PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034971

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034971

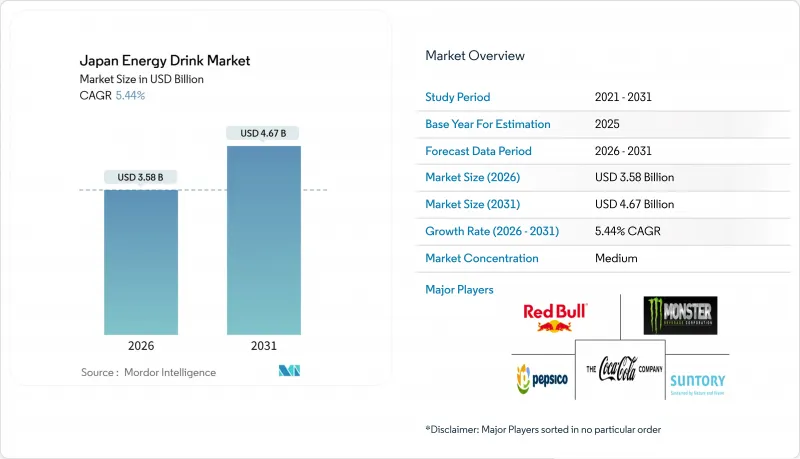

Japan Energy Drink - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan energy drink market size is estimated at USD 3.58 billion in 2026, and is expected to reach USD 4.67 billion by 2031, at a CAGR of 5.44% during the forecast period (2026-2031).

This trajectory reflects a market balancing entrenched consumer habits around traditional vitamin-fortified energy tonics with accelerating demand for natural formulations, premium packaging, and functional ingredients targeting muscle recovery and cognitive performance. Japan's aging workforce and surging e-sports participation create divergent consumption patterns. Older cohorts favor pharmaceutical-heritage brands dispensed through 3.97 million vending machines, while younger gamers gravitate toward carbonated imports and low-sugar variants sold in convenience stores that command the majority of food and beverage sales. The interplay between regulatory stringency under the Ministry of Health, Labour and Welfare, and brand localization strategies determines which players capture share in a market where distribution density, not just brand equity, drives profitability.

Japan Energy Drink Market Trends and Insights

Growing e-sports and gaming culture engagement

Japan's gaming culture is fuelling energy drink adoption among younger demographics, particularly the 13-24 age cohort that comprises the core e-sports audience. Red Bull's global sponsorship of e-sports teams and tournaments translates into localized activations in Japan, where gaming cafes and LAN centers serve as consumption hubs for carbonated energy drinks. Monster is expanding sports marketing in Japan through baseball sponsorships to recruit new consumers and increase visibility in on-premises channels managed by Asahi. The convergence of gaming marathons and energy drink consumption creates a usage occasion distinct from traditional workplace fatigue relief, enabling brands to segment messaging and SKU development around sustained alertness and reaction-time enhancement.

Product innovation and flavor diversification expansion

Flavor localization and functional ingredient layering are reshaping product portfolios as brands compete for shelf space in Japan's 58,000 convenience stores. Kaneka launched Q10 yogurt drinks in March 2024 under the Foods with Function Claims pathway, targeting brain care and stress reduction, a positioning that overlaps with energy drinks' cognitive-enhancement messaging. Kirin relaunched immune-care beverages fortified with LC-Plasma in March 2024, achieving year-over-year growth and targeting 10 million+ cases in 2023, demonstrating consumer appetite for functional claims beyond caffeine. Craft entrants like Penta CRAFT ENERGY SYRUP differentiate through caffeine-free formulations using medicinal herbs, galangal, hops, and cinnamon, positioning as "next-generation energy drinks" that appeal to wellness-oriented consumers wary of stimulant dependency. Suntory's Dekavita C competes with Coca-Cola Japan's Real Gold, Asahi's Dodekamin, and approximately 25 other vitamin drinks, forcing continuous reformulation to maintain relevance.

Health concerns over high caffeine content

Caffeine content scrutiny is intensifying as Japan's Ministry of Health, Labour and Welfare mandates warnings on high-caffeine products, requiring labels to state "not recommended for children or pregnant/breastfeeding women". While Japan lacks specific caffeine limits per serving, the warning requirement signals regulatory caution and can deter health-conscious consumers or parents purchasing for adolescents. International precedents, such as proposals to restrict energy drink sales to minors in various jurisdictions, create the risk that Japan could adopt age-verification requirements at retail, which would compress the addressable market and increase compliance costs. Otsuka's Oronamin C contains caffeine but positions as a vitamin drink rather than an energy drink, sidestepping some scrutiny through heritage and pharmaceutical credibility. The regulatory environment creates a two-tier market: pharmaceutical brands with decades-long safety records face less resistance, while imported carbonated energy drinks with 150-200 milligrams of caffeine per can attract consumer advocacy attention and potential future restrictions.

Other drivers and restraints analyzed in the detailed report include:

- Functional beverages with added health benefits

- Wellness trends encouraging low-sugar formulations

- Stringent labelling and age restriction policies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional energy drinks commanded 77.23% market share in 2025, reflecting decades of consumer loyalty to pharmaceutical-heritage brands like Otsuka's Oronamin C (launched in 1965 in 120-milliliter glass bottles fortified with vitamins B2, B6, C, and caffeine) and Taisho's Lipovitan. These vitamin drinks are dispensed through vending machines and convenience stores, leveraging ubiquitous distribution and workplace fatigue-relief positioning. Yet natural/organic energy drinks are projected to grow at a 5.56% CAGR from 2026 to 2031, driven by clean-label demand and craft entrants like Penta CRAFT ENERGY SYRUP, which uses caffeine-free medicinal herbs (galangal, hops, cinnamon) to appeal to wellness-oriented consumers. Sugar-free or low-calorie energy drinks are expanding as Suntory's 60% sugar-free portfolio in Japan demonstrates corporate commitment to wellness trends, while energy shots remain niche due to limited retail acceptance and consumer preference for larger-format beverages that double as hydration.

The traditional segment's resilience stems from pharmaceutical companies' credibility in functional formulation and their control of vending-machine placements, where Coca-Cola Bottlers Japan's 1.2-1.4 million machines and real-time IoT-enabled assortment optimization create switching costs for consumers accustomed to specific SKU availability. Otsuka introduced label-free Oronamin C bottles in July 2021 to reduce plastic waste, and launched the product in Egypt in April 2024, signaling international expansion ambitions. Natural/organic entrants face distribution barriers but benefit from Foods with Function Claims regulatory flexibility, which allows rapid market entry without pre-approval for health claims. Other energy drinks, including carbonated imports like Monster and Red Bull, occupy a premium niche targeting younger, urban consumers willing to pay 200-300 yen per can versus 120-150 yen for traditional vitamin drinks.

Metal cans are expanding at a 5.72% CAGR from 2026 to 2031, outpacing PET Bottles' 40.22% market share in 2025, propelled by Japan's aluminum can recycling rate (2021) and horizontal recycling rate, compared to PET's. Suntory and UACJ developed the world's first 100% recycled aluminum can, cutting CO2 emissions by 60% and deploying it initially in beer products, with energy drink applications likely to follow. Japanese beverage vendors, including Muji and Dydo, are replacing PET bottles with aluminum cans for sustainability and extended shelf life (90-270 days), creating momentum that benefits energy drink brands seeking premium positioning. MA Aluminum operates Japan's largest can recycling plant, ensuring closed-loop supply chains that appeal to environmentally conscious consumers and corporate sustainability mandates.

PET bottles retain the largest share due to vending machine compatibility, consumer preference for resealable formats during commutes, and lower per-unit costs for high-volume pharmaceutical brands. Glass bottles are declining but persist in heritage products like Oronamin C, where the 120-milliliter glass bottle reinforces pharmaceutical credibility and premium perception. Aseptic Packages (Tetra Pak, cartons, pouches) remain marginal in energy drinks due to consumer associations with juice and milk categories, though functional beverage convergence could expand usage. Disposable cups are negligible, limited to on-premises consumption in cafes and HoReCa settings. Kirin invested Yen 10 billion in 100-milliliter PET bottle production for vending machines, targeting immune-care beverages but signalling broader industry commitment to small-format PET for functional drinks.

The Japan Energy Drink Market is Segmented by Product Type (Traditional Energy Drinks, Energy Shots, and More), Packaging (PET Bottles, Glass Bottles, Metal Cans, and More), Functionality (Endurance/Energy Boost, Muscle Recovery, and More), and Distribution Channel (Horeca and Retail). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Liters).

List of Companies Covered in this Report:

- Taisho Pharmaceutical Co., Ltd.

- Suntory Beverage & Food Ltd.

- Asahi Soft Drinks Co., Ltd.

- Coca-Cola

- Red Bull

- Monster Energy

- PepsiCo

- Kirin Holdings Company, Limited

- Otsuka Pharmaceutical Co., Ltd.

- Sato Pharmaceutical Co., Ltd.

- Meiji Holdings Co., Ltd.

- Fuji Organics Inc.

- Ajinomoto Co., Inc.

- Cheerio Corporation

- Itoh Kanpoh Co., Ltd.

- Kabaya Foods Corporation

- Daiso Pharmaceutical Co., Ltd.

- Amway Japan G.K.

- Osotspa Co., Ltd.

- PepsiCo, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising health and fitness lifestyle influence

- 4.2.2 Product innovation and flavor diversification expansion

- 4.2.3 Growing e-sports and gaming culture engagement

- 4.2.4 Functional beverages with added health benefits

- 4.2.5 Wellness trends encouraging low-sugar formulations

- 4.2.6 Convenience of ready-to-drink energy beverages

- 4.3 Market Restraints

- 4.3.1 Competition from alternative functional beverage categories

- 4.3.2 Health concerns over high caffeine content

- 4.3.3 Sugar content deterring health-focused consumers

- 4.3.4 Stringent labeling and age restriction policies

- 4.4 Consumer Demand Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Product Type

- 5.1.1 Traditional Energy Drinks

- 5.1.2 Sugar-free or Low-calories Energy Drinks

- 5.1.3 Natural/Organic Energy Drinks

- 5.1.4 Energy Shots

- 5.1.5 Other Energy Drinks

- 5.2 Packaging

- 5.2.1 PET Bottles

- 5.2.2 Glass Bottles

- 5.2.3 Metal Can

- 5.2.4 Aseptic packages

- 5.2.5 Disposable Cups

- 5.3 Functionality

- 5.3.1 Endurance/Energy Boost

- 5.3.2 Muscle Recovery

- 5.3.3 Others

- 5.4 Distribution Channel

- 5.4.1 HoReCa

- 5.4.2 Retail

- 5.4.2.1 Supermarkets/Hypermarkets

- 5.4.2.2 Convenience/Grocery Stores

- 5.4.2.3 Online Retail Stores

- 5.4.2.4 Other Distribution Channels

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Taisho Pharmaceutical Co., Ltd.

- 6.3.2 Suntory Beverage & Food Ltd.

- 6.3.3 Asahi Soft Drinks Co., Ltd.

- 6.3.4 Coca-Cola

- 6.3.5 Red Bull

- 6.3.6 Monster Energy

- 6.3.7 PepsiCo

- 6.3.8 Kirin Holdings Company, Limited

- 6.3.9 Otsuka Pharmaceutical Co., Ltd.

- 6.3.10 Sato Pharmaceutical Co., Ltd.

- 6.3.11 Meiji Holdings Co., Ltd.

- 6.3.12 Fuji Organics Inc.

- 6.3.13 Ajinomoto Co., Inc.

- 6.3.14 Cheerio Corporation

- 6.3.15 Itoh Kanpoh Co., Ltd.

- 6.3.16 Kabaya Foods Corporation

- 6.3.17 Daiso Pharmaceutical Co., Ltd.

- 6.3.18 Amway Japan G.K.

- 6.3.19 Osotspa Co., Ltd.

- 6.3.20 PepsiCo, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK