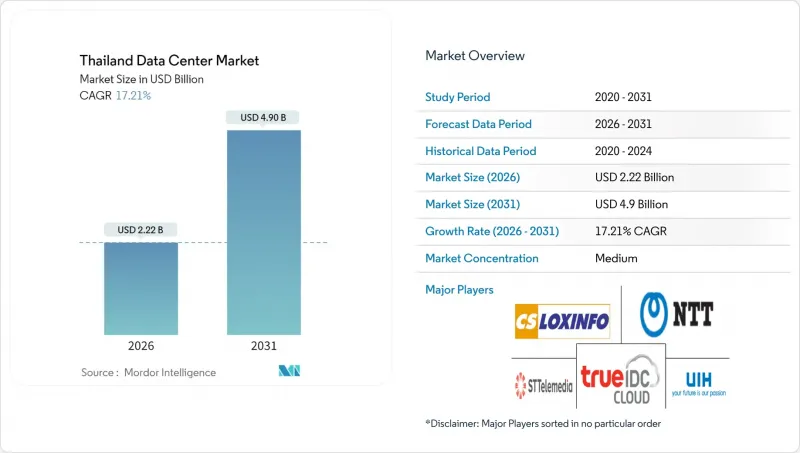

Thailand Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Thailand Data Center Market was valued at USD 1.89 billion in 2025 and estimated to grow from USD 2.22 billion in 2026 to reach USD 4.9 billion by 2031, at a CAGR of 17.21% during the forecast period (2026-2031).

In terms of market size, the market is expected to grow from 0.77 thousand megawatt in 2025 to 2.93 thousand megawatt by 2030, at a CAGR of 30.60% during the forecast period (2025-2030). The market segment shares and estimates are calculated and reported in terms of MW. Hyperscaler capital commitments, Thailand 4.0 policy incentives, and aggressive submarine-cable builds underpin the expansion, while grid modernization and progressive renewable-energy purchase rules sustain operator confidence. Enterprise cloud migration accelerated AI adoption, and edge buildouts in the Eastern Economic Corridor (EEC) further strengthen demand. Competition intensifies as global platforms enter, spurring facility upgrades in rack density, liquid cooling, and carrier-neutral interconnection.

Thailand Data Center Market Trends and Insights

Rising Cloud-First Digital Transformation Mandates Among Thai Enterprises

Continuous state-backed digital policies now oblige corporations to host regulated workloads in-country. The Board of Investment grants up to 13-year income-tax holidays on projects above THB 750 million (USD 21.7 million) that add local compute, lowering the effective total cost of ownership. Manufacturers such as Midea run 5G-enabled smart factories in the EEC that depend on proximate edge nodes for real-time quality control. Mergers in fixed broadband, notably AIS-3BB, lift access speeds and hasten enterprise cloud adoption. Carrier-neutral sites with dense on-ramps therefore secure long-term contracts despite premium pricing.

Aggressive Submarine-Cable Investments Enhancing International Connectivity

New trans-Asian systems shorten round-trip latency to Singapore, Hong Kong, and Tokyo below 10 milliseconds, enabling content, fintech, and SaaS firms to anchor regional workloads inside Bangkok. Hyperscalers cite bandwidth gains as the precondition for launching sovereign cloud regions, which cascade demand into wholesale colocation halls requiring triple-path fiber and dark-fiber diversity. Better throughput also lets Thai operators serve neighbouring Mekong markets from domestic hubs, opening wholesale revenue streams.

Land Scarcity and Soaring Bangkok Real-Estate Costs

Prime plots inside Bangkok's carrier hotels and CBD corridors command record premiums that squeeze multi-tenant operators on expansion budgets. Hyperscalers leverage deeper balance sheets to pre-empt entire industrial parks, leaving colocators to retrofit vertical extensions or migrate capacity to outer provinces. Resultant site hunts add months to project lead-times and compel higher rack-density strategies to lift revenue per square meter.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives Under Thailand 4.0 Driving Data Localization

- Surge in AI and High-Density Computing Workloads Requiring Hyperscale Capacity

- Chronic Grid Stability Issues Outside Primary Metro Areas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medium facilities accounted for a notable slice of the Thailand data center market size, growing at 17.95% CAGR as enterprises and telecom carriers prioritize low-latency zones closer to users. Large campuses hold economies of scale and captured 26.35% of Thailand data center market share in 2025, but their downtown land constraints limit additional expansion.

Operators replicate standardized 6-12 MW blueprints in provincial industrial estates, aligning with 5G edge computing rollouts by Advanced Info Service that anchor private network cores near manufacturing clusters. The pattern lowers transport latency for factory automation and drives diverse demand beyond Bangkok.

Tier 3 specifications represented 85.62% of Thailand data center market share in 2025, demonstrating enterprise comfort with 99.982% uptime at more practical price points than Tier 4. Upgrades to support high-density AI racks fuel a 18.88% CAGR for Tier 3 builds over 2026-2031.

Colocation providers enhance redundancy via modular power trains and hot-swap chillers rather than shifting to full Tier 4, preserving capex discipline. STT GDC's Frost and Sullivan award spotlights operational excellence inside Tier 3 footprints optimized for liquid immersion cooling demand.

The Thailand Data Center Market Report is Segmented by Data Center Size (Large, Massive, Medium, Mega, and Small), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Type (Hyperscale/Self-built, Enterprise/Edge, and Colocation), End User (BFSI, IT and ITES, E-Commerce, Government, Manufacturing, Media and Entertainment, Telecom, and More), and Hotspot. The Market Forecasts are Provided in Terms of IT Load Capacity (MW).

List of Companies Covered in this Report:

- Huawei Cloud Computing Technologies Co., Ltd.

- True Internet Data Center Co., Ltd.

- China Mobile Limited (SUPERNAP Thailand)

- Advanced Info Service PLC (CS LoxInfo)

- STT GDC Pte Ltd.

- Alibaba Cloud

- OneAsia Network Ltd.

- Internet Thailand Public Company Ltd.

- National Telecom Public Company Ltd.

- Telehouse International Corporation of Europe Ltd.

- United Information Highway Co., Ltd.

- TCC Technology Co., Ltd.

- Bridge Data Centres (Chindata Group)

- KT Corporation with Jasmine Group

- Etix Everywhere

- NTT Global Data Centers (Thailand) Ltd.

- Equinix Inc.

- Digital Realty Trust Inc.

- EdgeConneX Inc.

- Global Switch Holdings Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising cloud-first digital transformation mandates among Thai enterprises

- 4.2.2 Aggressive submarine cable investments enhancing international connectivity

- 4.2.3 Government incentives under Thailand 4.0 driving data localization

- 4.2.4 Surge in AI and high-density computing workloads requiring hyperscale capacity

- 4.2.5 Edge deployments for Industry 4.0 corridors in Eastern Economic Corridor

- 4.2.6 Lucrative green-energy tariffs encouraging sustainable data center builds

- 4.3 Market Restraints

- 4.3.1 Land scarcity and soaring Bangkok real-estate costs

- 4.3.2 Chronic grid stability issues outside primary metro areas

- 4.3.3 Lengthy permitting and environmental approval cycles

- 4.3.4 Intensifying competition compressing colocation pricing margins

- 4.4 Market Outlook

- 4.4.1 IT Load Capacity

- 4.4.2 Raised Floor Space

- 4.4.3 Colocation Revenue

- 4.4.4 Installed Racks

- 4.4.5 Rack Space Utilization

- 4.4.6 Submarine Cable

- 4.5 Key Industry Trends

- 4.5.1 Smartphone Users

- 4.5.2 Data Traffic Per Smartphone

- 4.5.3 Mobile Data Speed

- 4.5.4 Broadband Data Speed

- 4.5.5 Fiber Connectivity Network

- 4.5.6 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (MEGAWATT)

- 5.1 By Data Center Size

- 5.1.1 Large

- 5.1.2 Massive

- 5.1.3 Medium

- 5.1.4 Mega

- 5.1.5 Small

- 5.2 By Tier Type

- 5.2.1 Tier 1 and 2

- 5.2.2 Tier 3

- 5.2.3 Tier 4

- 5.3 By Data Center Type

- 5.3.1 Hyperscale/Self-built

- 5.3.2 Enterprise/Edge

- 5.3.3 Colocation

- 5.3.3.1 Non-Utilized

- 5.3.3.2 Utilized

- 5.3.3.2.1 Retail Colocation

- 5.3.3.2.2 Wholesale Colocation

- 5.4 By End User

- 5.4.1 BFSI

- 5.4.2 IT and ITES

- 5.4.3 E-Commerce

- 5.4.4 Government

- 5.4.5 Manufacturing

- 5.4.6 Media and Entertainment

- 5.4.7 Telecom

- 5.4.8 Other End Users

- 5.5 By Hotspot

- 5.5.1 Bangkok

- 5.5.2 Rest of Thailand

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Huawei Cloud Computing Technologies Co., Ltd.

- 6.4.2 True Internet Data Center Co., Ltd.

- 6.4.3 China Mobile Limited (SUPERNAP Thailand)

- 6.4.4 Advanced Info Service PLC (CS LoxInfo)

- 6.4.5 STT GDC Pte Ltd.

- 6.4.6 Alibaba Cloud

- 6.4.7 OneAsia Network Ltd.

- 6.4.8 Internet Thailand Public Company Ltd.

- 6.4.9 National Telecom Public Company Ltd.

- 6.4.10 Telehouse International Corporation of Europe Ltd.

- 6.4.11 United Information Highway Co., Ltd.

- 6.4.12 TCC Technology Co., Ltd.

- 6.4.13 Bridge Data Centres (Chindata Group)

- 6.4.14 KT Corporation with Jasmine Group

- 6.4.15 Etix Everywhere

- 6.4.16 NTT Global Data Centers (Thailand) Ltd.

- 6.4.17 Equinix Inc.

- 6.4.18 Digital Realty Trust Inc.

- 6.4.19 EdgeConneX Inc.

- 6.4.20 Global Switch Holdings Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment