PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034992

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034992

Japan Management Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

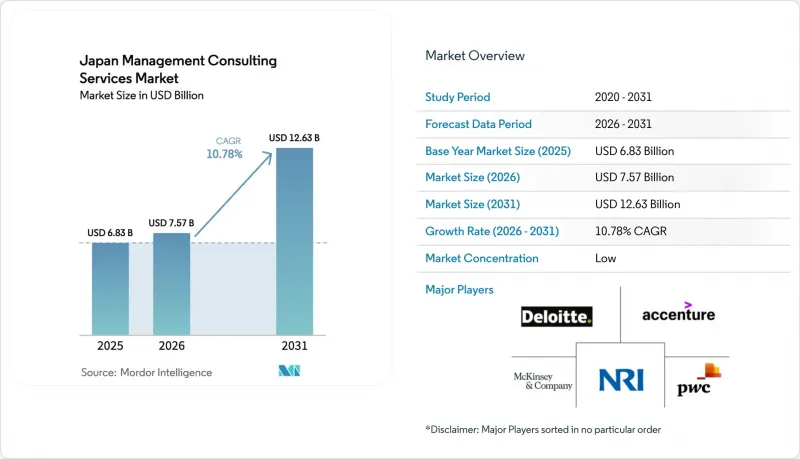

The Japan management consulting services market size is expected to grow from USD 6.83 billion in 2025 to USD 7.57 billion in 2026 and is forecast to reach USD 12.63 billion by 2031 at 10.78% CAGR over 2026-2031.

The current market size reflects strong demand from both public and private sector transformation programs that combine digital-transformation (DX) targets with green-transformation (GX) mandates imposed by Tokyo. Heightened regulatory complexity, demographic pressures, and a nationwide pivot toward data-driven productivity have turned consulting engagements from advisory-only projects into execution-heavy partnerships that embed consultants inside client operating models. The coexistence of DX and GX obligations has created an unprecedented dual catalyst: enterprises must modernize IT systems while simultaneously aligning capital projects with net-zero pathways, an overlap that pushes boards to source outside expertise quickly. In parallel, rapid gains in generative-AI capability, widening subsidy frameworks, and record levels of corporate cash reserves continue to unlock discretionary budgets for large-scale change initiatives across financial services, manufacturing, healthcare, and energy verticals.

Japan Management Consulting Services Market Trends and Insights

Accelerating Corporate Digital-Transformation (DX) Spending

DX budgets have shifted from back-office automation to end-to-end business-model redesign. Government programs under the Digital Agency's "Priority Plan for a Digital Society" call for seamless data interchange among municipalities, catalysing demand for consulting roadmaps that integrate legacy core systems with cloud-native stacks. Enterprise boards increasingly view DX as existential, committing multi-year funds to transform supply chains, customer experience, and cybersecurity layers. Consultants now deliver "AI-transformation" (AIX) offerings that bundle algorithm design, data-governance re-architecture, and workforce reskilling into single statements of work. Market growth further benefits from Tokyo's fast-tracking of open-API standards and public data lakes, which shortens pilot-to-scale timelines and raises client appetite for outcome-based fee models.

Mandatory Green-Transformation (GX) Subsidy Compliance Consulting Surge

The JPY 150 trillion GX roadmap relies on subsidy and tax-incentive instruments that obligate corporations to file voluminous technical documentation. Clients turn to consultancies for lifecycle carbon-accounting toolkits, technology due-diligence, and financial-model alignment needed to access Contracts-for-Difference support for clean-hydrogen, green-steel, and battery projects. Deep-tech startups vying for NEDO grants also request assistance in proposal drafting, commercialization strategies, and partner matchmaking. As a result, GX engagements often span regulatory interpretation, engineering economics, and supply-chain localization within multi-phase scopes lasting up to five years.

Intensifying Price Competition from Freelance Platforms

Platforms such as Another works disclose median monthly consulting fees of JPY 1.2 million, roughly 30 to 40% below traditional firm rates, squeezing margins especially on standardized IT-implementation work. Transparency around rates encourages procurement teams to benchmark aggressively, prompting incumbent firms to adopt modular pricing or subscription-based support. Nevertheless, enterprises still lean on brand-name consultants for board-level credibility and regulatory assurance, which mitigates complete commoditization.

Other drivers and restraints analyzed in the detailed report include:

- Ageing-Workforce Productivity Pressure on Japanese Firms

- Post-Pandemic Hybrid Remote Operating-Model Optimisation

- Consulting-Talent Attrition Due to Startup Ecosystem Growth

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The small and medium-sized enterprise segment accounted for 28.65% of the Japan management consulting services market size in 2025 and is growing at 14.05% CAGR, markedly above the overall trajectory. Much of this velocity stems from supply-chain-transparency clauses inside the Economic Security Promotion Act that apply to vendors regardless of capitalization, compelling SMEs to seek external guidance on data-collection frameworks and cyber-resilience audits. Freelance marketplaces further democratize access by matching niche experts to project-based mandates at transparent price points, enabling owner managers to commission targeted deliverables instead of multi-year retainers. Consulting mandates often focus on hands-on ERP rollouts, subsidy paperwork, and successor-training programs aimed at mitigating founder-retirement risks.

Large enterprises still dominate project value, holding 71.35% of the Japan management consulting services market share in 2025. Budgets cover continent-spanning PMI programs and AI-factory conversions, such as Shiseido's eleven-country FOCUS platform executed with a global consulting consortium. These blue-chip clients value integrated teams that blend strategy, design, and managed services within unified governance structures, securing long-term wallet share for tier-one firms.

Operations consulting retained 27.55% revenue in 2025 as manufacturers rolled out kaizen-driven plant upgrades, yet technology consulting now posts the fastest 13.25% CAGR, capturing projects around generative-AI, zero-trust security, and cloud-native modernization. The Japan management consulting services market size for technology projects reached an estimated USD 2.30 billion in 2026 and is projected to exceed USD 4.28 billion by 2031. Consulting propositions combine large-language-model fine-tuning, data-fabric architecture, and ethical-AI guardrails to satisfy regulators and boards in tandem.

Strategy, HR, and other service lines continue to secure high-margin advisory roles but increasingly integrate analytics accelerators into core offerings. HR engagements, for instance, embed AI-driven skills taxonomies that feed into reskilling pathways for displaced employees, strengthening cross-practice synergies inside firms.

The Japan Management Consulting Services Market Report is Segmented by Organization Size (Large Enterprises, and SMEs), Service Type (Strategy Consulting, Operations Consulting, and More), Delivery Model (On-Site Consulting, and Remote/Virtual Consulting), End-User Industry (IT and Telecommunications, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Accenture Japan Ltd.

- Deloitte Tohmatsu Consulting LLC

- McKinsey and Company Japan

- PwC Consulting LLC (Japan)

- Ernst and Young Strategy and Consulting Co., Ltd.

- KPMG AZSA LLC

- Bain and Company Japan Inc.

- Boston Consulting Group (Japan)

- Nomura Research Institute, Ltd.

- Roland Berger Ltd. (Japan)

- ABeam Consulting Ltd.

- IBM Japan, Ltd. (Consulting)

- NTT DATA Group (Consulting Services)

- Capgemini Japan K.K.

- BearingPoint Japan Co., Ltd.

- NEC Management Partner, Ltd.

- Re-grit Partners, Inc.

- SIGMAXYZ Inc.

- Japan GX Group Inc.

- Members Co., Ltd. (Municipal GX Centre)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating corporate digital-transformation (DX) spending

- 4.2.2 Mandatory Green-Transformation (GX) subsidy compliance consulting surge

- 4.2.3 Ageing-workforce productivity pressure on Japanese firms

- 4.2.4 Post-pandemic hybrid / remote operating-model optimisation

- 4.2.5 Reshoring of critical supply-chains under economic-security law

- 4.2.6 SME succession-planning boom amid record retirements

- 4.3 Market Restraints

- 4.3.1 Intensifying price competition from freelance platforms

- 4.3.2 Consulting-talent attrition due to start-up ecosystem growth

- 4.3.3 Rising client scrutiny over billable-hour models

- 4.3.4 Data-privacy regulations restricting remote-delivery scope

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Bargaining Power of Buyers

- 4.7.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Organization Size

- 5.1.1 Large Enterprises

- 5.1.2 Small and Medium-sized Enterprises

- 5.2 By Service Type

- 5.2.1 Strategy Consulting

- 5.2.2 Operations Consulting

- 5.2.3 HR Consulting

- 5.2.4 Technology Consulting

- 5.2.5 Other Service Types

- 5.3 By Delivery Model

- 5.3.1 On-site Consulting

- 5.3.2 Remote / Virtual Consulting

- 5.4 By End-user Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Financial Services (BFSI)

- 5.4.4 Manufacturing and Industrial

- 5.4.5 Energy and Utilities

- 5.4.6 Government and Public Sector

- 5.4.7 Real Estate and Construction

- 5.4.8 Retail and Consumer Goods

- 5.4.9 Media, Entertainment and Sports

- 5.4.10 Hospitality and Travel

- 5.4.11 Other Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Accenture Japan Ltd.

- 6.4.2 Deloitte Tohmatsu Consulting LLC

- 6.4.3 McKinsey and Company Japan

- 6.4.4 PwC Consulting LLC (Japan)

- 6.4.5 Ernst and Young Strategy and Consulting Co., Ltd.

- 6.4.6 KPMG AZSA LLC

- 6.4.7 Bain and Company Japan Inc.

- 6.4.8 Boston Consulting Group (Japan)

- 6.4.9 Nomura Research Institute, Ltd.

- 6.4.10 Roland Berger Ltd. (Japan)

- 6.4.11 ABeam Consulting Ltd.

- 6.4.12 IBM Japan, Ltd. (Consulting)

- 6.4.13 NTT DATA Group (Consulting Services)

- 6.4.14 Capgemini Japan K.K.

- 6.4.15 BearingPoint Japan Co., Ltd.

- 6.4.16 NEC Management Partner, Ltd.

- 6.4.17 Re-grit Partners, Inc.

- 6.4.18 SIGMAXYZ Inc.

- 6.4.19 Japan GX Group Inc.

- 6.4.20 Members Co., Ltd. (Municipal GX Centre)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment