PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034985

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034985

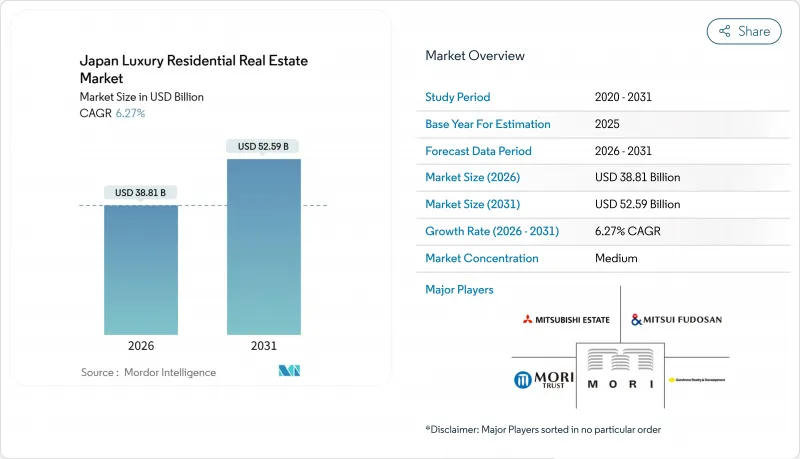

Japan Luxury Residential Real Estate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan Luxury Residential Real Estate Market size is estimated at USD 38.81 billion in 2026, and is expected to reach USD 52.59 billion by 2031, at a CAGR of 6.27% during the forecast period (2026-2031).

Currency depreciation, finite land supply in Tokyo's core wards, and redevelopment pipelines that embed advanced seismic engineering combine to keep pricing firm despite demographic headwinds. Offshore capital benefits from a yen that stayed near 150 per USD through 2025, effectively discounting trophy assets by as much as one-third for dollar-denominated investors. Developers with integrated land banks are absorbing construction-cost inflation, while branded-residence operators widen the rental pool and lift service expectations. Demand spillovers from infrastructure projects in Nagoya and Osaka are diversifying geographic exposure within the Japan luxury residential real estate market, even as natural-hazard and demographic risks temper sentiment outside prime metros.

Japan Luxury Residential Real Estate Market Trends and Insights

Scarcity of Prime Land and View Corridors Supports Price Resilience

Net new residential zoning in Minato, Chiyoda, and Shibuya wards averaged below 0.5% of total land area each year from 2023-2025, creating a structural ceiling on fresh supply. Multi-generational owners hold many of the best parcels, making site assembly slow and expensive. Asahi Shimbun recorded an 8.2% year-on-year land-price jump in Minato for 2024, the steepest since 1991, as developers compete for scarce plots with unobstructed bay or palace vistas. Upper-floor units commanding landmark views now achieve 25-35% premiums over mid-tier stock, double the spread seen in 2020. The Tokyo Metropolitan Government has no plans to enlarge residential zoning in these wards through 2031, locking scarcity into the outlook.

Yen Weakness Boosts Foreign and Expat HNWI Purchasing Power

The yen's slide to 150 per USD in mid-2024 sliced headline prices by roughly 30% relative to 2021 levels for dollar and euro buyers. Foreign direct investment in Japanese real estate hit USD 14 billion in fiscal 2024, up 42% year-on-year, with luxury housing absorbing close to one-fifth of that flow. Resort markets such as Niseko saw international buyers secure nearly 60% of new-build units in 2024, versus 45% two years earlier. Policy risk emerged in late 2025 when officials floated foreign-buyer screening thresholds, but no formal cap has yet been enacted. Monetary-policy divergence suggests currency support will remain in place at least into 2027.

Demographic Headwinds and Thin Liquidity Outside Core Metros

The share of residents aged 65+ reached 28.9% in 2024 and is on course to top 30% by 2030, reducing household formation in prefectures beyond Tokyo, Osaka, and Nagoya. Luxury transactions in Shizuoka and Niigata fell 12% year-on-year during 2024 as local buyer pools shrank. Estate disposals by aging owners are flooding regional markets with dated stock, stretching selling periods, and pushing discounts. Institutional and foreign investors, who could provide liquidity, remain focused on core metros, leaving secondary markets exposed to price drift. Without a demographic reversal, exit options for non-prime high-end assets will stay constrained through the forecast horizon.

Other drivers and restraints analyzed in the detailed report include:

- Redevelopment and Teardown-to-Custom Rebuilds Command Premiums

- Rise of Branded Residences and Serviced/Hotel Hybrids

- Rising Construction and Fit-Out Costs Compress Feasibility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sales transactions dominated with a 69.1% share of the Japan luxury residential real estate market in 2025, yet rentals are rising on the back of expatriate inflows and branded-residence offerings. Rental stock posted 90%+ occupancy across key Mori Living properties and average lease tenures extended to 24 months in 2024, signaling stickier demand. Elevated sales pricing above USD 100,000 per sq m in ultra-prime towers narrows the buyer pool, prompting developers to pivot toward build-to-rent pipelines. The rental segment's 7.31% CAGR to 2031 exceeds the overall Japan luxury residential real estate market size trajectory, suggesting investors will allocate more capital to income-producing models.

Flexibility and turnkey services differentiate rental offerings, especially among international assignees who value predictable monthly outgo over large down payments. Branded-residence leases often include concierge, housekeeping, and wellness amenities bundled into the rent, raising achievable yields. Tax rules also permit depreciation benefits that shelter rental income for certain investor profiles. As corporations adopt hybrid working, executives favor centrally located, fully serviced apartments over suburban ownership, reinforcing rental demand. This evolution indicates that rentals could approach parity with sales by 2031, reshaping revenue mix for integrated developers active in the Japan luxury residential real estate market.

The Japan Luxury Residential Real Estate Market Report is Segmented by Business Model (Sales, Rental), by Property Type (Apartments & Condominiums, Villas & Landed Houses), by Mode of Sale (Primary, Secondary), and by City (Tokyo, Osaka, Nagoya, Rest of Japan). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Mitsubishi Estate Co. Ltd.

- Mitsui Fudosan Co. Ltd.

- Mori Trust Co. Ltd.

- Mori Building Co. Ltd.

- Sumitomo Realty & Development Co. Ltd.

- Tokyu Land Corporation

- Daiwa House Group

- Tokyo Tatemono Co. Ltd.

- Nomura Real Estate Holdings Inc.

- Daikyo Incorporated

- Sekisui House Ltd.

- Sumitomo Forestry Co. Ltd.

- Itochu Property Development Ltd.

- NTT Urban Development Corp.

- Obayashi Corporation

- Hulic Co. Ltd.

- Keio Realty & Development Co. Ltd.

- Mitsui Home Co. Ltd.

- Westbank Corp. (Japan Projects)

- Nakano Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Scarcity of prime land and view corridors in central Tokyo wards (Minato, Chiyoda, Shibuya) supports long-term price resilience.

- 4.2.2 Yen weakness boosts purchasing power for foreign and expat HNWIs in Tokyo, Osaka, Kyoto, and resort markets (e.g., Niseko).

- 4.2.3 Redevelopment pipelines and teardown-to-custom rebuilds command premiums for design, views, and seismic performance.

- 4.2.4 Growth in branded residences and serviced/aparthotel hybrids appealing to global buyers seeking turnkey, amenitized living.

- 4.2.5 Safe-haven appeal-rule of law, quality construction, and low crime-attracts capital allocation to ultra-prime assets.

- 4.3 Market Restraints

- 4.3.1 Demographic headwinds and thin liquidity outside core metros limit exit options for non-prime luxury.

- 4.3.2 Rising construction/fit-out costs and stricter energy/seismic standards elevate total project budgets.

- 4.3.3 Natural hazard exposure (earthquake, flood) and insurance availability/costs add diligence and ownership friction.

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Residential Real Estate Market Size & Growth Forecasts (Value USD billion)

- 5.1 By Business Model

- 5.1.1 Sales

- 5.1.2 Rental

6 Residential Real Estate Market (Sales Model) Size & Growth Forecasts (Value USD billion)

- 6.1 By Property Type

- 6.1.1 Apartments & Condominiums

- 6.1.2 Villas & Landed Houses

- 6.2 By Mode of Sale

- 6.2.1 Primary (New-Build)

- 6.2.2 Secondary (Existing-Home Resale)

- 6.3 By City

- 6.3.1 Tokyo

- 6.3.2 Osaka

- 6.3.3 Nagoya

- 6.3.4 Rest of Japan

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 7.4.1 Mitsubishi Estate Co. Ltd.

- 7.4.2 Mitsui Fudosan Co. Ltd.

- 7.4.3 Mori Trust Co. Ltd.

- 7.4.4 Mori Building Co. Ltd.

- 7.4.5 Sumitomo Realty & Development Co. Ltd.

- 7.4.6 Tokyu Land Corporation

- 7.4.7 Daiwa House Group

- 7.4.8 Tokyo Tatemono Co. Ltd.

- 7.4.9 Nomura Real Estate Holdings Inc.

- 7.4.10 Daikyo Incorporated

- 7.4.11 Sekisui House Ltd.

- 7.4.12 Sumitomo Forestry Co. Ltd.

- 7.4.13 Itochu Property Development Ltd.

- 7.4.14 NTT Urban Development Corp.

- 7.4.15 Obayashi Corporation

- 7.4.16 Hulic Co. Ltd.

- 7.4.17 Keio Realty & Development Co. Ltd.

- 7.4.18 Mitsui Home Co. Ltd.

- 7.4.19 Westbank Corp. (Japan Projects)

- 7.4.20 Nakano Corporation

8 Market Opportunities & Future Outlook

- 8.1 White-space & Unmet-Need Assessment