PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034988

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034988

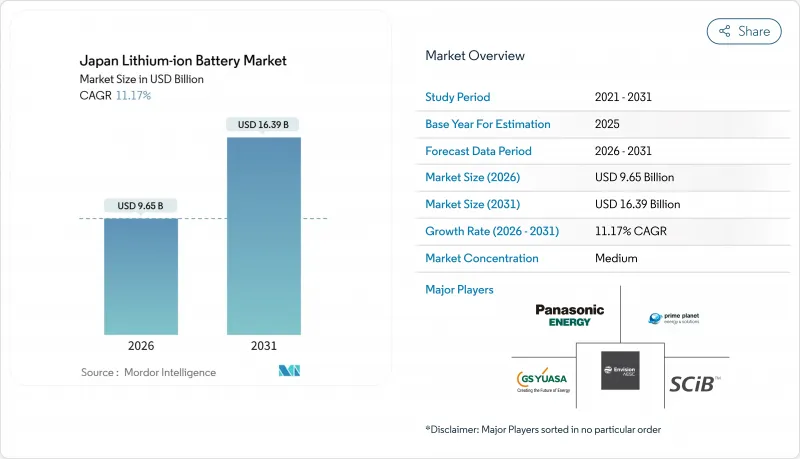

Japan Lithium-ion Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan Lithium-ion Battery Market size is estimated at USD 9.65 billion in 2026, and is expected to reach USD 16.39 billion by 2031, at a CAGR of 11.17% during the forecast period (2026-2031).

Rapid subsidy reform, an aggressive solid-state commercialization roadmap, and the build-out of virtual power-plant programs move batteries from simple energy stores to dynamic grid assets, reinforcing the long-term rise of the Japan Lithium-ion Battery market. Domestic content rules tied to life-cycle carbon disclosures now reward local cell producers that run on Japan's comparatively low-carbon power mix, while export demand for high-reliability industrial batteries supports margins as global mining, robotics, and marine operators shift to electrified platforms. Solid-state pilots backed by JPY 20 trillion in Green Transformation (GX) support funding promise step-change energy density and charging speed, sustaining investor confidence. Meanwhile, the Japan Lithium-ion Battery market benefits from frequency-regulation revenues under the national capacity market, which shortens payback periods for grid-scale storage projects.

Japan Lithium-ion Battery Market Trends and Insights

Government EV Subsidies & Corporate Carbon-Neutral Mandates

Japan raised its electric-vehicle incentive ceiling to JPY 1.3 million in fiscal 2024 but tied eligibility to battery production CO2 footprints, forcing automakers to source low-emission domestic cells. Voluntary emissions trading began in fiscal 2023 and became mandatory in 2026, lifting the cost of carbon-intensive imported batteries. Corporate members of Keidanren must disclose Scope 3 emissions by 2025, so cell suppliers certified under ISO 14067 gain preferential access to procurement lists. The revised Energy Conservation Act also compels large power users to install on-site storage, anchoring demand for stationary systems independent of utility procurements. Collectively, these rules strengthen domestic value capture within the Japan Lithium-ion Battery market.

Accelerated Domestic Solid-State R&D Roadmap (Post-2027 Launch Targets)

Toyota, Nissan, and Panasonic operate pilot lines aiming for 2027-2028 mass production of sulfide or oxide solid-state cells that promise 1,200 km driving range and 10-minute charging. Idemitsu Kosan supplies sulfide electrolytes, targeting production costs below JPY 10,000 per kWh by 2030. Government grants under NEDO and GX bonds cushion capital expenditure, while technical challenges such as interface resistance remain. Early volumes will likely serve premium vehicles and aerospace systems, but confidence in the technology accelerates investment throughout the Japan Lithium-ion Battery market.

Raw-Material Price Volatility & China Refining Dependence

Lithium carbonate collapsed from USD 80,000 per ton in 2022 to USD 10,000-15,000 in 2024, disrupting mine investments and threatening future supply when demand rebounds. Japan imports nearly all of its lithium and cobalt, while China controls about two-thirds of global refining, exposing cell makers to geopolitical risk. Although long-term offtake deals secure volumes for Panasonic and GS Yuasa, smaller firms lack balance-sheet capacity, widening the cost gap within the Japan Lithium-ion Battery market.

Other drivers and restraints analyzed in the detailed report include:

- ESS Build-Out for Virtual-Power-Plant Programs

- Export Demand for High-Reliability Industrial Batteries

- Lengthy Domestic Permitting & Ageing Charger Network

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium Cobalt Oxide captured 30.9% of the Japan Lithium-ion Battery market share in 2025, reflecting entrenched consumer-electronics demand. Lithium Titanate is set to grow at 19.8% per year through 2031 as mining vehicles and frequency-regulation projects value 20,000-cycle durability over energy density. In automotive, Nickel-rich chemistries such as NMC and NCA dominate, with Panasonic's 4680 cells reaching 260 Wh/kg for Tesla platforms. LFP adoption remains limited because cold-weather range loss impedes sales in northern prefectures, though cost pressure could spur gradual uptake. Manganese-based cells serve hybrids and power tools, benefiting from thermal stability.

Over the forecast horizon, the Japan Lithium-ion Battery market will likely segment along three chemistry lanes: cobalt-rich for premium density, titanate for industrial longevity, and manganese or iron phosphate for cost-sensitive mass markets. Each lane requires distinct precursor supply chains, reshaping procurement among cell makers. As solid-state technology matures, chemistries may reorganize once more, but until then, cell producers must manage complex portfolios to balance margin and volume.

Prismatic cells delivered 50.4% of shipments in 2025, favored by Japanese automakers for pack packaging efficiency. Cylindrical output is forecast to rise 16.7% annually as Panasonic ramps 4680 lines in Wakayama and Kansas, offering fivefold capacity gains over 2170 predecessors. Pouch variants stay niche because swelling risks complicate thermal control in long-life industrial settings. The Japan Lithium-ion Battery market thus sees form-factor lock-in, with automakers reluctant to redesign packs mid-cycle.

Format choices influence supplier bargaining power. Automakers embedded in prismatic architectures rely on Prime Planet, reinforcing medium-term stability, while Panasonic's cylindrical roadmap leverages external EV platforms and export demand. Solid-state breakthroughs could upend this balance by introducing new geometries unbound by liquid-electrolyte constraints.

The Japan Lithium-Ion Battery Market Report is Segmented by Product Type (LCO, LFP, NMC, NCA, LMO, LTO), Form Factor (Cylindrical, Prismatic, Pouch), Power Capacity (Up To 3, 000 MAh, 3, 000 To 10, 000 MAh, 10, 000 To 60, 000 MAh, Above 60, 000 MAh), and End-Use Industry (Automotive, Consumer Electronics, Industrial, Stationary Storage, Aerospace, Marine). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Panasonic Energy Co., Ltd.

- Prime Planet Energy & Solutions (PPES)

- GS Yuasa International Ltd.

- Toshiba Corporation

- Envision AESC

- LG Energy Solution

- Contemporary Amperex Technology Ltd. (CATL)

- Maxell, Ltd.

- Furukawa Battery Co., Ltd.

- Lithium Energy Japan

- Sony / Murata Manufacturing Co., Ltd.

- Blue Energy Co., Ltd.

- Vehicle Energy Japan Inc.

- Hitachi Energy Ltd.

- Asahi Kasei Corp.

- Mitsubishi Chemical Group Corp.

- Toray Industries, Inc.

- UBE Corporation

- W-Scope Corporation

- Sumitomo Chemical Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government EV subsidies & corporate carbon-neutral mandates

- 4.2.2 Accelerated domestic solid-state R&D roadmap (post-2027 launch targets)

- 4.2.3 ESS build-out for virtual-power-plant (VPP) programs

- 4.2.4 Export demand for high-reliability industrial batteries (mining & robotics)

- 4.2.5 Corporate fleet electrification of kei-class logistics vehicles

- 4.2.6 Circular-economy value capture via re-use & recycling hubs

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility & China refining dependence

- 4.3.2 Lengthy domestic permitting for gigafactory expansion

- 4.3.3 Ageing charger network & high-power upgrade costs

- 4.3.4 Shrinking domestic consumer-electronics production base

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Lithium Cobalt Oxide (LCO)

- 5.1.2 Lithium Iron Phosphate (LFP)

- 5.1.3 Lithium Nickel Manganese Cobalt (NMC)

- 5.1.4 Lithium Nickel Cobalt Aluminium (NCA)

- 5.1.5 Lithium Manganese Oxide (LMO)

- 5.1.6 Lithium Titanate (LTO)

- 5.2 By Form Factor

- 5.2.1 Cylindrical

- 5.2.2 Prismatic

- 5.2.3 Pouch

- 5.3 By Power Capacity

- 5.3.1 Up to 3,000 mAh

- 5.3.2 3,000 to 10,000 mAh

- 5.3.3 10,000 to 60,000 mAh

- 5.3.4 Above 60,000 mAh

- 5.4 By End-use Industry

- 5.4.1 Automotive (EV, HEV, PHEV)

- 5.4.2 Consumer Electronics

- 5.4.3 Industrial and Power Tools

- 5.4.4 Stationary Energy Storage

- 5.4.5 Aerospace and Defense

- 5.4.6 Marine

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Panasonic Energy Co., Ltd.

- 6.4.2 Prime Planet Energy & Solutions (PPES)

- 6.4.3 GS Yuasa International Ltd.

- 6.4.4 Toshiba Corporation

- 6.4.5 Envision AESC

- 6.4.6 LG Energy Solution

- 6.4.7 Contemporary Amperex Technology Ltd. (CATL)

- 6.4.8 Maxell, Ltd.

- 6.4.9 Furukawa Battery Co., Ltd.

- 6.4.10 Lithium Energy Japan

- 6.4.11 Sony / Murata Manufacturing Co., Ltd.

- 6.4.12 Blue Energy Co., Ltd.

- 6.4.13 Vehicle Energy Japan Inc.

- 6.4.14 Hitachi Energy Ltd.

- 6.4.15 Asahi Kasei Corp.

- 6.4.16 Mitsubishi Chemical Group Corp.

- 6.4.17 Toray Industries, Inc.

- 6.4.18 UBE Corporation

- 6.4.19 W-Scope Corporation

- 6.4.20 Sumitomo Chemical Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment