PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940880

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940880

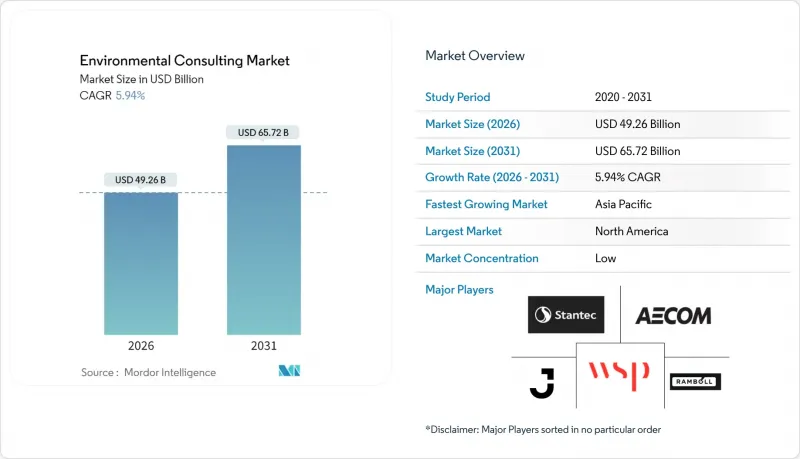

Environmental Consulting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The environmental consulting market was valued at USD 46.50 billion in 2025 and estimated to grow from USD 49.26 billion in 2026 to reach USD 65.72 billion by 2031, at a CAGR of 5.94% during the forecast period (2026-2031).

This sustained performance reflects synchronized climate-policy mandates across OECD and G20 economies, rising corporate disclosure obligations, and rapid digitization that compresses delivery costs while expanding advisory scope. Demand concentrates in high-value segments, particularly Environmental Impact Assessment and ESG advisory, because regulatory standardization turns compliance from discretionary spending into essential infrastructure. Corporate net-zero commitments, growth in green finance, and industrial decarbonization funds deepen the addressable pool of projects, while technology such as AI-enabled site characterization elevates consulting productivity. Competitive intensity remains balanced: specialized boutiques capture niche technical mandates, whereas large integrated players leverage cross-service synergies to defend margins despite framework fee pressure.

Global Environmental Consulting Market Trends and Insights

Mandatory Climate-Policy Compliance in OECD and G20 Economies

Converging climate rules transform consulting demand into a standardized, repeatable service line rather than episodic project work. Updated OECD Environmental Performance Reviews require quantified decarbonization pathways, while carbon-border adjustment mechanisms introduce supply-chain verification needs that transcend national boundaries.Consulting firms deploy single methodological frameworks across multiple jurisdictions, lowering customization costs and enlarging their client base. As compliance shifts from voluntary to mandatory, service pipelines become more predictable, enabling long-term resource planning and investment in digital delivery platforms.

Corporate Net-Zero and ESG Disclosure Mandates

The EU Corporate Sustainability Reporting Directive applies to more than 50,000 companies starting in 2024, compelling detailed environmental disclosures that exceed prior voluntary guidelines. Many firms lack in-house expertise to map operations to taxonomy criteria, producing a multi-year backlog of advisory assignments. Similar rules under consideration by the U.S. Securities and Exchange Commission and other regulators extend the same demand pattern globally. Consequently, environmental consulting market relationships migrate from short-term compliance engagements to continuous strategic partnerships that include scenario modeling and assurance readiness.

Persistent Fee-Pressure from Framework Contracts

Corporate buyers consolidate vendors under multiyear frameworks that embed annual cost-down clauses. Routine compliance tasks become commoditized, forcing consultants to diversify toward specialized, high-value niches such as PFAS remediation or nature-positive accounting. Larger firms leverage scale and cross-selling to defend margins, whereas smaller boutiques rely on unique technical depth to command premium rates.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Green and Transition Bonds Requiring 3rd-Party Verification

- Industrial Decarbonization Funds Tied to Advisory Spend

- Delayed Permitting for Large Infrastructure in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Environmental Impact Assessment captured 30.25% of the environmental consulting market in 2025, reflecting its entrenched role in project permitting across every major economy. Despite its scale, fee rates face pressure as standardized digital workflows shorten field programs. Conversely, ESG Reporting and Sustainability Strategy is forecast to increase at a 6.12% CAGR, propelled by mandatory disclosure rules that necessitate continuous rather than project-based engagement. The environmental consulting market size for climate-change consulting accelerates as transition pathway modeling becomes a board-level priority, positioning consultants as strategic advisors on capital allocation.

Water and wastewater management benefits from infrastructure stimulus and new contaminant regulations such as the EPA Lead and Copper Rule Improvements, which unlock USD 45 billion of addressable projects through 2030. Consultants specializing in PFAS remediation secure complex, multi-year assignments requiring hydrogeological expertise and advanced treatment design. Meanwhile, AI-driven contaminated-site assessment compresses traditional fieldwork yet opens new revenue streams in data analytics and remote sensing interpretation.

The Environmental Consulting Market Report is Segmented by Service Type (Climate Change Consulting, EHS, Environmental Impact Assessment, Water and Wastewater Management, and More), End-User Industry (Energy and Power, Mining and Metals, Public Sector, Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 35.53% of environmental consulting market share in 2025, leveraging mature rules such as the National Environmental Policy Act that underpin steady demand for impact assessments and remediation. Federal infrastructure packages add long-cycle projects focused on climate resilience, water systems, and grid renewal, enhancing revenue visibility. Emerging state-level climate disclosure bills further amplify advisory pipelines.

Asia-Pacific leads regional growth at a 6.31% CAGR through 2031. China's draft Ecological and Environmental Code consolidates fragmented regulations, compelling industrial operators to seek standardized consulting support. India's renewable-energy targets and Make-in-India manufacturing expansion elevate demand for environmental permitting, while Southeast Asian countries adopt carbon-pricing and ESG reporting frameworks. Consultants with local regulatory fluency and global technical resources gain first-mover advantage.

Europe maintains robust activity through the EU Taxonomy and Corporate Sustainability Reporting Directive, which institutionalize disclosure obligations for thousands of firms. Consultants export their experience to jurisdictions adopting similar frameworks, transforming European expertise into a global competitive asset. Middle East and Africa present pockets of high growth tied to megaprojects and emerging water scarcity solutions, though uneven regulatory enforcement tempers market velocity. Latin America benefits from mining investments and renewable build-out but continues to battle political volatility and elongated permitting.

- Jacobs Solutions Inc.

- AECOM

- WSP Global Inc.

- Tetra Tech, Inc.

- Stantec Inc.

- Ramboll Group A/S

- ERM International Group Limited

- Arup Group Limited

- GHD Group Pty Ltd

- Sweco AB

- Arcadis N.V.

- John Wood Group PLC (Wood)

- SNC-Lavalin Group Inc. (AtkinsRealis)

- HDR, Inc.

- SLR Consulting Limited

- Antea Group N.V.

- Mott MacDonald Group Limited

- Montrose Environmental Group, Inc.

- Brown and Caldwell, Inc.

- Worley Limited

- ICF International, Inc.

- EA Engineering, Science, and Technology, Inc., PBC

- Cardno Limited

- Golder Associates Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory Climate-Policy Compliance in OECD and G20 Economies

- 4.2.2 Corporate Net-Zero and ESG Disclosure Mandates

- 4.2.3 Growth of Green and Transition Bonds Requiring 3rd-Party Verification

- 4.2.4 Industrial Decarbonisation Funds Tied to Advisory Spend

- 4.2.5 AI-Enabled Rapid Site-Characterisation Tools Cut Due-Diligence Time

- 4.2.6 "Nature-Positive" Impact Accounting Frameworks Emerge

- 4.3 Market Restraints

- 4.3.1 Persistent Fee-Pressure from Framework Contracts

- 4.3.2 Delayed Permitting for Large Infrastructure in Emerging Markets

- 4.3.3 Scarcity of Licensed Hydro-geologists and Toxicologists

- 4.3.4 Client Shift to In-House Digital EHS Platforms

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of Macroeconomic Shocks

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Climate Change Consulting

- 5.1.2 EHS

- 5.1.3 Environmental Impact Assessment

- 5.1.4 Water and Wastewater Management

- 5.1.5 ESG Reporting and Sustainability Strategy

- 5.1.6 Other Service Types (Includes Contaminated Site Assessment)

- 5.2 By End-User Industry

- 5.2.1 Energy and Power

- 5.2.2 Mining and Metals

- 5.2.3 Public Sector

- 5.2.4 Manufacturing

- 5.2.5 Pharmaceuticals

- 5.2.6 Other End-user Industries (Construction and Infrastructure, Transportation, etc.)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Poland

- 5.3.3.7 Russia

- 5.3.3.8 Rest of Europe

- 5.3.4 Asia Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 South Korea

- 5.3.4.5 Australia

- 5.3.4.6 Rest of Asia Pacific

- 5.3.5 Middle East and Africa

- 5.3.5.1 Middle East

- 5.3.5.1.1 Saudi Arabia

- 5.3.5.1.2 United Arab Emirates

- 5.3.5.1.3 Turkey

- 5.3.5.1.4 Rest of Middle East

- 5.3.5.2 Africa

- 5.3.5.2.1 South Africa

- 5.3.5.2.2 Nigeria

- 5.3.5.2.3 Egypt

- 5.3.5.2.4 Rest of Africa

- 5.3.5.1 Middle East

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Jacobs Solutions Inc.

- 6.4.2 AECOM

- 6.4.3 WSP Global Inc.

- 6.4.4 Tetra Tech, Inc.

- 6.4.5 Stantec Inc.

- 6.4.6 Ramboll Group A/S

- 6.4.7 ERM International Group Limited

- 6.4.8 Arup Group Limited

- 6.4.9 GHD Group Pty Ltd

- 6.4.10 Sweco AB

- 6.4.11 Arcadis N.V.

- 6.4.12 John Wood Group PLC (Wood)

- 6.4.13 SNC-Lavalin Group Inc. (AtkinsRealis)

- 6.4.14 HDR, Inc.

- 6.4.15 SLR Consulting Limited

- 6.4.16 Antea Group N.V.

- 6.4.17 Mott MacDonald Group Limited

- 6.4.18 Montrose Environmental Group, Inc.

- 6.4.19 Brown and Caldwell, Inc.

- 6.4.20 Worley Limited

- 6.4.21 ICF International, Inc.

- 6.4.22 EA Engineering, Science, and Technology, Inc., PBC

- 6.4.23 Cardno Limited

- 6.4.24 Golder Associates Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment